In the previous article, we discussed regarding various provisions of Companies Act, 2013, where valuation is required, profession of registered valuers in India and brief of Valuation Standards issued by ICAI.

In this article, we are going to discuss regarding procedure to be adopted or followed while performing a valuation assignment. Followings are the seps to be taken: –

I. Analyse the asset to be valued and collect the necessary information

II. Define the Valuation Base

III. Select the premise of Value

IV. Consider and apply appropriate valuation approaches and methods

V. Arrive at a value or a range of values

In this article, broadly, we will discuss point IV. Valuation approaches and methods and give a brief introduction of rest.

1. Analyse the asset to be valued and collect the necessary information: –

The first step of the valuation procedure is to analyse the asset being valued and collect the necessary information (financial and non-financial). This is the very much crucial steps amongst all other steps as information analysed and collected in this step shall assist the Registered Valuer in selecting the valuation base, premise of value and appropriate valuation methods.

The nature and extent of the information required to perform the analysis shall depend on the following:

- nature of the asset to be valued;

- scope and purpose of the valuation engagement;

- the valuation date;

- the intended use of the valuation;

- the applicable ICAI Valuation Standard;

- the applicable premise of value;

- assumptions and limiting conditions; and

- applicable governmental regulations or regulations prescribed by

- other regulators or other professional standards;

In analysing the asset to be valued, the valuer shall gather, analyse and adjust the relevant information necessary to perform a valuation, appropriate to the nature or type of the engagement.

II. Define the Valuation Base: –

As per Valuation Standard-102, Valuation base means the indication of the type of value being used in an engagement. Different valuation bases may lead to different conclusions of value. Therefore, it is important for the valuer to identify the bases of value pertinent to the engagement. This Standard defines the following valuation bases:

- Fair value;

- Participant specific value; and

- Liquidation value

III. Select the premise of Value: –

As per Valuation Standard-102, Premise of Value refers to the conditions and circumstances how an asset is deployed. In a given set of circumstances, a single premise of value may be adopted while in some situations multiple premises of value may be adopted. Some common premises of value are as follows:

- highest and best use;

- going concern value;

- as is where is value;

- orderly liquidation; or

- forced transaction.

The premise shall always reflect the facts and circumstances underlying each valuation engagement. Determining the business value depends upon the situation in which the business is valued, i.e., the events likely to happen to the business as contemplated at the valuation date.

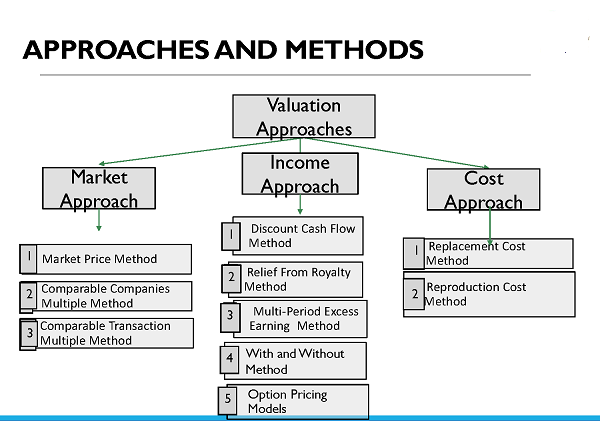

IV. Consider and apply appropriate valuation approaches and methods: –

Internationally following are the three main valuation approaches: –

- Market Approach;

- Income Approach; and

- Assets Approach.

ICAI VS-103, also defines these three approaches. These approaches further contain different valuation methods within their criteria as follows: –

MARKET APPROACH: –

Market approach is a valuation approach that uses prices and other relevant information generated by market transactions involving identical or comparable (i.e., similar) assets, liabilities or a group of assets and liabilities, such as a business.

The following are some of the instances where a valuer applies the market approach:

a. where the asset to be valued or a comparable or identical asset is traded in the active market;

b. there is a recent, orderly transaction in the asset to be valued; or

c. there are recent comparable orderly transactions in identical or comparable asset(s) and information for the same is available and reliable.

The following are the common methodologies for the market approach:

- Market Price Method;

- Comparable Companies Multiple Method; and

- Comparable Transaction Multiple Method.

Market Price Method:

A valuer shall consider the traded price observed over a reasonable period while valuing assets which are traded in the active market. A valuer shall also consider the market where the trading volume of asset is the highest when such asset is traded in more than one active market. A valuer shall use average price of the asset over a reasonable period. The valuer should consider using weighted average or volume weighted average to reduce the impact of volatility or any one-time event in the asset.

Comparable Companies Multiple (CCM) Method: –

I. Comparable Companies Multiple Method, also known as Guideline Public Company Method, involves valuing an asset based on market multiples derived from prices of market comparable traded on active market.

II. The following are the major steps in deriving a value using the CCM method:

(a) identify the market comparables;

(b) select and calculate the market multiples of the identified market comparables;

(c) compare the asset to be valued with the market comparables to understand material differences; and make necessary adjustments to the market multiple to account for such differences, if any;

(d) apply the adjusted market multiple to the relevant parameter of the asset to be valued to arrive at the value of such asset; and

(e) if value of the asset is derived by using market multiples based on different metrics/parameters, the valuer shall consider the reasonableness of the range of values.

III. While identifying and selecting the market comparables, a valuer shall consider the factors such as-

a. industry to which the asset belongs;

b. geographic area of operations;

c. similar line of business, or similar economic forces that affect the asset being valued; or

d. other parameters such as size (for example – revenue, assets, etc), stage of life-cycle of the asset, profitability, diversification, etc.

IV. The market multiples are generally computed on the basis of following inputs:

a. trading prices of market comparables in an active market; and

b. financial metrics such as Earnings Before Interest, Tax, Depreciation and Amortisation (EBITDA), Profit After Tax (PAT), Sales, Book Value of assets, etc.

V. If market participants are using market multiple based on nonfinancial metrics for valuing an asset, such multiples may also be considered by the valuer in addition to market multiple based on the financial metrics. For example, Enterprise Value (EV) / Tower in case of tower telecom companies, EV/Tonne in case of cement industry, etc.

VI. The following are some of the differences between the asset to be valued and market comparable that the valuer may consider while making adjustments to the market multiple:

a. size of the asset;

b. geographic location;

c. profitability;

d. stage of life-cycle of the asset;

e. diversification;

f. historical and expected growth; or

g. management profile.

Comparable Transaction Multiple (CTM) Method

I. Comparable Transaction Multiple Method, also known as ‘Guideline Transaction Method’ involves valuing an asset based on transaction multiples derived from prices paid in transactions of asset to be valued /market comparables (comparable transactions). The price paid in comparable transactions generally include control premium, except where transaction involves acquisition of noncontrolling/ minority stake. The following are the major steps in deriving a value using the CTM method:

a. identify comparable transaction appropriate to the asset to be valued;

b. select and calculate the transaction multiples from the identified comparable transaction;

c. compare the asset to be valued with the market comparables and make necessary adjustments to the transaction multiple to account where differences, if any existed;

d. apply the adjusted transaction multiple to the relevant parameter of the asset to be valued to arrive at the value of such asset; and

e. if valuation of the asset is derived by using transaction multiples based on different metrics or parameters, the valuer shall consider the reasonableness of the range of values and exercise judgement in determining a final value.

II. The transaction multiples are generally computed based on the following two inputs:

a. price paid in the comparable transaction; and

b. financial metrics such as EBITDA, PAT, Sales, Book Value, etc of the market comparable.

III. Even multiples based on non-financial metrics such as EV per room for hotels, EV/Bed for hospitals) can be considered.

IV. A valuer shall preferably use multiple comparable transactions of recent past rather than relying on a single transaction.

V. The following are some of the differences between the asset to be valued and comparable transaction that the valuer may consider while making adjustments to the transaction multiple:

a. size of the asset;

b. geographic location;

c. profitability;

d. stage of life-cycle of the asset;’

e. diversification;

f. historical and expected growth;

g. management profile such as private ownership vs. public sector undertaking; or

h. conditions if any governing the comparable transaction such as deferred payment of consideration contingent on achievement of certain milestones).

Discounts and Control Premium

A valuer shall evaluate and make adjustments for differences between the asset to be valued and market comparables/comparable transactions. The most common adjustment under CCM method and CTM method pertain to ‘Discounts’ and ‘Control Premium’. ‘Discounts’ include Discount for Lack of Marketability (DLOM) and Discount for Lack of Control (DLOC).

DLOM is based on the premise that an asset which is readily marketable (such as frequently traded securities) commands a higher value than an asset which requires longer marketing period to be sold (such as securities of an unlisted entity) or an asset having restriction on its ability to sell (such as securities under lock-in-period or regulatory restrictions).

Control Premium generally represents the amount paid by acquirer for the benefits it would derive by controlling the acquiree’s assets and cash flows. Control Premium is an amount that a buyer is willing to pay over the current market price of a publicly-traded company to acquire a controlling interest in an asset. It is opposite of discount for lack of control to be applied in case of valuation of a noncontrolling/ minority interest.

INCOME APPROACH: –

I. Income approach is a valuation approach that converts maintainable or future amounts (e.g., cash flows or income and expenses) to a single current (i.e., discounted or capitalised) amount. The fair value measurement is determined on the basis of the value indicated by current market expectations about those future amounts. This approach involves discounting future amounts (cash flows/income/cost savings) to a single present value.

II. The following are some of the instances where a valuer may apply the income approach:

a. where the asset does not have any market comparable or comparable transaction;

b. where the asset has fewer relevant market comparables; or

c. where the asset is an income producing asset for which the future cash flows are available and can reasonably be projected.

III. Some of the common valuation methods under income approach are as follows:

a. Discounted Cash Flow (DCF) Method;

b. Relief from Royalty (RFR) Method;

c. Multi-Period Excess Earnings Method (MEEM);

d. With and Without Method (WWM); and

e. Option pricing models.

Discounted Cash Flow (‘DCF’) Method: –

I. The DCF method values the asset by discounting the cash flows expected to be generated by the asset for the explicit forecast period and also the perpetuity value (or terminal value) in case of assets with indefinite life. The DCF method is one of the most common methods for valuing various assets such as shares, businesses, real estate projects, debt instruments, etc. This method involves discounting of future cash flows expected to be generated by an asset over its life using an appropriate discount rate to arrive at the present value.

II. The following are the major steps in deriving a value using the DCF method:

a. Consider the projections to determine the future cash flows expected to be generated by the asset;

b. analyse the projections and its underlying assumptions to assess the reasonableness of the cash flows;

c. choose the most appropriate type of cash flows for the asset, viz., pre-tax or post-tax cash flows, free cash flows to equity or free cash flows to firm;

d. determine the discount rate and growth rate beyond explicit forecast period; and

e. apply the discount rate to arrive at the present value of the explicit period cash flows and for arriving at the terminal value.

III. While using the DCF method, it may also be necessary to make adjustments to the valuation to reflect matters that are not captured in either the cash flow forecasts or the discount rate adopted. In case of the DCF method, projected cash flows reflect the benefits of control and accordingly the value of asset arrived under this method is not to be grossed up for control premium.

IV. The following are important inputs for the DCF method:

A. Cash flows;

B. Discount rate; and

C. Terminal value

A. Cash flows: –

I. In most cases, the projections shall comprise the statement of profit & loss, balance sheet, cash flow statement, along with the underlying key assumptions. However, in certain cases, if balance sheet and cash flow statement are not available, details of future capital expenditure and working capital requirements may also suffice.

II. The projections reflect the accrual based accounting income and expenses. For arriving at the cash flows, non-cash expenses, such as depreciation and amortisation, shall be added back. Further, cash outflows relating to capital expenditure and incremental working capital requirements, if any shall be deducted.

III. Generally, historical financial statements are used as the base for preparation of projections. If in future, changes in circumstances are anticipated the assumptions underlying the projections shall reflect differences on account of such differences vis-à-vis the historical financial statements.

IV. The length of the period of projections (explicit forecast period) shall be determined based on the following factors:

a. Nature of the asset- where the business is of cyclical nature, explicit forecast period should ordinarily consider one entire cycle (for example cement business).

b. Life of the asset- In case of asset with definite life, explicit period should be for the entire life of the asset (for example, debt instruments, Build Operate Transfer (BOT) road projects).

c. Sufficient period- The forecast period should have a length of time that is sufficient for the asset to achieve stable levels of operating performance.

d. Reliable data- The data that are used for projecting the cash flows, should be reliable.

V. The following are the cash flows which are used for the projections:

a. Free Cash Flows to Firm (FCFF): FCFF refers to cash flows that are available to all the providers of capital, i.e. equity shareholders, preference shareholders and lenders. Therefore, cash flows required to service lenders and preference shareholders such as interest, dividend, repayment of principal amount and even additional fund raising are not considered in the calculation of FCFF.

b. Free Cash Flows to Equity (FCFE): FCFE refers to cash flows available to equity shareholders and therefore, cash flows after interest, dividend to preference shareholders, principal repayment and additional funds raised from lenders / preference shareholders are considered.

B. Discount rate: –

I. Discount Rate is the return expected by a market participant from a particular investment and shall reflect not only the time value of money but also the risk inherent in the asset being valued as well as the risk inherent in achieving the future cash flows.

II. The following discount rates are most commonly used depending upon the type of the asset:

i. cost of equity;

ii. weighted average cost of capital;

iii. Internal Rate of Return (‘IRR’);

iv. cost of debt; or

v. yield.

III. Different methods are used for determining the discount rate. The most commonly used methods are as follows:

i. Capital Asset Pricing Model (CAPM) for determining the cost of equity.

ii. Weighted Average Cost of Capital (WACC) is the combination of cost of equity and cost of debt weighted for their relative funding in the asset.

iii. Build-up method (generally used only in absence of market inputs).

IV. A valuer may consider the following factors while determining the discount rate:

i. cash flows used for the projections as FCFE needs to be discounted by Cost of Equity whereas FCFF to be discounted using WACC;

ii. pre-tax cash flows need to be discounted by pre-tax discount rate and post-tax cash flows to be discounted by post-tax discount rate;

C. Terminal value: –

I. Terminal value represents the present value at the end of explicit forecast period of all subsequent cash flows to the end of the life of the asset or into perpetuity if the asset has an indefinite life.

II. In case of assets having indefinite or very long useful life, it is not practical to project the cash flows for such indefinite or long periods. Therefore, the valuer needs to determine the terminal value to capture the value of the asset at the end of explicit forecast period.

III. There are different methods for estimating the terminal value. The commonly used methods are:

(a) Gordon (Constant) Growth Model: The terminal value under this method is computed by dividing the perpetuity maintainable cash flows with the discount rate as reduced by the stable growth rate. The estimation of stable growth rate is of great significance because even a minor change in stable growth rate can have an impact on the terminal value and the value of the asset too.

(b) Variable Growth Model: The Constant Growth Model assumes that the asset grows (or declines) at a constant rate beyond the explicit forecast period whereas the Variable Growth Model assumes that the asset grows (or declines) at variable rate beyond the explicit forecast period.

(c) Exit Multiple: The estimation of terminal value under this method involves application of a market-evidence based capitalisation factor or a market multiple (for example, Enterprise Value (EV) / Earnings before Interest, Tax, Depreciation and Amortisation (EBITDA), EV / Sales) to the perpetuity earnings / income.

(d) Salvage / Liquidation value: In some cases, such as mine or oil fields, the terminal value has limited or no relationship with the cash flows projected for the explicit forecast period. For such assets, the terminal value is calculated as the salvage or realisable value less costs to be incurred for disposing of such asset.

Relief from Royalty (RFR) Method: –

I. RFR Method is a method in which the value of the asset is estimated based on the present value of royalty payments saved by owning the asset instead of taking it on lease. It is generally adopted for valuing intangible assets that are subject to licensing, such as trademarks, patents, brands, etc.

II. The fundamental assumption underlying this method is that if the intangible asset to be valued had to be licensed from a third-party owner there shall be a royalty charge for use of such asset. By owning the said intangible asset, royalty outgo is avoided. The value under this method is equal to the present value of the licence fees / royalty avoided by owning the asset over its remaining useful life.

III. The following are the major steps in deriving a value using the RFR method:

a. obtain the projected income statement associated with the intangible asset to be valued over the remaining useful life of the said asset from the client or the target;

b. analyse the projected income statement and its underlying assumptions to assess the reasonableness;

c. select the appropriate royalty rate based on market-based royalty rates for similar intangible assets or using the profit split method;

d. deduct costs associated with maintaining licencing arrangements for the intangible asset from the resultant royalty savings;

e. apply the selected royalty rate to the future income attributable to the said asset;

f. use the appropriate marginal tax rate or such other appropriate tax rate to arrive at an after-tax royalty savings;

g. discount the after-tax royalty savings to arrive at the present value using an appropriate discount rate; and

h. Tax amortisation benefit, if appropriate, should be added to the overall value of the asset.

Multi-Period Excess Earnings Method (MEEM): –

I. MEEM is generally used for valuing intangible asset that is leading or the most significant intangible asset out of group of intangible assets being valued. The fundamental concept underlying this method is to segregate the earnings attributable to the intangible asset being valued. Intangible assets which have a finite life can only be used to value using MEEM. The value under this method is equal to the present value of the incremental after-tax cash flows (‘excess earnings’) attributable to the intangible asset to be valued over its remaining useful life.

II. The following are the major steps in deriving a value using the MEEM

a. obtain the projections for the entity or the combined asset group over the remaining useful life of the said intangible asset to be valued from the client or the target to determine the future after tax cash flows expected to be generated;

b. analyse the projections and its underlying assumptions to assess the reasonableness of the cash flows;

c. Contributory Asset Charges (CAC) or economic rents to be reduced from the total net after-tax cash flows projected for the entity/combined asset group to obtain the incremental after-tax cash flows attributable to the intangible asset to be valued;

d. the CAC represent the charges for the use of an asset or group of assets (e.g., working capital, fixed assets, assembled workforce, other intangibles) based on their respective fair values and should be considered for all assets, excluding goodwill, that contribute to the realisation of cash flows for the intangible asset to be valued;

e. discount the incremental after-tax cash flows attributable to the intangible asset to be valued to arrive at the present value using an appropriate discount rate; and

f. Tax amortisation benefit, if appropriate.

With and Without Method (WWM): –

I. Under WWM, the value of the intangible asset to be valued is equal to the present value of the difference between the projected cash flows over the remaining useful life of the asset under the following two scenarios:

(a) business with all assets in place including the intangible asset to be valued; and

(b) business with all assets in place except the intangible asset to be valued.

II. The following are the major steps in deriving a value using the WWM:

(a) obtain cash flow projections for the business over the remaining useful life of the said asset to be valued under the following two scenarios:

(i) business with all assets in place including the intangible asset to be valued; and

(ii) business with all assets in place except the intangible asset to be valued.

(b) analyse the projections and its underlying assumptions to assess the reasonableness of the cash flows;

(c) discount the difference between the projected cash flows under two scenarios to arrive at the present value using an appropriate discount rate; and

(d) Tax amortisation benefit, if appropriate.

Option Pricing Models: –

I. There are several methods to value options, of which the Black-Scholes-Merton Model and Binomial Model are widely used. The important inputs required in these models are as under:

a. current price of asset to be valued;

b. exercise price;

c. life of the option;

d. expected volatility in the price of the asset;

e. expected dividend yield; and

f. risk free interest rate.

II. These models value options by creating replicating portfolios composed of asset to be valued and riskless lending or borrowing.

COST APPROACH: –

I. Cost approach is a valuation approach that reflects the amount that would be required currently to replace the service capacity of an asset (often referred to as current replacement cost). In certain situations, historical cost of the asset may be considered by the valuer where it has been prescribed by the applicable regulations/law/guidelines or is appropriate considering the nature of the asset.

II. Examples of situations where a valuer applies the cost approach are:

a. an asset can be quickly recreated with substantially the same utility as the asset to be valued;

b. in case where liquidation value is to be determined; or

c. income approach and/or market approach cannot be used.

III. The following are the two most commonly used valuation methods under the Cost approach:

(a) Replacement Cost Method: Replacement Cost Method, also known as ‘Depreciated Replacement Cost Method’ involves valuing an asset based on the cost that a market participant shall have to incur to recreate an asset with substantially the same utility (comparable utility) as that of the asset to be valued, adjusted for obsolescence. The following are the major steps in deriving a value using the Replacement Cost method:

a. estimate the costs that will be incurred by a market participant for creating an asset with comparable utility as that of the asset to be valued;

b. assess whether there is any loss on account of physical, functional or economic obsolescence in the asset to be valued; and

c. adjust the obsolescence value, if any as determined under above from the total costs estimated under (a) above, to arrive at the value of the asset to be valued.

(b) Reproduction Cost Method: Reproduction Cost Method involves valuing an asset based on the cost that a market participant shall have to incur to recreate a replica of the asset to be valued, adjusted for obsolescence. The following are the major steps in deriving a value using the Reproduction Cost method:

a. estimate the costs that will be incurred by a market participant for creating a replica of the asset to be valued;

b. assess whether there is any loss of value on account of physical, functional or economic obsolescence in the asset to be valued; and

c. adjust the obsolescence value, if any as determined under (b) above from the total costs estimated under (a) above, to arrive at the value of the asset to be valued.

Author Bio

Very use full pl sened time on my mailer wadsup no. 9430704033

It is very useful. Thank you.

It is understandable and very well compiled.