Simplifying Joint Development agreements (JDA)

I am going to tell u what is Real Estate sector

Real Estate Sector: A real estate business is a business entity that deals with the buying, selling, management, or investment of real estate properties. Real estate is “the property, land, buildings, air rights above the land and underground rights below the land.

Firstly, we will discuss types of Real estate projects

1. Builder purchasing land and constructing the land and selling to customers.

In this mode, the builder has to invest the capital on both lands and for construction. It will create a burden on the Builder with heavy investment.

Ex: Builder purchases land at Vijayawada and incurs expenditure on construction on that land. He is receiving the advances from the Customer during the construction phase and selling the flats and receiving the payment after the completion of construction.

Gst implication

| Sale during construction phase | Sale after completion of construction |

| Gst liability @ 5%/1%/12% | No GST liability |

| Tax @ 1%/5% – No ITC

Tax @ 12% – ITC Eligible |

No ITC |

1% tax rate – Affordable residential houses

| Metropolitan Cities | Non-metropolitan cities |

| Bangalore, Chennai, Hyderabad, Delhi, Mumbai, Noida, Ghaziabad, Gurgaon, Faridabad, Kolkata | Other than Metropolitan Cities |

| Gst rate @ 1% if

a. Carpet area <= 60sq.mts & b. Cost of Flat <= 45 Lakhs |

Gst rate @ 1% if

a. Carpet area <= 90sq.mts & b. Cost of Flat <= 45 Lakhs |

Both conditions should be fulfilled. If any of the conditions failed to satisfy then it goes under the Non-Affordable Housing Projects.

| 90 sq. Meters – 107.6391 Sq. Yards – 968.752 SFT

60 Sq. Meters – 71.7594 Sq. Yards – 645.835 SFT |

Value in Agreement is to be considered for cost of Flat

As per Notification no. 3/2019- Central tax (rate)

The specified GST rates

Residential Buildings

| Particulars | Affordable Housing projects | Non-affordable Housing projects |

| CGST | 0.75% | 3.75% |

| SGST | 0.75% | 3.75% |

| Total | 1.5% | 7.5% |

| Less: 1/3rd value of Land | 0.5% | 2.5% |

| Gst rate | 1% | 5% |

| ITC Eligible | No | No |

Total Carpet Area = Residential housing+ Commercial complex

The tax rate of 5% will apply only when the ratio of area commercial complex to Total Carpet area does not exceed 15%

Carpet area of Commercial complex * 100 <= 15%

Total Carpet Area

In Residential housing Project including commercial complex, we will use inputs and input services for the whole project. There will be difficulty in identifying inputs and input services for claiming ITC.

The inputs and Input services used for Residential Housing Project are ineligible for Claiming ITC.

Then we have to follow Rule 42.

| Reversal of ITC = Common ITC * Carpet area of Residential Housing

Total Carpet Area |

The Calculated amount should be reversed while filing

Form Gstr-3b

The value of flat includes an undivided share of land

According to the Negative list (Schedule III)

Sale of Land is not liable to GST

For valuation purposes, 1/3 value is for Land Value.

Calculation of GST rate after excluding land value

In some cases, they say that we know the land value. So, we will do calculations after excluding the land value from flat value.

Is it allowed- No

Explanation: As per notification no.11/2017

It is presumed that the value of land is 1/3rd of the supply

We have excluded the 1/3rd land value irrespective of the actual value of the land.

2. Works Contractor (Material Contract)

The landowner gives the land to the contractor and the Contractor constructs the property in the given land (both including material cost and labor cost) upon receiving a lumpsum consideration from Landowner.

The consideration will be fixed per sq. feet basis in this works contract/material contract in case of Commercial/ Residential properties

Rate of Tax (ITC Eligible)

| Affordable Housing | Non-affordable Housing |

| 12% | 18% |

Value of Supply = Material Cost + Labour Cost + Profit (charged by contractor)

There is no concept of Land value in the Works Contract.

3 Labour Contractor

The landowner gives the land and material to the Contractor. The contractor will supply labor service for the construction of Property.

The landowner will pay a lump sum consideration for the construction of property upon supplying labor by the landowner.

The consideration will be fixed on Per sq. feet basis.

| Single residential unit | Any other case |

| Exempt

(as per Notification no.12/2017) |

Taxable @ 18% |

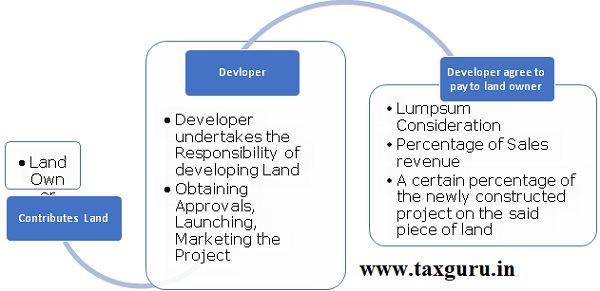

4. JDA (Discussion Point)

what is the role of JDA In the Real estate sector?

We mostly see JDA’s in the Real estate sector.

Joint Development Agreement:

Note: This JDA varies depending upon the terms & conditions, mutually agreed upon by the parties.

Benefits of entering into JDA

| Sl.no | Landowner | Developer |

| 1 | No need for capital investment for construction | Avoiding huge investment in buying land |

| 2 | Will get Developed Property | Will get profit without buying land. |

| 3 | Will get lumpsum consideration in terms of money and constructed flats | Will get Profit on sale of flats. Speedy construction of the property by the developer. |

Taxability of JDA Transactions

In the hands of Landowner and Developer

There are two tax regimes will apply

1. GST

2. Income tax

We will discuss firstly on Gst on JDA

There are Three Transactions in JDA

a. Landowner to Builder

This is a Supply of Transferrable Development Rights to Builder

The landowner is the supplier of service and Builder is the recipient of service.

The supply of TDR is exempt as per notification no. 4/2019

b. Builder to Landowner

Builder is constructing the flats and giving flats to the landowner in consideration of the supply of land by the landowner.

Here, Landowner is the supplier of services i.e., Construction services and Landowner is the recipient of service.

–

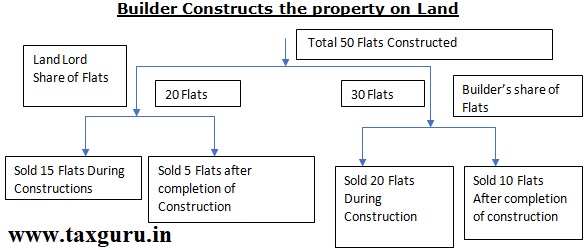

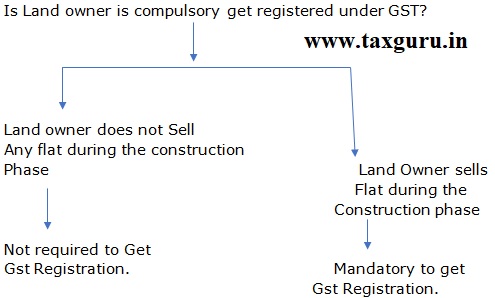

Steps to be followed by the landowner while paying Gst on sale of Flats during the Construction phase. (15 Flats)

1. The landowner should collect GST from customers 1%/5%/12% according to the nature of the activity.

2. The landowner should pay the Gst to the Builder

3. The builder should file GSTR-1 and GSTR-3B

In B2B Transaction, The Builder should quote the GSTIN of Landowner and file returns.

4. The landowner Should file GSTR-1 and pay the GST to the Government.

In GSTR-3B the Landowner should show as supplies made to Customers as Outward supply

The calculation is as follows

| Particulars | Reference | Calculation |

| Outward supply in GSTR-3B | 1%/5%/12% | Tax on Supply (Sale of Flats) |

| Less: ITC available in GSTR-2A | Tax paid to Builder | Input Tax Credit |

| Tax payable | Nil |

Builders are ineligible to claim ITC.

Balance 5 Flats: The Landowner is not required to pay Gst. The Builder will pay Gst on 5 Flats.

Builder Share of Flats:

During construction phase Builder sold 20 flats. The builder has to pay Gst on sale of 20 flats.

Builder is ineligible to claim ITC in case of 1%/5% Cases i.e., Affordable and Non-Affordable housing project Cases.

Builder is eligible to claim ITC on 12% Cases i.e., Commercial Projects.

Note: In Landowner case is eligible to claim ITC we have made a transaction to avoid double taxation both to landowner and Builder

In this case, if Landowner is selling both Residential and Commercial Building then he is eligible to claim ITC only for commercial buildings. If inputs and input services register maintained separately for Commercial and Residential buildings, he can claim ITC easily. But, in case of Common inputs and input services for both the buildings then he should follow Rule 42 for the reversal of ITC.

Balance 10 Flats i.e., Sale of Flats after completion of Construction.

Supply of Transferrable Development Rights is exempted supply i.e., it is an exempt supply under (Entry 41A/41B) Notification no. 04/2019.

This exemption will apply only when all the flats sold under the construction process.

But if any unsold flats are lying with the builder after issuance of completion certificate by the competent authority then

Note: Gst payable on Commercial buildings @ 18% on TDR value.

Here the supplier of TDR is Landowner. Hence, the landowner has to pay Gst on TDR. But, as per sec 9(3), this concept is covered under RCM so the recipient i.e., Builder is required to pay GST under the concept of TDR.

Whether ITC is available to Builders

| 1%/5% | ITC not available |

| 18% | ITC available |

The payment of Gst will arise only after the issuance of completion certificate.

The flats sold after completion, there will be no charge of

GST on that flats. But, as per RCM provisions the builder has to pay GST on TDR on SDV of unsold Flats.

The builder has to pay Gst on flats given to Landowner for consideration of Land given for Development.

The liability will arise to the landowner upon the receipt of consideration in the form Developed flats. The payment of Gst is made by the Builder only.

The Gst will be paid on the SDV of the flats as on the Date executed on the Agreement

The above is the beneficial provision to the promoters.

The conditions in the case of 1%/5% i.e., Affordable and Non-Affordable Housing projects.

1. ITC will not available

2. 80% of Inputs and input services used in supplying the services shall be purchased from registered persons. In case of shortfall, RCM u/s 9(4) @ 18 %. However, the rate of cement is 28%.

3. Moreover, GST on capital goods shall be paid by the promoter on a reverse charge basis, u/s 94(4) of the CGST act at the applicable rates.

| Sl.no | Particulars | Can we buy from Registered Dealer | % share(approx.) |

| 1 | Cement | Yes | 20 |

| 2 | Iron | Yes | 15 |

| 3 | Sand | No | 20 |

| 4 | Bricks

(Mud or Cement) |

Yes | 10 |

| 5 | Manpower | Yes, when the labor from Manpower Agency | 20 |

If any builder purchases from unregistered dealer, then Gst has to be paid @ 28%.

Taxation under Income tax

The Taxability of JDA in the hands of the developer is under business income and in the hands of the landowner is under Capital Gains.

Determination of date of Transfer:

Capital Gains arising on the “transfer” of a capital asset. As per Section 2(47) of the Income Tax Act 1961, the word “transfer” amongst other things includes:

“any transaction involving the allowing of the possession of any immovable property to be taken or retained in part performance of a contract of nature referred to in section of the Transfer of Property Act, 1882 (4 of 1882)”

This clause gave a deemed effect of the transfer on the satisfaction of the following conditions:

1. There should be a contract for consideration in writing and the same should be signed by the transferor;

2. The contract should be for transfer of immovable property;

3. The transferee should have taken possession of the property and has done something for the furtherance of the contract;

4. The transferee should be ready and willing to perform his part of the contract; and

5. In this case, even without execution of sale deed, the transferee acquires the right in the property and the transferor cannot claim any right in respect of the property under consideration other than the rights expressly provided in the terms of the contract.

The assessing officers contended that the date of execution of the JDA was the date of transfer of the capital asset. However, it is worth noting that on the date of execution of the JDA, the landowner has not liquidated the land and has no funds to pay the taxes, and hence this appeared irrational and hence led to litigation. Further, in the absence of funds, the landowner was also unable to claim the benefits under the Section 54 series, causing genuine hardship to the assesses.

Determination of Consideration:

Considering that the landowner is required to pay the taxes on the date of execution of JDA, the biggest question is that when the project is just on the JDA with no real existence, what will be a consideration. For this purpose, I would like to draw attention to Section 50D of the Income Tax Act, 1961, which says,

“Where the consideration received or accruing as a result of the transfer of a capital asset by an assessee is not ascertainable or cannot be determined, then, for computing income chargeable to tax as capital gains, the fair market value of the said asset on the date of transfer shall be deemed to be the full value of the consideration received or accruing as a result of such transfer.”

Now, this section leads to even more confusing considering that fact that the projects under JDA run for an average 2 to 3 years and that the prices of real estate are subject to fluctuation, how could one determine apt fair market value on the date of execution of JDA?

What Is The Change?

The Budget 2017, has provided a ramping revolution in the taxability of JDAs putting an end to the ever-existing disputes. The proposed amendments are:

Determination of date of Transfer:

A new sub-section (5A) in section 45 is proposed to be issued to shift the capital gain arising on JDA to the previous year in which the certificate of completion for the whole or part of the project is issued by the competent authority in case of an assessee being individual or Hindu undivided family provided the assessee does not transfer his share in the project to any other person on or before the date of issue of said certificate of completion.

Determination of Consideration:

It is proposed to provide that the stamp duty value of land or building or both, in the project on the date of issuing of said certificate of completion given to the landowner as increased by any monetary consideration received, if any, shall be deemed to be the full value of the consideration received or accruing as a result of the transfer of the capital asset.

Tax Deduction at Source:

A new section 194 – IC is introduced to provide that in case any monetary consideration is payable under the specified agreement, tax at the rate of ten percent shall be deductible from such payment.

CONCLUSION:

These amendments are removing the considerable hardship faced by the assessees and are a welcome step that will improve the sentiments of the developers and landowners leading to an increase in the supply of land to developers. Hope these amendments will numb the pain of demonetization, the hit the real estate transaction hard.

Author Bio