Foreign Contribution

Individuals, Associations and Non-Profit Companies intending to receive the funding in India from foreign source are needed to comply with and are subject to the regulations made by government in this regard.

Earlier Foreign Contribution (Regulation) Act 1976 (FCRA, 1976) was in force to regulate and facilitate the acceptance and utilization of foreign contribution. After that, Foreign Contribution (Regulation) Act, 2010 (FCRA, 2010) has came into force with effect from 1 May, 2011 as an improvement over the existing FCRA 1976 and with wider applicability. This FAQ has been prepared to give brief idea about the legal compliances for receiving foreign funding.

Q 1.What is FCRA 2010 ?

Foreign Contribution (Regulation) Act, 2010 is an act to consolidate the law to regulate the acceptance and utilization of foreign contribution by certain individuals or associations or companies and to prohibit acceptance and utilization of foreign contribution for any activities detrimental to the national interest and incidental matters.

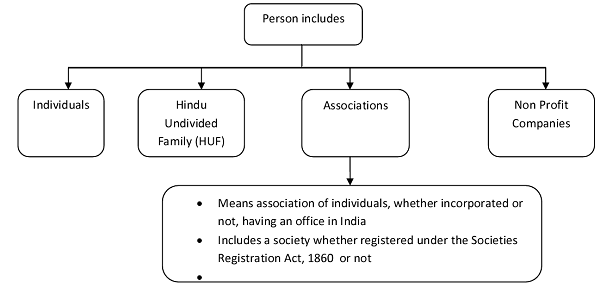

Q 2. What is Foreign Contribution?

Foreign Contribution means contribution and donation made by foreign source of :

- Any article ( except an article given to a person as a gift for his personal use having market value in India not more than Rs. 25000/-)

- Any currency, whether Indian or foreign

- Any security including foreign security as defined in Foreign Exchange Management Act 1999

Q 3. What is foreign source?

Foreign source includes :

- Government of any foreign country and any agency thereof

- Any international agency excluding the agencies specified by the Central Government

- A foreign company

- A corporation incorporated in a foreign country

- Multi- national corporation defined in FCRA, 2010

- A trade union in any foreign country

- A foreign trust or foundation

- A citizen of foreign country

- A society, club or other association formed or registered outside India

- A Company registered in India and more than half of share capital is held by-

- Government of a foreign country

- Citizens of a foreign country

- Corporations incorporated in a foreign country

- Trusts, societies or other associations formed or registered in a foreign country

- Foreign company

Q 4. What is foreign Security?

Foreign Security means any security in the form of shares, stocks, bonds, debentures or any other instrument denominated or expressed in foreign currency and securities expressed in foreign currency but where redemption or any other form of return such as interest or dividends is payable in Indian currency.

Q 5. Who can accept Foreign Contribution?

A person having a definite cultural, economic, educational, religious or social programme can accept foreign contribution after getting registration or prior permission from the Central Government.

Q 6. Who cannot accept Foreign Contribution?

- Election candidate

- Member of any legislature (MP and MLAs)

- Political party or office bearer thereof

- Organization of a political nature

- Correspondent, columnist, cartoonist, editor, owner, printer or publishers of a registered Newspaper.

- Judge, government servant or employee of any corporation or any other body controlled on owned by the Government.

- Association or company engaged in the production or broadcast of audio news, audio visual news or current affairs programmes through any electronic mode

- Any other individuals or associations who have been specifically prohibited by the Central Government

Q 7. How can foreign contribution be accepted?

Foreign contribution can be accepted only by taking the permission of the Central Government. Such permission can be taken in the following two ways:

Ways:

- Registration (Regular)-Shall be valid for a period of 5 years and need to be renewed.

- Prior Permission (Adhoc)-Shall be granted for specific amount from a specific donor for specific purpose

Q 8. What is the eligibility criteria for grant of registration?

The Association:

- must be registered (under the Societies Registration Act, 1860 or Indian Trusts Act 1882 or section 8 of Companies Act, 2013 etc.)

- normally be in existence for at least 3 years.

- has undertaken reasonable activity in its field for the benefit of the society.

- Has spent at least Rs.10,00,000/- (Rs. ten lakh) over the last three years on its activities. (Statements of Income & Expenditure, duly audited by Chartered Accountant, for the last three years are to be submitted)

Q 9. What is the eligibility criteria for grant of prior permission?

An Association, which has not completed 3 years of existence, is not eligible for grant of registration. Such organization may apply for grant of prior permission. For this, the Association:

- must be registered (under the Societies Registration Act, 1860 or Indian Trusts Act 1882 or section 8 of Companies Act, 2013 etc.)

- should submit a commitment letter from the donor indicating the amount of foreign contribution and the purpose

- should submit copy of a reasonable project for the benefit of the society for which the foreign contribution is proposed to be utilized.

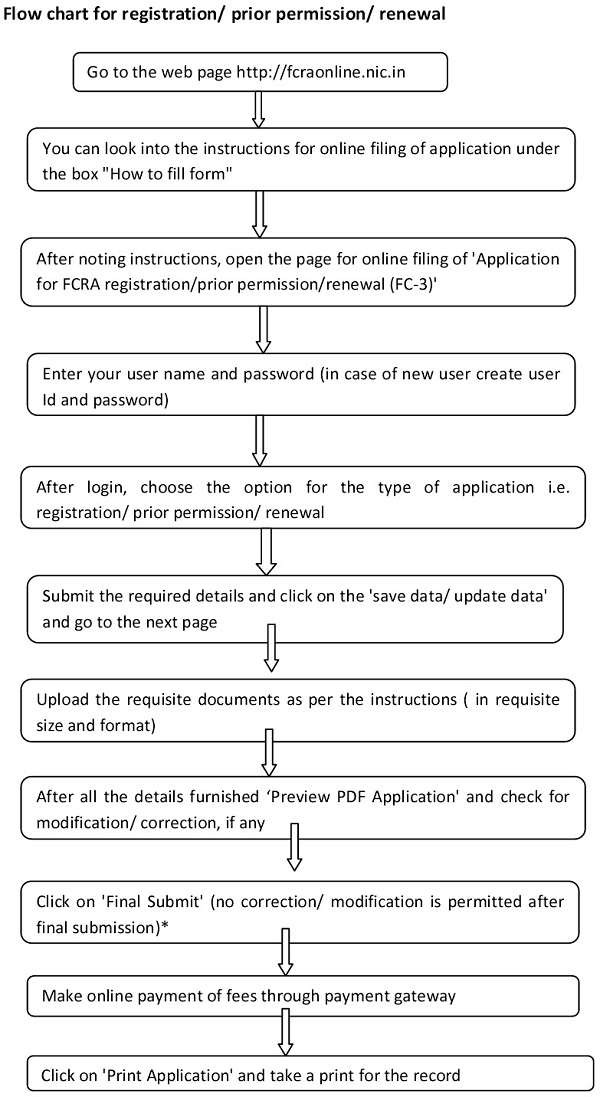

Q10. What is the process for registration/ prior permission?

Following steps are to be followed:

- An application in prescribed form must be submitted online using FCRA online services.

- For this user Id and password is created.

- After creating user name and password, details are furnished as per the requirement and relevant documents are attached.

- After that application is finally submitted along with requisite documents and online fee is paid.

- Ministry of Home Affairs is supposed to grant registration/ prior permission within 90 days from the date of receipt of complete application.

Q11. What are the documents to be submitted for the grant of registration?

Following documents should be submitted for grant of registration:

- Self certified copy of registration certificate (registered as Society, Trust, Section 8 Company etc.)

- Self certified copy of Memorandum and Article of Association/ Trust deed etc.

- Activity report indicating details of activities during the last three years

- Copies of audited statement of accounts for the past three years

- If functioning as editor, printer or publisher of a publication, a certificate from the Registrar of Newspapers

- Image of Chief Functionary’s signature

- Image of the Seal of the Association

Q12. What are the documents to be submitted for the grant of prior permission?

Following documents should be submitted for grant of prior permission:

- Self certified copy of registration certificate

- Self certified copy of Memorandum and Article of Association/ Trust deed etc.

- Copy of commitment letter from foreign donor specifying the amount of foreign contribution and the purpose for which it is to be given

- Copy of the project report for which foreign contribution is solicited and is proposed to be utilized

- If functioning as editor, printer or publisher of a publication, a certificate from the Registrar of Newspapers

- Image of Chief Functionary’s signature

- Image of the Seal of the Association

Q13. Whether contributions given by Non- Resident Indians (NRIs) holding valid indian passport, i.e. Indian citizenship, is treated as foreign contribution?

No, Contribution made by a NRI holding valid indian passport from his personal savings/ earnings is not treated as foreign contribution.

Q14. Whether donation given by an individual of Indian origin and having foreign nationality is treated as ‘foreign contribution?

Yes, Donation from an Indian who has acquired foreign citizenship is treated as foreign contribution.

Q15. Whether foreign remittances received from a relative are to be treated as foreign contribution?

No, However in case foreign contribution received in excess of rupees one lakh or equivalent in a financial year from any of the relatives, information to the Central Government in Form FC-1 within thirty days from the date of receipt of such contribution will be given.

Q16. What can be accepted as Foreign Contribution even by the persons otherwise prohibited from accepting foreign contribution?

Persons otherwise prohibited can accept foreign contribution:

- By way of salary, wages or other remuneration or by way of payment in the ordinary course of business in India by foreign source

- By way of payment in the ordinary course of business transacted outside India

- As an agent of foreign source in relation to any transaction with the Central Government or State Government.

- By way of a gift or presentation as a member to any Indian delegation

- From his relative

- By way of remittance received in the ordinary course of business

- By way of any scholarship, stipend or any payment of like nature

Q17. Whether an association should open an exclusive foreign currency A/c before submission of an application for registration or prior permission?

Yes, since the foreign currency A/c through which foreign contribution is proposed to be received and utilized is to be mentioned in the application seeking registration or prior permission, therefore the association should open such account with the Bank before submission of application.

Q18. What is the validity period of registration granted?

Registration granted under FCRA 2010 is valid for a period of 5 years from the date of its issue and it will be renewed six months before the date of expiry of said period. However in case of ongoing multi-year project, application for renewal shall be made twelve month before the date of expiry of registration.

Q19. What is the procedure for renewal of registration?

- An online application in Form FC -3 is to be made for renewal of registration

- Requisite details are furnished and following documents are attached:

- Self certified copy of registration certificate

- Self certified copy of Memorandum and Articles of Association/ Trust Deed

- Self certified copy of FCRA Registration certificate issued by Ministry of Home Affairs

- Image of seal of Association

- Image of signature of Chief Functionary

- After the application is finally submitted, a fee of Rs. 500/- is to be paid online through payment gateway.

- After that application is dealt with by the Ministry of Home Affairs and renewal of registration is granted.

Q20. What are the consequences of non submission/delay in submission of renewal application?

In case an application for renewal of registration is not submitted or made after the due date, validity of registration is deemed to have ceased from the date of completion of period of 5 years from the date of grant of registration and application for the fresh registration will be made.

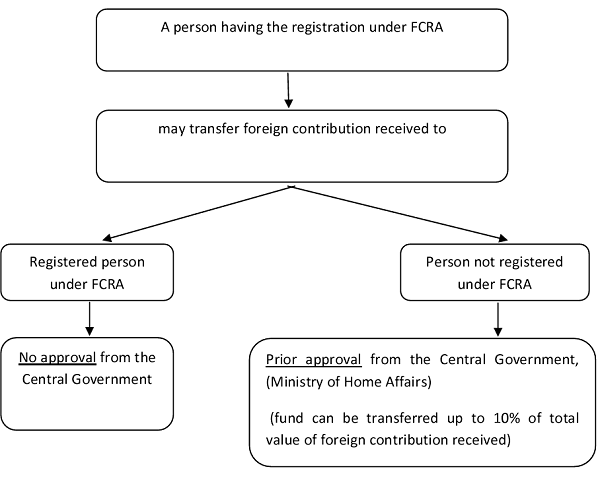

Q21. How can the foreign contribution be transferred from one person to another person?

Q22. Can foreign contribution be received in Indian rupees?

Yes, any amount received from ‘foreign source’ in Indian rupees or foreign currency is construed as ‘foreign contribution’. Such transactions even in Indian rupees term are considered foreign contribution.

Q23. What is the method for accounting under FCRA, 2010?

There is no specific method of accounting prescribed under FCRA act and rules. However separate set of accounts and records will be maintained for the foreign contribution received and utilized.

Q24. What are the reporting/ filing requirement under FCRA, 2010?

- Online submission of Annual Return in Form FC- 4 along with income and expenditure statement, receipt and payment account and balance sheet, duly certified by a Chartered Accountant, for every financial year within 9 months from the closure of the financial year.

- Nil return is also to be filed in case no foreign contribution is received /utilized during the year.

- Intimation of quarterly receipt of foreign contribution within 15 days from the last day of the quarter in which it is received.

- Online intimation about opening of Utilization Bank Account(s) within 15 days of opening of such account(s)

- Online intimation regarding change in details of association within 15 days of such change.

Q25. Can foreign contribution be received in and utilized from multiple bank accounts?

Foreign contribution can be received/deposited in the exclusive designated Foreign Currency account of a bank, as mentioned in the order for registration or prior permission granted by Ministry of Home Affairs.

However, one or more accounts in one or more banks may be opened for utilizing the foreign contribution after it has been received.

Q26. Can foreign contribution be mixed with local receipts?

No, Foreign contribution cannot be deposited or utilized from the bank account being used for domestic funds.

Q27. What are the reporting requirement in case of change in details of association registered with the FCRA department?

Intimation will be given online in Form – 6 within 15 days of change in details. Intimation will be given in the following cases:

- Change in name of association or its address

- Change of objects, aims, nature and registration with relevant authorities.

- Change in bank/ branch of the bank and/or designated foreign contribution account number

- Change in key members of the association if such change causes replacement of fifty percent or more of the key members

Q28. Whether interest or any other income earned from foreign contribution be considered foreign contribution?

Yes, It will be shown as fresh foreign contribution receipt during the year in which it is earned and can be utilized for the activities/projects of the Association.

Q29. Whether infusion of foreign share capital in a company registered under section 8 of the Companies Act, 2013 (Non- profit Company) attracts the provisions of FCRA, 2010?

Yes, infusion of foreign share capital in a non- profit company is treated as foreign contribution.

Q 30. Is it mandatory for an Association to have registration under section 80G or 35 AC of Income Tax Act, 1961 to be eligible for getting registration or prior permission under FCRA, 2010

No, It is not mandatory to have registration under Income Tax Act, 1961 for seeking registration or prior permission under FCRA, 2010

Q31. Can an Association utilize the foreign contribution for any purpose?

No, Foreign contribution should be utilized only for the purposes for which it is received.

Q32. Is there any ceiling for the administrative expenses to be incurred?

Yes, Association should not incur more than 50 percent of the foreign contribution received in a financial year to meet administrative expenses. However more than 50 percent of such foreign contribution may be incurred with prior approval of the Central Government.

Q33. Can an Association use the foreign contribution for investment in mutual funds and other speculative investments?

No, the use of foreign contribution or any income derived there from is not allowed to be invested in mutual funds or any speculative business.

*No need to submit the copy of the online application in physical form to the Ministry of Home Affairs.

Disclaimer: This article has been prepared in good faith on the basis of information available on the date of publication without any independent verification. The Author does not guarantee or warrant the accuracy, reliability, completeness or currency of the information in this publication nor its usefulness in achieving any purpose. The Author will not be liable for any loss, damage, cost or expenses incurred or arising by reason of any person using or relying on information in this publication. Readers are requested to consult a professional before taking any action.

(Author – Sonika Bharati, FCS, LLB, is a Company Secretary in Practice from Delhi and can be contacted at sonika@akgadvisory.com)

Author Bio

What forms to be produced for donation received from foreign countries. They asked us to produce form 35 1 & 2.

Please explain any forms are available for the above 35 1 & 2

Magesh

What forms to be to produce for donation received from Foreign countries for Charitable Trust in india.

whether any form is available in the name of 35 1 & 2

Magesh

Should an individual receiving donations from NRI for medicial reasons, still require prior government approval?

Thanks for your nice interpretation of Foreign contribution.

Whether reimbursement from overseas party towards expenses made in FC from India would be treated as foreign contribution ?

Hello, Nice Article

Is FCRA registration is required by the trust registered u/s 12A , for receipt of money as per will of a NRI trustee (Foreign citizen of Indian Origin). The NRI was also the founder of Indian trust.

What is the procedure for Indian organization (non-profit) to transfer FCRA money to an entity (non-profit) based outside India?

Very nicely explained. Thanks.

I still have a query regarding foreign currency donation received in donation boxes. What is to be done with that. Since it is voluntary undisclosed donation whether it is covered under FCRA or can be deposited in any bank account.

Thank you so much for detailed study on FCRA.

It would be nice if you clear my small doubt. Can a sec 8 company registered under GST receive ‘income’ from foreign person for service rendered by sec 8 company. The company as of now don’t have FCRA.

In FC-4 It is asking details of donation from Foreign Source and local source .My question is which donation we should so under local source..plz clear this

Thanks a lot for the very nice article on FCRA.

but I have still a query regarding filing of quarterly FCRA Return. Pls help me to resolve

Q21. How can the foreign contribution be transferred from one person to another person?

A person having the registration under FCRA, may transfer foreign contribution received to

a) registered person under FCRA

b) unregistered person under FCRA

now whether (a) registered person under FCRA, will report his receipt in quarterly FCRA Return?

If yes then

which remitter’s name (main foreigner or Indian NGO) to be shown in FCRA Return?

It was very helpful Article . From above given Article I got all required details regarding FCRA 2010.

Thanks for above article.

Thank you Sonika, I understand a lot with this article, even though I have some queries :

1, can a profit oriented company to receive foreign contribution for the betterment of the society (spend to the needy people).

Sonika article is very good, but have some queries

1. Is there any provision of penalty for non intimation of quarterly report.

2. qtrly return and intimation are one and the same,

3. how to intimate for past quarter if we failed to upload quarterly intimation

4. Bank account utilisation means, only after receipt of fund correct.

Please reply.

Very Helpful Article. In depth Information. Thanks a lot for sharing the knowledge.