Broadly this theory may be discussed under 5 sub theories, they are:

1) Interest Rate Parity

2) Purchasing Power Parity

3) Fisher Effect

4) International Fisher Effect

5) Expectation Theory

1)Interest Rate Parity:

This theory states that the interest rate differential between two countries (say $ interest and Rs. interest should be same for exchange risk.) should be equal to the percentage difference between forward exchange rate and spot exchange rate. This theory holds till there is no restriction on moving money from one economy/country/currency to another. Practically, dealers set the forward prices by comparing the differences between $ interest and Rs. interest.

To be precise, when money market and currency are in equilibrium then any interest rates differential should be equal to the % difference in forward exchange rates and spot exchange rate, i.e., there won’t be any question of earning riskless profit otherwise arbitrageurs will earn riskless profit.

IRP Theory relates to a condition of equality of returns on comparable money market instruments.

IRP relates Spot Rate and Forward Rate using two countries’ risk free rates.

For clarity we may take an example:

Suppose an investor has $100000 at the beginning of the year to be invested for a period of 1 year.

Let us say $ interest rates on deposits equals 2% p.a. on the other hand Indian deposits offer attractive interest rate of 10% and exchange rate is Rs.50 per $. Now it is to be decided where the amount should be invested.

Solution:

Case I: If the investor invests in US: Amount at the end of the period will be as 100000*102%= $102000 (100000 as principal plus 2000 as interest)

Case II: If he wishes to invest in India:

-First he has to convert the $ amount into Rupee amount, i.e. he has to buy corresponding rupees, hence he can buy 100000*50=Rs.50,00,000.

-Now he will invest the amount @ 10%, finally at the year end he will have Rs. 50,00,000*110%=55,00,000 (50,00,000-principal + 5,00,000-interest) in his hand.

Hence at last the investor has to convert the Rs. amount generated into $, and we do not know what will be the exchange rate at the year end.

Now see how this theory helps us. As per this theory we can fix today the price at which the Rs. amount to be sold. Such rate(price) fixed today is the forward rate. The one year forward rate is 53.9216*. Therefore by selling Rupees generated at the year end, the investor will be sure to earn 5500000/53.9216=$101999.

Talking about the conclusion we can say that these two investments are offering almost exactly same rate of return.

Now see how 53.9216 is computed as forward rate between $ and Rs.

For every $ invested you will get (1 + R$) and investing in India you will get SR*(1+ RRS)/FR and these have to be equal so as to prevent arbitrage.

Some Formulae:

(i) (FR-SR)/SR= (Rq– Rb) [here, q means quote currency means and b stands for base currency]

[Satisfying the first line of the theory]

(ii) FR=SR*[1+ (Rq– Rb)] [solve first formula]

(iii) (1+Rb) = SR* (1+ Rq)/FR [This formula will give exact result while the above formula gives approximate result]

(iv) FR/SR = (1+ Rq)/ (1+Rb) [solve iii]

(v) (FR-SR)/SR =(Rq– Rb)/(1+Rb) [converting formula at point (i) from approximate to exactness]

(vi) FR= SR*[1+ (Rq– Rb)]t [In case we have t periods and IRP approximation]

Note:There are not 5 formulae, only two –giving approximate and accurate results.

Meanings

Meanings

| forward exchangerate: the agreed upon exchange rate to be used in aforward trade |

forward trade: an agreement to exchange currency at some time in future |

| spot exchnge rate: the exchange rate on a spot trade | spot trade: an agreement to trade currencies based on today’s exchange rate for settlement within two business days |

2)Purchasing Power Parity:

Basically, we have seen that IRP theory is used in obtaining Forward Rate. But we have not discussed how spot rate is determined. Thus, this theory helps in this issue.

There are two forms of PPP-(i) Absolute Form of PPP & (ii) Relative Form of PPP

Absolute Form of PPP:

The basic idea behind this theory is that a commodity costs the same regardless of what currency is used to purchase it or where it is selling. This is a straight forward concept. Loosely, speaking as per this theory 1$ will buy same number of say, burger anywhere in the world.

Assumptions required to hold absolute PPP true

- The transaction cost of trading – shipping, insurance, spoilage & so on must be zero.

- There must be no barrier on trading-no tariffs, taxes or other political barriers.

- The goods traded (burgers) in one place (economy) must be identical to the burger traded in another economy.

Let’s be clear with some cases:

If the burger in India costs Rs. 100 in India and exchange rate is Rs.50 per $, then the same burger should cost Rs.100/50=$2 in America.

Formally discussing:

Let S0 be the spot exchange rate between Rs. & $ [exchange rate is quoted as Rs./$]

P$be the current price in US

P`be the current price in India

Then absolute PPP says that PRs=S0 * P$

If in case the actual exchange rate is Rs.40/$ then with$2 a trader in America would buy a burger in America and ship it to India and sell the same in India @ Rs.100 per burger and convert the Rs.100 into $, as a result of which he will get 100/40 =$2.5, hence he is gaining $0.5 in this transaction.

Since, the trader is making riskless profit and the burgers start moving from US Market to India as a result of which there will be reduced supply of burgers in US and the prices will start rising in US economy at the same time India will lower the price of burger due to increased supply, this will continue till equilibrium is maintained in these two economies. At last the exchange rate quoted will be expected to rise form Rs.40.

Practically, Absolute PPP will not hold true (ignoring some exceptions) because the assumptions of this theory are rarely met.

Relative Form of PPP

This theory does nottell us about what determines the absolute level of exchange rate, moreover, it tells what determines the change in the exchange rate over the given period.

Strictly speaking, this theory implies that the differential inflation rate is always identical to the change in spot rate.

Hence change in exchange rates is determined by the difference in the inflation rates of two countries, i.e. any difference in the rates of inflation will be offset by a change in exchange rate.

If so then let, S0 be the current spot exchange rate at t0 [Rs./$]

E(St ) be the expected exchange rate in t periods

iqbe the inflation in quote currency [iRs]

ibbe the inflation rate in base currency[i$ ]

Now by definition,

[E(St )- S0 ]/ S0 =[iq-ib]

Solving this we get,

E(St )= S0 *[1+{ iq-ib}]

E(St )= S0 *(1+iq )/(1+ib )

Note:For validity of Relative PPP, validity of Absolute PPP is not mandatory. It is already discussed that Absolute PPP will hold true for rare goods, we shall be focusing more on relative PPP.

For example, if prices are rising by 1.0% in the United States and by 6.0% in Mexico, the number of pesos that you can buy for $1 must rise by 1.06/1.01 – 1, or about 5.0%. Therefore purchasing power parity says that to estimate changes in the spot rate of exchange, you need to estimate differences in inflation rates.

Note: If inflation and interest differential are equal then PPP and IRP would give same result.

3)Fisher Effect:

“A change in the expected inflation rate causes the same proportionate change in the nominal interest rate; it has no effect on the required real interest rate.”

This theory tells us the relationship between nominal rates, real rates and inflation. Thus with the help of this theory we can review more carefully the relation between inflation and interests. It is obvious that the investors are ultimately concerned with what they can buy with their money, they need compensation for inflation.

Nominal Return (Money Return): It indicates the rate which money is growing. Nominal rates are called nominal because they have not been adjusted for inflation. It includes inflation. Transactions can be done in the market taking the basis of this return.

Real Return:This return is without inflation. It indicates the rate at which the purchasing power is growing. These are the rates which have been adjusted for inflation.

Example: You have Rs. 1000 today and if you invest the same amount you will be with Rs. 1155 at the year end. And with the same Rs. 1000 you can buy 20 hamburgers at the beginning of the year. Assume the inflation rate to be 5%. (i.e. the price is expected to go up by 5% during the year.)

Now the question arises here about the impact of inflation.

See the calculation here:

Investment at t0 =1000

At year end you will get 1155

Then we can say that nominal interest rate (money return) is (1155-1000)/1000=15.5%

At the beginning you can buy 20 hamburgers [cost per hamburgers is 1000/20=50]

Due to rise in price you have to pay 50*1.05=52.50 for 1 hamburgers at year end.

If you want to buy the hamburgers at the end with your invested amount then you can buy 1155/52.50=22 hamburgers only.

What I would like to concentrate is that despite of 15.50% increase in my investment my purchasing power have gone up by 10% only because of inflation. Frankly speaking I am really 10% rich only.

It can also be stated that with 5% inflation, each of the Rs. 1155 nominal dollars we get is worth 5% less in real terms.

Hence the real Rs. Value of our investment is 1155/1.05=1100 only.

The nominal rate on an investment is the % change in number of rupees you have.

The real rate of the investment is the % change in how much you can buy with your rupees- ie, the % change in your buying power.

Now I would like to make relationship using these 3 terms (real rate, nominal rate & inflation) and the credit for this goes to the great economist Irving Fisher.

Fisher effect tells,

(1+R)=(1+r)*(1+i) [This is the domestic Fisher effect]

Where,

R=Nominal Risk Free Rate

r= Real Risk Free Rate [Fisher assumed this rate to be constant across the countries]

i=Inflation Rate

Finally solving above equation we will get,

r=(R-i)/(1+i)

{(1+i) is the discounting factor, r is constant, if we ignore (1+i) in the denominator because the denominator will be slightly more than one, if done as said, then result of (R-1)/(1+i) will be approximately equal to

(R-1), the we will get R~r+i, means ‘R’ is directly proportional to ‘i’ since ‘r’ is constant}

Fisher on arriving to the conclusion says that investors are not foolish. They do care about the impact of inflation &know that inflation reduces purchasing power and, therefore, they will demand an increase in the nominal rate before lending money.

A rise in the rate of inflation causes the nominal rate to rise just enough so that the real rate of interest is unaffected. In other words, the real rate is invariant to the rate of inflation.

Fisher is of the view that ‘r’ will remain constant irrespective of inflation but not all economists would agree with Fisher that the real rate of interest is unaffected by the inflation rate. Practically ‘r’ differs as per economic conditions of the country.

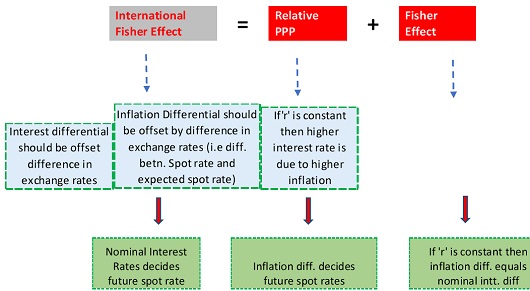

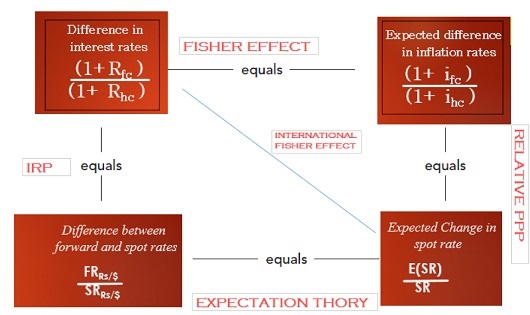

4)International Fisher Effect [also called common real interest rates]

This theory is based on the idea that a country with a higher interest rate will have a higher rate of inflation ultimately it causes its currency to depreciate. In theoretical terms, this relationship is expressed as an equality between the expected % change in exchange rate and the difference between the two countries’ interest rates, divided by one plus the second country’s interest rate.

This tells us that the difference in returns between the home country and a foreign country is just equal to the difference in inflation rates.

Mathematically,

(1+Rfc )/(1+ Rhc)=(1+ ifc)/(1+ ihc)

Because the divisor approximates 1, the expected percent exchange rate change roughly equals the interest rate differential.

ifc− ihc= Rfc− Rhc

5)Expectation Theory

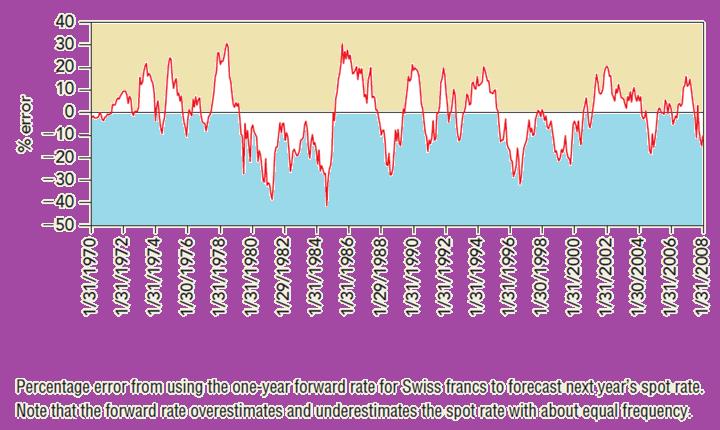

This theory tells that ‘today’s forward rate’ is going to be the ‘future spot rate’.

If this theory, holds then FR=E(S)

Economists and scholars based on their experience and research over the period have seen that forward rates moreover exaggerate the likely change in the spot rate. When FR predicts that the SR will rise in future, then the FR is over estimating the Future SR and vice versa then SR will change as per the prediction, however many researchers have found that , when the forward rate predicts a rise, the spot rate is more likely to fall, and vice versa. You may refer “K. A. Froot and R. H. Thaler, “Anomalies: Foreign Exchange,” Journal of Economic Perspectives 4 (1990), pp. 179–192”

So, this finding is notconsistent with the expectations theory.

Because of this we say “forward rate is an unbiased predictor of future spot rate”.

AT A GLANCE:

DOWNLOAD ARTICLES IN PDF FORMAT

Disclaimer:  The above article is contributed by Niraj Thapa (ICAI Reg. No. : FRO0004147), a CA Final Student currently doing Article ship in a Delhi based Firm and is meant for learning purpose. Due care have been taken into consideration that the content presented above do not violate the opinion of any writers and copyright issues. . For any queries and suggestions you may reach him at: tniraj20@hotmail.com, (Mob. No: +91-7503500777).

The above article is contributed by Niraj Thapa (ICAI Reg. No. : FRO0004147), a CA Final Student currently doing Article ship in a Delhi based Firm and is meant for learning purpose. Due care have been taken into consideration that the content presented above do not violate the opinion of any writers and copyright issues. . For any queries and suggestions you may reach him at: tniraj20@hotmail.com, (Mob. No: +91-7503500777).

I would like to thank Sandeep Sir for publishing the article on “International Finance Theory”, further for readers what I am interested in informing is that the formatting of article has been displayed slightly in a different manner in the website (basically in calculations and numbers) so interested readers may write a mail to receive the file or may follow the link given below:

https://taxguru.in/wp-content/uploads/2014/10/itf-nIRAJ-TAXGURU.pdf

Good work brother, God grace you!

Brief and Nicely presented.