Introduction

Actuarial valuation of Employee benefits requires use of actuarial assumptions to determine the present value of defined benefit obligation (PVDBO).

One of the actuarial assumptions that has in particular a material effect on the valuation is discount rates.

This article describes in detail the methodology for determination of discount rates used in actuarial valuation of Employee Benefits.

As per para 78 of AS15 (R) / 83 of IND AS19 reads as under,

“The rate used to discount post-employment benefit obligations (both funded and unfunded) shall be determined by reference to market yields at the end of the reporting period on government bonds. The currency and term of the government bonds or corporate bonds shall be consistent with the currency and estimated term of the post-employment benefit obligations.”

The standard further states that:

“The discount rate reflects the estimated timing of benefit payments. In practice, an entity often achieves this by applying a single weighted average discount rate that reflects the estimated timing and amount of benefit payments and the currency in which the benefits are to be paid.”

Hence, first the duration of liabilities is calculated in order to determine the term of the government bond and corresponding yield at reporting date, which is used as discount rate in valuation.

Page Contents

Determination of Discount rates

Subsequent sections in this document explain the steps followed to derive the discount rates used in actuarial valuation.

1. Duration of Liabilities

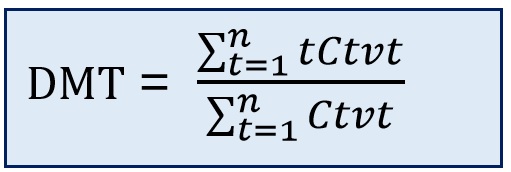

Duration of liabilities (benefit obligations in this case) is calculated using a mathematical method called Macaulay Duration. The Macaulay duration is the weighted average term to maturity of the cash flows from a bond. The weight of each cash flow is determined by dividing the present value of the cash flow by the price.

Macaulay Duration or Discounted Mean Term (DMT) is the mean term of the cash-flows Ct, weighted by present value. It is defined as:

where Ct = Cash-flow at time t, n is the total number of years, t is the respective time period and vt = 1 / (1 + i)^t where i is the annual rate of interest.

- The duration of the liabilities indicates that on an average in how much time the expected liabilities of the company will be paid off.

- Liabilities with higher DMT are more sensitive to the movements/fluctuations in interest rates (i.e., discount rates)

DMT of liability for given Company is determined using following steps:

- The expected benefit pay out for each employee of the company at each time point in future (say t) is estimated using various assumptions such as mortality, salary growth rate etc. The total benefit pay-out for the Company (i.e. sum of pay-outs of all employees) is then estimated at each time point (referred as Ct in formula above)

- DMT of liability for the Company is then estimated using the above formula.

2. Ascertaining the Discount Rates

Once the duration of liability is determined, the government bond yield (G-sec) at that duration as at the reporting date is used as discount rate for valuation of liabilities. The common sources for G-sec yields are www.investing.com and Fixed Income Money Market and Derivatives Association of India (FIMMDA).

Note: Average Future Service is the simple average of Future Service of all employees. It does not include the impact of various decrements such as attrition rate, mortality rate, retirement rate etc. Hence average future service is not the correct term for choosing g-sec yield.

3. Impact of movement in Discount Rates on Value of Liability

Discount rates have an inverse relationship with the value of liability, i.e., increase in the discount rates results in reduction in liability and vice versa. However, the impact also depends on various other factors such as:

- How salary growth rate varies with the movement in discount rates? – Salary growth rate assumption is used to estimate the expected amount of benefit pay-out and impact of movement in salary growth rate on value of liability is opposite to the of the impact due to movement in discount rates. Therefore, change in the salary growth rate offsets the change in value of liabilities on account of discount rate movements. This may not hold true if benefit pay-out has reached its maximum limit (for e.g., 20 Lacs in case of Gratuity).

- Change in the duration of liability – The longer the duration of liability, more sensitive it will be to the movements in discount rates.

4. Yield Curves

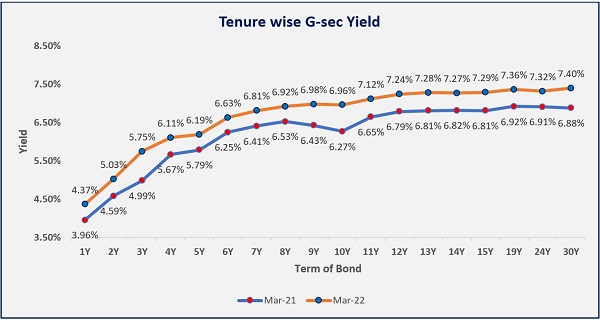

Following graph illustrates the yield on the government bond at different bond terms:

Source: www.investing.com; yields from this website are semi-annual. Graph above shows annualised yield

- G-Sec Yields have increased at Mar-22 from the last year levels and this increase can be seen across all durations.

- An average increase of 50 bps can be observed over the year.

- 10-year bond term shows the highest increase of around 70 bps.

Month on month comparison of G-sec yield over last 10 years for short term, long term and 10 year bond terms is given below:

(Source: www.investing.com) yields from this website are semi-annual. Graph above shows annualised yield

Author Bio

Clear and incisive explanation…

Very insightful article.. Thanks for posting it..