The monthly Newsletter – encompasses MCA notifications issued in the month of February 2020, informal Guidances given by SEBI on SEBI SBEB , Takeover and Insider Trading Regulations and NCLT judgement in Videocon Insolvency case.

Independent Directors who could not get themselves registered on IICA databank can rest easy. The deadline for registration has been extended by further 2 months i.e. upto 30 April 2020 . Further even if Directors have served as Director/ KMP for more than 10 years in a Body Corporate listed on a recognized stock exchange will be exempted from online proficiency test.

Noteworthy amendment is that MCA has released Companies (Auditor’s Report) Order, 2020, (CARO) to enhance due diligence and disclosures by auditors and bring greater transparency into the financial affairs of companies. Statutory Auditors will now have to additionally report on benami transactions, default in borrowings, comment on internal audit system, cash losses, CSR compliance, qualifications in audit report of subsidiaries (in Consolidated financial statements), utilisation of funds raised through IPO/ private placement and complaints received from whistle blowers. These will need to be included in Audit report for year ended 31st March 2020. This will put greater onus on companies to share information with the auditors.

While some Corporates are still recovering from the hangover of the proposed amendments by SEBI pertaining to Related Party Transactions posing serious threat of onerous compliances and administrative challenges in implementation, the Regulators have invited comments through consultation / discussion papers on Enhancement of Audit Standards to ensure more transparency in reporting by Auditors and Takeover Regulations to enable acquisition through bulk and block deals during open offer period.

Aside to above, there have been few generic amendments in the Month of February 2020 by the Regulators.

The key synopsis of some of the other highlights in this month are:

> Consultation paper on Audit Independence and Accountability – MCA has invited comments of the Public with respect to amendments to Companies Act, 2013 with respect to Audit independence and accountability. The key points on which MCA has sought industry’s suggestions and affecting the companies, are as under:

-

- The list of restricted non-audit services by Auditors

- Whether Joint Audit should be made mandatory for big companies

- Whether comment of Holding Company’s auditor on account of subsidiary companies should be made mandatory

- Concurrent Audit for big listed companies

- Unlisted company whose parent company is a listed company will also require submitting quarterly returns to SEBI

- Resignation of Auditors – Is the process prescribed for auditors of listed companies (to complete audits for the previous quarter if resigned before 45 days and for the following quarter if resigned after 45 days) to be followed for other large companies.

> Companies (Incorporation) Amendment Rules, 2020 – MCA with an aim to reduce time and cost of starting business in India has introduced Form SPICe+ which integrates 10 procedures of incorporation in single web form (including opening bank account, EPFO registration) and facilitates on-screen filing and real time data validation for seamless incorporation of Companies

> NCLT orders inclusion of Videocon’s overseas assets in insolvency – NCLT has lifted the Corporate veil between Videocon Industries Limited (“VIL”) and its overseas companies which was formed as special purpose vehicles only to ostensibly hold the foreign oil and gas assets, properties and interests therein. NCLT has passed an order instructing that all the assets of the foreign oil and gas business held by the Group’s foreign arms was in fact the assets and property of the VIL and that the same be included in the process of Insolvency.

- RBI extends one time re-structuring of MSME advances upto 31 Dec 2020.

Newsletter Preparation Team- Brijbala, Ruchie, Archana, Pooja

INDEX

| Sr. No. | Law/section/rule/regulation amended | Amendments -Snapshot | Date |

| Ministry of Corporate Affairs (“MCA”) ORDERS | |||

| 1. | The Companies (Auditors Report) Order, 2020 (“CARO Report 2020”) | MCA introduces new CARO Report 2020 whereby stricter disclosure norms have been prescribed for reporting by Auditors. | 25 February 2020 (yet to be published in Official Gazette) |

| 2. | Consultation Paper on “Enhancement of Audit Independence and Accountability” | MCA to enhance Audit Independence and Accountability viz. Non-Audit services not to be taken by Auditor, Joint Audit mandatory, Comment of Holding Cos. Auditor on Subsidiary Cos report, resignation of auditor etc ., invites suggestions on Consultation | 15 March 2020

(Last Date of receiving Public Comments) |

| B. SECURITIES AND EXCHANGE BOARD OF INDIA (“SEBI”) UPDATES | |||

| 1. | Discussion Paper on “SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011” (SAST Regulations)

|

SEBI invites comments for amending SAST Regulations, proposes following:

a. Completion of acquisition through bulk and block deals during the open offer period; b. Depositing 100% escrow in case of open offers made pursuant to indirect acquisitions; and c. Payment of interest in case of delay in open offers |

2 March 2020 (Last Date of receiving Public Comments) |

| 2. | SEBI (Issuing Observations On Draft Offer Documents Pending Regulatory Actions) Order, 2020 | SEBI introduces new order whereby instances, process and timelines for issuing observations in respect of draft offer documents being filed by entities on whom regulatory action is pending, have been prescribed. | 5 February 2020 |

| 3. | Regulation 79 of Securities and Exchange Board of India (Depositories and Participants) Regulations, 2018

|

The procedure prescribed under Regulation 79 of the said regulations, for creation of pledge, shall also be followed in case of re-pledge of securities for margin and/or settlement obligations of beneficial owner. | 24 February 2020 |

| 4. | Consultation Paper on ‘Regulatory Framework for Corporate bonds and Debenture Trustees”

|

SEBI invites comments from the Public to strengthen framework for Corporate bonds, securing interest of Debenture Holders, enhancing the role of Debenture Trustees | 17 March 2020 (Last Date of receiving Public Comments) |

| C. SEBI INFORMAL GUIDANCES | |||

| 5. | SEBI (Buy-back of Securities) Regulations 2018 | Infosys Limited – Issue of shares pursuant to completion of one year of Vesting of RSUs but prior to the one year from the end of Buyback Period as Issue of shares was considered as subsisting obligation in Buyback Regulations. | 3 February 2020 |

| 6. | SEBI (Share Based Employee Benefits) Regulations, 2014 | JSW Limited – Applicability of SEBI (Share Based Employee Benefits) Regulations, 2014 to Joint Ventures and Promoter Controlled Entities. | 5 November 2019 |

| 7. | SEBI (Prohibition of Insider Trading) Regulations, 2015 and SEBI (Substantial Acquisition of Shares and Takeovers) Regulation, 2011 | Shri Dinesh Mills Limited – Restriction of contra trade under SEBI PIT Regulations will apply to inter-se and off market transfer amongst Promoter/Promoter Group entities, even though exempted from open offer under the SEBI Takeover Regulations. | 4 November 2019 |

| D. NATIONAL COMPANY LAW TRIBUNAL ORDERS (“NCLT”) | |||

| 1. | Insolvency and Bankruptcy Code, 2016 | NCLT orders inclusion of Videocon’s overseas assets in insolvency process | 12 February 2020 |

| E. MCA UPDATES | |||

| 1. | Notification of Section 230(11) and 230(12) of the Companies Act, 2013 | New rules for takeover of unlisted companies

– Takeover offers in case of unlisted companies can be made through Scheme of compromise or arrangement, while in case of listed companies, takeover offers must be made as per regulation prescribed by the Securities and Exchange Board of India. |

3 February 2020 |

| 2. | The Companies (Compromises, Arrangements and Amalgamations) Amendment Rules, 2020 | – An aggrieved party having grievances with respect to the takeover offer of unlisted companies can make an application to Tribunal in the prescribed manner. | 3 February 2020 |

| 3. | The National Company Law Tribunal (Amendment) Rules, 2020 | – Prescribed a mechanism and the process for the above by making suitable amendments to the rules framed there under. | 3 February 2020 |

| 4. | The Companies (Incorporation) Amendment Rules, 2020 | New integrated web-based incorporation process – Form SPICe+

SPICe+ Integration of 10 procedures in single web form RUN – Application of Change of name AGILE-PRO – Enabling Employees’ Provident Fund Organisation (EPFO) Registration, Profession Tax Registration and Opening of Bank Account |

23 February 2020 |

| 5 | Insolvency Bankruptcy Code, 2016 | MCA allows Insolvency Professionals to file eforms on MCA portal

To enable companies undergoing insolvency resolution process to comply with statutory compliances |

17 February 2020 |

| 6. | The Companies (Issue of Global Depository Receipts) Amendment Rules, 2020 | MCA amends Companies (Issue of Global Depository Receipts) Rules, 2014 replacing the term “abroad” with “convenient jurisdiction”

MCA has amended the Rules allowing proceeds from GDR issue can be remitted in an International Financial Services Centre Banking Unit. |

13 February 2020 |

| 7. | The Nidhi (Second Amendment) Rules, 2020 | Time-limit for companies to declare themselves as Nidhi’s, incorporated/ functioning prior to 15 August 2019, extended to 14 May 2020 | 14 February 2020 |

| 8. | The Companies (Registration Offices and Fees) Amendment Rules, 2020 | Form GNL-2 substituted by delete tabs for filing of circular for inviting Deposits, return of deposits and declaration of solvency as specific e-forms has been prescribed. | 18 February 2020 |

| 9. | MCA Circular – Extension of last date of filing IND AS complaint Financial Statements by NBFC

|

Last date of filing e-forms AOC-4 NBFC (Ind AS) and AOC-4 CFS NBFC (Ind AS) by NBFC’s without additional fees has been extended to 31 March 2020 | 30 January 2020 |

| 10. | MCA Circular – Extension of last date of filing e-forms pertaining to Annual Return and Financial Statements by Companies in the jurisdiction of J&K and Ladakh. | Last date of filing e-forms without additional fees has been extended to 31 March 2020 | 31 January 2020 |

| 11. | Companies (Appointment and Qualification of Directors) Amendment Rules, 2020 | Extended the due date for mandatory registration of Independent Directors on IICA data bank to 30 April 2020

Additional Criteria for exemption from proficiency test |

|

| F. OTHER REGULATORY UPDATES | |||

| 1 | Indian Institute of Corporate Affairs(IICA) Updates | Fees for 5 years and Lifetime Membership notified for Registration of Independent Director on Databank | |

| 2 | BSE Guidance and FAQs on Regulation 32 of the SEBI (LODR) Regulations, 2015 | BSE releases guidance and FAQ on submission of Statement of Deviations | |

A. MCA Orders

♦ MCA notifies New CARO Report 2020 – (yet to be published in the Official Gazette)

SYNOPSIS

In supersession of the existing CARO Report Order 2016, MCA has notified and introduced a new CARO Report Order 2020 after consultation with the National Financial Reporting Authority, wherein all the existing clauses are there, some new clauses are added and some are amended. Further there are various reporting requirements on the auditor now.

The CARO Report 2020 shall be applicable for the financial years commencing on or after the 1 April 2019;

– not apply to the auditor’s report on consolidated financial statements except where subsidiary reports have qualifications/adverse remarks (clause (xxi) of paragraph 3 of CARO, 2020).

BRIEF OF AMENDMENTS

Details of difference in CARO Report 2020 and CARO Report 2016 is as follows:

| Sr. No. | CARO Report 2020 | CARO Report 2016 |

| 1. | Reporting of Company’s Property, Plant, Equipment and intangible assets is required | Reporting of all the Fixed Assets of the Company was required |

| 2. | Confirmation of physical verification of Property, Plant, Equipment by the Management of the Company and whether material discrepancy has been dealt in books is now required to be confirmed | Confirmation of physical verification of Fixed Assets of the Company by the Management of the Company and whether material discrepancy has been dealt in books was required to be confirmed |

| 3. | Format has been prescribed to provide details of title deeds not held in Companies name of all the immovable property (other than properties where the company is the lessee and the lease agreements are duly executed in favour of the lessee) | No such format was prescribed for under CARO Report 2016 |

| 4. | Reporting on revaluation of Property, Plant and Equipment’s by Company and specify the amount of change, if change is more than 10%. | No such reporting requirement was prescribed under CARO Report 2016 |

| 5. | Reporting of proceedings initiated or pending under the Benami Transactions (Prohibition) Act, 1988. | No such reporting requirement was prescribed under CARO Report 2016 |

| 6. | In case of physical verification of inventory conducted, a limit for reporting material discrepancies has been prescribed in the CARO Report 2020 i.e. which is 10% or more in the aggregate for each class of inventory. | No such limits for reporting material discrepancy was provided under CARO Report 2016 |

| 6. | Reporting of compliances if company was sanctioned working capital limits in excess of five crore rupees or more from banks or financial institutions | No such reporting requirement was prescribed under CARO Report 2016 |

| 7. | Reporting of compliances as prescribed for renewal or extension of loans and advances in the nature of loan, which has fallen due during the year | No such reporting requirement was prescribed under CARO Report 2016 |

| 8. | Reporting of transactions not recorded in the books of accounts but have disclosed the same as income in the income tax assessments of the Company |

No such reporting requirement was prescribed under CARO Report 2016 |

| 9. | Format has been prescribed to report Company’s default in the repayment of loans / other borrowings or in the payment of interest to any lender | No such format was prescribed for under CARO Report 2016 |

| 10. | Auditor to confirm on the following:

1. Whether the Company is declared willful defaulter by any Bank or Financial Institutions or lender; 2. Whether term loans was used for any other purpose and provide the details; 3.Whether funds raised on short term basis was used for long term purpose; 4. Whether any funds taken for its subsidiaries, joint venture and if taken, provide details; 5. Whether Company has raised loans during the year by pledging securities held in subsidiaries, joint venture or associate companies and provide details; 6. Whether the Company has conducted any Non-Banking Financial or Housing Finance activities without a valid Certificate of Registration from RBI 7. Whether the Company is Core Investment Company and compliance of the criteria and provisions as provided |

No such confirmations was required to be made by Auditor under CARO Report 2016 |

| 11. | Auditors are required to report all the instances of frauds on the Company and also confirm if any report under Section 143(12) of the Act has been filed in Form ADT-4 by Auditor | In CARO Report 2016, Auditors were restricted to report frauds done by the Company’s Officers and employees on the Company and were not required to confirm if report under Section 143(12) of the Act has been filed in Form ADT-4. |

| 12. | Auditor to consider whistle blower complaints, if any, received by Company in his audit | No such requirement was prescribed under CARO Report 2016 |

| 13. | In case of Nidhi Company, Auditor to confirm if there has been any default in payment of interest on deposits or repayments and provide details | No such requirement was prescribed under CARO Report 2016, for Nidhi Companies |

| 14. | Reporting on Company’s internal audit system and consideration of report Internal Auditor | No such requirement was prescribed under CARO Report 2016 |

| 15. | Reporting of cash losses incurred by the Company in current and immediately preceding financial year | No such requirement was prescribed under CARO Report 2016 |

| 16. | Reporting on resignation of the statutory auditors, if any, during the year and take into consideration the issues, objections or concerns raised by the outgoing auditors | No such requirement was prescribed under CARO Report 2016 |

| 17. | The auditor is required to render his opinion on the basis of the financial ratios, ageing of financial assets, payment of financial liabilities, etc., his knowledge of the Board of Directors and management plans, that no material uncertainty exists for the Company and that company is capable of meeting its liabilities existing at the date of balance sheet as and when they fall due within a period of one year from the balance sheet date. | No such requirement was prescribed under CARO Report 2016 |

| 18. | Reporting of compliances relating to transfer of unspent amount of CSR activities to the special account in compliance with Section 135 | No such requirement was prescribed under CARO Report 2016 |

| 19. | In case there is any qualification/ adverse remarks made by the respective Auditors in their respective CARO Reports of the Companies included in the consolidated financial statements, the Statutory Auditor of the Holding Company is required to mention the details of such Company and the qualification/adverse remark in their Audit Report. | No such requirement was prescribed under CARO Report 2016 |

–

| Law/section/rule/regulation amended | CARO Report 2016 |

| Effective date | Effective from the date of publication in the Official Gazette |

| Link to access | https://taxguru.in/company-law/caro-2020.html |

♦ MCA to enhance Audit Independence and Accountability, invites suggestions on Consultation Paper latest by 15 March 2020

SYNOPSIS

MCA has invited a consultation paper suggesting amendments to the Companies Act, 2013 with respect to Audit independence and accountability. The comments need to be provided by 15 March 2020. The key points on which MCA has sought industry’s suggestions and affecting the companies, are as under:

- Expansion sought in the list of restricted non-audit services by Auditors

- Joint Audit – Should it be mandatory for big companies

- Mandatory comment of Holding Company’s auditor on account of subsidiary companies

- Concurrent Audit for big listed companies (especially which have borrowings and inter-corporate loans and investments)

- Unlisted company whose parent company is a listed company will also require submitting quarterly returns to SEBI

- Resignation of Auditors – Is the process prescribed for auditors of listed companies (to complete audits for the previous quarter if resigned before 45 days and for the following quarter if resigned after 45 days) to be followed for other large companies.

BRIEF OF AMENDMENTS

| Sr. No | Concern | Existing Provisions | Suggestions sought by MCA |

| 1 | Economic concentration/ Oligopoly of audits of listed companies by “Big Four” Audit Firms | – | – What are the ways to remove such economic concentration?

– Should the number of audits/ number of partners under one audit firm/ Auditor be reduced? – Should the Auditors in listed – Whether the home grown Indian audit firms are equipped with the audit procedures, audit tools, manpower capacity to handle the audit of large organisations |

| 2 | Non-Audit Services not to be taken by Auditors | Sec 144 of CA 13 prohibits the following services directly or indirectly to company or its

(a) accounting and book keeping services; (b) internal audit; (c) design and implementation of any financial information system; (d) actuarial services; (e) investment advisory services; (f) investment banking services; (g) rendering of outsourced (h) management services; and (i) any other kind of services as may be prescribed. |

– What more non-audit services can be included in the list

– How the self-regulation among the auditors can be increased? |

| 3 | Joint Audit – Should it be mandatory for bigger companies?

|

No provision exists on mandatory conduct of Joint Audits, except Section 139 mentioning that Joint Auditors may not end their rotation simultaneously |

– Should it be mandatory for bigger companies?

– If so, what threshold? – Joint audits are mandatory in |

| 4 | Mandatory comment of Holding Company’s auditor on account of subsidiary companies?

|

Section 143(1) of the Companies Act, 2013 gives the auditor of a holding company the right of access to the records of all its subsidiaries and associate companies in so far as it relates to the consolidation of its financial statements with that of its subsidiaries.

Also SA 600-699 allows the auditor to use the work of others such as work of another Auditor, Internal Auditors, Auditor’s expert. |

– Whether the holding company’s auditor must also review the working papers of auditor of subsidiary and make mandatory comment on the account of subsidiary companies |

| 5 | Methodology for creation and maintenance of proposed panel of auditors – CAG/RBI/NFRA |

– Only approval of the Shareholders needed for appointment of an auditor | – Maintenance of panel of auditors for Non-Government Companies (Both Listed, Unlisted and Private Companies). What methodology can be adopted for creation of such panel of auditors? |

| 6 | Audit Engagement letter – where mandated and assessment of its utility and misuse. |

– | – To be filed with ADT-1 (appointment of Auditors) to see if the same is not in violation of section 144 of the Act i.e, Non-audit services are not there in audit engagement letter. |

| 7 | Utilisation of Borrowed funds – Concurrent Audit for big listed companies? | – No provisions on concurrent audit | – whether the concurrent audit is to be made mandatory in big listed companies

– what points should be included in the checklist to be developed in company audit in this regard. – What should be the threshold for big listed companies for this purpose? |

| 8. | Restriction on number of audit firms a group [Big 4] can have in whole of India. | – Whether number of audits under one audit firm/ Auditor be reduced? Whether the number of partners under/ one audit firm be reduced or fixed? | |

| 9. | Disclosure / requirement on Probability of default? – On the lines of Credit Rating Agencies

|

(SEBI) has introduced a “probability of default” mechanism to keep Credit Rating Agencies (CRAs) in check.

Rating companies, in consultation with the regulator, will now create a uniform probability of default benchmark for each rating category on their website, for one-year, two- year and three-year cumulative default rates, both for the short term and long term. According to the new framework, rating agencies have to assign the default probability to each rated debt instrument, and disclose its benchmark by December-end. |

– In order to reduce the NPAs and defaulters of loan payments, the suggestions are invited as to whether such kind of disclosures are required to be made by the Auditor in his Audit Report? If yes, in what manner? |

| 10. | Unlisted company whose parent company is a listed company will also require submitting quarterly returns to SEBI | No provision exists for submission of standalone accounts of subsidiaries of listed companies

|

Suggestions are invited as to whether unlisted company whose parent company is a listed company should also require submitting quarterly returns to SEBI. |

| 11. | Development of a ‘Composite Audit Quality Index’ to improve accountability of auditors and audit firms

|

In order to increase the quality of audit and have an objective mechanism to ascertain the quality, suggestions are invited on what qualitative and quantitative parameters should be included in such an index, how they should be measured, and which all companies should this be mandated for. What should be the thresholds for such companies? | |

| 12. | Strengthening Deterrence of conducting improper audits by inspection of audit engagements

|

Feasibility and mechanism of this inspection of audit engagements, manner and basis of selection of companies for such an inspection, agency which must undertake the same, whether audit firm level inspections also may be incorporated in this etc. | |

| 13. | Resignation of auditors | ICAI – Implementation Guide on Resignation/ Withdrawal from an Engagement to Perform Audit of Financial Statements – guidance on various aspects of auditors’ resignation like circumstances leading to withdrawal/ resignation, procedure to be followed by auditors in case of resignation, auditor’s responsibilities, professional obligations to be complied with by auditors.

Auditing standards also provides for the situation/ circumstances under which an auditor can resign or withdraw from the audit engagements. The circumstances in which the Auditors may withdraw/resign from the audit engagements are given in different paragraphs of SQC 1, SA 200, SA 210, SA 240, SA 250, SA 260(Revised), SA 315, SA 580, SA-705 (revised), SA 706(Revised), SA 720 (Revised) and Code of Ethics. Further, section 143(9) of the Act makes it mandatory for auditors of companies to comply with the Standards of Auditing issued by the ICAI. SEBI (for listed companies) – sub-clause (7A) of Clause A in Part A of Schedule III of SEBI LODR Regulations

CA 13 (for all companies) Auditor who has resigned from the company is required to file a statement with the company and the Registrar in ADT-3 within 30 days from the date of resignation. The reasons for resignation are also required to be disclosed in the ADT-3 for resignation |

Whether the aforesaid conditions as laid down by SEBI and ICAI should also be made mandatory for the auditors of other companies/ bigger companies

|

–

| Law/section/rule/ regulation amended | Consultation Paper by MCA on “Enhancing Audit Independence and Accountability” |

| Due date of submission of Comments | 15 March 2020 |

| Link to access | https://taxguru.in/company-law/mca-proposes-amendments-enhance-audit-independence-accountability.html |

B. SECURITIES AND EXCHANGE BOARD OF INDIA (“SEBI”) UPDATES

♦ SEBI invites comments on amendments in SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 (‘SAST Regulations’) latest by 2 March 2020

SYNOPSIS

Amendments proposed by SEBI in the SAST Regulations are here under:

- SEBI has proposed to allow completion of acquisition through bulk and block deals during the open offer period.

- In case of indirect acquisition under the SAST Regulations, it is proposed that an amount of 100 percent of the consideration payable under the open offer shall be deposited two working days before the date of detailed public statement.

- In case of delay in the open offer, the acquirer may be required to pay interest rate of 10 percent per annum in respect of indirect acquisitions. It is proposed that the revised open offer price may be calculated after addition of interest (10%) and the revised offer price is paid to all the shareholders.

BRIEF ANALYSIS

Regulation-wise background and proposal is summarised herein below:

| Sr. No | Regulation No. | Background | Proposal |

| Completion of acquisition through bulk and block deals during the open offer period | |||

| 1 | 22 (1), 22(2) and 22(2A) | Acquisition pursuant to an Agreement

As per Regulation 22(1) and 22(2), an Acquirer is not permitted to complete the transaction (i.e. the acquisition of shares or voting rights in, or control over the target company) triggering the open offer until expiry of the open offer, except : a. Acquirer depositing 100% of the offer size in escrow in cash; and b. After expiry of 21 working days from the Detailed Public Statement (“DPS”) Acquisition pursuant to Stock Exchange Settlement process As per Reg 22(2A), an acquirer was permitted to acquire shares of the target company through preferential issue or through the stock exchange settlement process, other than through bulk deals or block deals, subject to: (i) such shares being kept in an escrow account, (ii) the acquirer not exercising any voting rights over such shares kept in the escrow account An acquisition through an Agreement, executed through block deal on the stock exchange platform is more transparent than the off-market route. Hence the prohibition mentioned in Reg 22(2A) has created confusion. Block deals (Rs 10 crores or more) and Bulk Deals (0.5% of the total paid up value) are regulated, settled through stock exchanges and have reporting requirements. |

Allow completion of acquisition through bulk and block deals during the open offer period through appropriate amendments, as they are more transparent, regulated & settled through Stock Exchanges and have reporting requirements.

The existing FAQ in this regard may also be deleted. Benefits of permitting completion of acquisition through block deals and bulk deals is as follows: 1. Acquirer will be able to directly acquire significant stake in target company through stock exchanges instead of off-market 2. Process of Acquisition will be completed quickly instead of placing small orders for long times with appropriate checks and balances as prescribed under Reg 22(2A) |

| Depositing 100% escrow in case of open offers made pursuant to indirect acquisitions | |||

| 2. | 13(2)(e) | Provisions of Regulation 22 allow acquirers to take control over the target company during the offer period itself subject to expiry of 21 working days from the date of after date of DPS if the acquirer deposits 100% of consideration payable in cash.

Pursuant to provisions of Reg 13(4), a relaxation is provided for making DPS, whereby it mentions that it shall be made not later than 5 working days after the completion of primary acquisition and hence, an acquirer acquires indirect control over the Target Company. Hence, primary acquisition, which would result in indirect acquisition of the target company, can be completed before the publication of DPS. The Acquirer acquires control over the Target Company before the date of DPS and is not required to deposit 100% of the consideration payable under the open offer in the escrow account Hence, Takeover Regulations have stricter compliances w.r.t deposit of money in escrow account for direct and deemed direct acquisitions, as compared to indirect acquisitions, if the acquirer wants to complete the acquisition prior to the end of the open offer period. |

In case of indirect acquisition, public announcement of an open offer made in terms of Reg 13(2)(e), an amount of 100% of the consideration payable under the open offer must be deposited 2 working days before the date of Detailed Public Statement; i.e. 100% cash in escrow account in case of indirect acquisitions

Regulations should not differentiate between direct acquisitions and indirect acquisitions when providing safeguards for shareholders who wish to avail the exit opportunity provided by an open offer |

| Payment of Interest in case of delay in open offers | |||

| 3 | 18(11) | As per Regulation 18(11) of the SAST Regulations, only delays with respect to non-receipt of statutory approvals has been envisaged. However, the open offers are delayed on account of other reasons as enumerated below, which are presently not envisaged in the Takeover Regulations:

(i) inter-se dispute among parties to the agreement; (ii) valuation disputes; (iii) investor complaints; (iv) delay in commencing the tendering process; (v) delay in making payment by acquirer upon tendering the shares under open offer; (vi) various stages of litigations, etc. While in some cases, the acquirer voluntarily agrees to compensate the shareholders by paying interest for the delay, the issue of payment of interest for such delays is not expressly mentioned in the SAST Regulations, other than by way of order/ directions by SEBI under Regulation 32 of SAST Regulations on a case to case basis. |

In case of delay in the open offer due to the reasons listed, the acquirer may be required to pay interest at 10% per annum. |

| Shareholders entitled for interest | |||

| 4 | – | Pursuant to Supreme court order in the matter of Clariant International Limited and another vs. SEBI, acquirers have been making interest payment only to the original shareholders with regard to delay due to litigations etc.

In case of indirect acquisitions and delays on account of non-receipt of statutory approval, the offer price is enhanced after addition of interest. Therefore, the revised offer price, after addition of interest for the entire period, is paid to all the shareholders who have tendered their shares in the open offer (irrespective of date of purchase of shares). |

Revised open offer price may be calculated after addition of interest (10%) and the revised offer price is paid to all the shareholders (in line with the approach currently followed for indirect acquisitions and delays on account of non-receipt of statutory approvals). |

–

| Consultation / Discussion Paper | Discussion Paper on proposed amendments to “SEBI (Substantial Acquisition of Shares and Takeovers) Regulation, 2011” |

| Due date for submission of Comments | 2 March 2020 |

| Link to access | https://taxguru.in/sebi/discussion-paper-proposed-changes-sebi-takeover-regulations.html |

♦ New SEBI General Order for issuance of observations on draft offer documents

SYNOPSIS

SEBI has issued the Securities and Exchange Board of India (Issuing Observations on draft offer documents pending regulatory actions) Order, 2020 (“SEBI Order 2020”) effective from 5 February 2020

- The said order supersedes the Securities and Exchange Board of India (Issuing Observations on Draft Offer Documents Pending Regulatory Actions) Order, 2006, as amended;

- Helps streamline the process and timeline involved in issuance of observations on draft offer documents (DOD);

- The General Order provides clarity on instances where an investigation, enquiry, adjudication, prosecution, disgorgement, recovery or other regulatory action is pending against an issuer, its director(s), promoter(s) and group companies (Entities).

BRIEF ANALYSIS

Brief details of the said SEBI Order 2020 are as here under:

i. Treatment where there is a probable cause for investigation or enquiry or when an investigation or enquiry is in progress against the entities

The observations on the draft offer filed shall be kept in abeyanace:

ii. Treatment where show cause notice has been issued to entities

iii. Treatment where recovery proceedings have been initiated or an order for disgorgement or monetary penalty has not been complied with or in case of non-compliance with any direction issued by the Board.

The observations on the draft offer document shall be kept in abeyance till such proceedings are concluded or until the directions are complied with.

iv. Re-consideration of proceedings pursuant to remand by the Securities Appellate Tribunal or court.

SEBI may take appropriate action in respect of the draft offer document under the provisions of this general order, subject to any order passed by the Securities Appellate Tribunal or a court, as the case may be, while remanding the matter.

v. Issuance of observations when the issuer is restrained by a court from making a public issue or filing of offer document:

SEBI may examine the offer document and issue its observations thereof with a qualification and that the public issue or issuance of the offer document to public shall be subject to the orders of such court or tribunal or authority.

vi. Issuance of observations do not indicate exoneration

Issuance of observations on draft offer document when an investigation or enquiry is pending or when any regulatory action is pending, does not indicate that the party has been exonerated in such proceedings or that action may not ultimately result from such proceedings.

vii. Removal of difficulties

In deserving cases, the Competent Authority may grant exemption from strict enforcement of any provision of the extant General Order.

| Law/section/rule/regulation amended | SEBI (Issuing Observations on Draft Offer Documents Pending Regulatory Actions) Order, 2006 |

| Effective date of amendment | 5 February 2020 |

| Link to access | https://taxguru.in/sebi/sebi-issuing-observations-draft-offer-documents-pending-regulatory-actions-order-2020.html |

♦ SEBI amends the SEBI (Depositories and Participants) Regulations, 2018 to enable re-pledge of securities pledged in dematerialized form

SYNOPSIS

SEBI has amended the SEBI (Depositories and Participants) Regulations, 2018 effective 24 February 2020 whereby an explanation has been added in Regulation 79 thereof to include re-pledge of securities in pledge. Thus, the procedure prescribed under Regulation 79 of the said regulations, for creation of pledge, shall also be followed in case of re-pledge of securities for margin and/or settlement obligations of beneficial owner.

EXTRACT OF REGULATION

Regulation 79 – Manner of creating pledge or hypothecation

The SEBI has approved insertion of the following explanation to Regulation 79 (manner of creating pledge in Depository) of the SEBI (Depositories and Participants) Regulations, 2018:

“Explanation:– For the purpose of these regulations, “pledge” includes re-pledge of securities for margin and/ or settlement obligations of the client or such other purposes as specified by the Board from time to time.”

| Law/section/rule/regul ation amended | Regulation 79 of the SEBI (Depositories and Participants) Regulations, 2018 |

| Effective date of amendment | 24 February 2020 |

| Link to access

|

https://taxguru.in/sebi/sebi-depositories-participants-amendment-regulations-2020.html |

♦ Consultation paper on Review of the Regulatory Framework for Corporate bonds and Debenture Trustees for public comments by 17 March 2020.

SYNOPSIS

With an objective to, inter alia, strengthen the regulatory framework for Corporate bonds and Debenture Trustees, SEBI has released a consultation paper on review of regulatory framework for Corporate Bonds and Debenture Trustees (“DTs”).

BRIEF OF AMENDMENT

Summary of the issues inviting public comments are here under:

| Creation of Identified Charge by the NBFCs

|

NBFCs, for every issue shall create charge on the identified assets that may include identified receivables, investment and cash instead of floating charge on the entire books of the NBFC. A debenture issued by an NBFC shall be treated as secured only on creation of identified charge. A transition period of 3-5 years shall be provided to shift from floating Pari-Passu charge to identified charge |

| Enhanced due diligence of identified assets and Granular Asset cover certificate | The statutory auditor certificate on asset cover shall be submitted on a half-yearly basis instead of annual basis and to make it more granular in terms of parameters proposed for maintaining the asset cover to enhance the monitoring of the quality of the underlying assets. If the quality of one or more of the identified receivables/ assets deteriorates or the receivable/ asset is pre-paid, the issuer shall identify further receivables to replace the bad/ matured/ prepaid ones and maintain the asset cover in accordance with the terms of Trust Deed.

For maintaining the quality of underlying assets, following parameters are being proposed:

|

| Calling of Event of Default (EoD) at ISIN level | DTs shall call EoD at ISIN level, which shall also include breach of any covenant mentioned in the IM/ DTD. |

| Mechanism/Conditions of joining Inter-Creditor Agreement (ICA) | Debenture Trustees shall join ICA subject to approval of debenture holders and following conditions:

a) If Resolution Plan imposes condition(s) on the DTs which are not in accordance with the provisions of SEBI Regulations and circulars issued, then DTs shall be free to exit ICA altogether with the same rights as it if never signed ICA. In such a circumstance, Resolution Plan would not be binding on the DTs. b) Resolution Plan shall be finalized within 180 days from the end of review period. If not, the DTs shall be free to exit the ICA altogether with the same rights as it if never signed the ICA. In such a circumstance, Resolution Plan would not be binding on the DTs. However, If ICA extends beyond 180 days, DTs can take extension beyond 180 days’ subject to approval of debenture holders with total timeline not exceeding 1 year from commencement period of ICA.

Further, a Debenture holder representative committee consisting of debenture holders having majority investment may be formed after default by the issuer, to Fast Track the ICA process and consent seeking by Debenture Trustee during the course of ICA. |

| Voting mechanism | i. Time period sought for seeking consent shall be reduced to 15 days from 21 days.

ii. For public and private placement, DT shall enforce the security by taking negative consent in the event of default (EoD). iii. The consent of debenture holders for enforcement of security and for joining ICA shall be taken simultaneously in the same letter iv. Negative consent for enforcement of security and positive consent for joining ICA shall be taken in the same letter. v. Proof of dispatch and delivery shall be maintained by the Debenture Trustee. vi. Providing E-Mail IDs shall be compulsory for Debenture holders in case of Private Placement |

| Creation of a recovery fund | i. A fund shall be created by the issuer at the time of issuance of debt that shall be used by DT in the event of default towards recovery proceedings expenses.

ii. The value of such fund shall be 0.01% percentage of the issue subject to the cap of 25 lakhs per issuer. iii. The above shall not be applicable on AAA rated bonds. However, in case of rating downgrade of a AAA rated bond, the issuer shall be obligated to create such fund within a fixed time frame. iv. Disclosure to such affect shall also be made in the IM. Such fund shall be overseen by the DT. v. The amount shall be returned to the issuer at the time of maturity in case there is no default by the company. |

| Minimum Disclosures on the website by DTs

|

i. Quarterly Compliance Reports received from the issuers.

ii. Compliance status on the receipt of asset cover from the issuers, maintenance of various funds by the issuers. iii. Defaults by the company. iv. Status of the proceedings of the cases under default. v. Compliance status of each covenant- issue wise on a half yearly basis. vi. Repayment schedule calendar/ calendar of interest and redemptions issuer wise (already mandated) |

| Disclosures regarding Performance of DTs | Disclosure on the following parameters may be made by DTs which would be reflective of their promptness in discharging their duties:

i. Timeliness on action taken (adhering to the time-lines specified by regulations/ transaction documents). ii. Monitoring of covenants / security cover iii. Timely intimation of a breach in covenants (if any). iv. Timely raising of red-flags if the issuer response is unsatisfactory. v. Effectiveness in enforcing security/ remedial actions in case of default. vi. Promptness in convening debenture holder’s meeting and aiding in decision making as and when requested or required |

| Public Disclosure of all covenants by the issuer in IM : | All covenants including the accelerated payment covenants whether given by way of side letter or otherwise shall be incorporated in the IM by the issuer at the time of issuance of debentures and disclosed on the stock exchange. The issuer shall also be obligated to inform the DT of such covenants for monitoring of the same by DT on behalf of the investors |

| Standardization of Debenture Trust Deed (DTD) | DTD shall be bifurcated into two parts:

i. Part A of DTD shall contain generic/standard clauses common to all DTDs. ii. Part B of DTD shall contain specific and customized clauses/ covenants relevant to the particular issue for which the DTD is executed. |

| Enhanced Disclosures | Following additional disclosures shall be made by the issuer in Investment Memorandum (IM):

i. A risk factor to state that while the debenture is secured against a charge to the tune of 100% of the principal and interest amount in favour of DT, the possibility of recovery of 100% of the amount shall depend on the market scenario prevalent at the time of enforcement of the security. ii. The issuer has no side letter with any bond holder except the one(s) disclosed in the IM and on the stock exchange website where the debt is listed. iii. About Pari-Passu charge and the entitlement of the investor in such cases. iv. The rights and duties of the DT. v. The detailed procedure to be followed at the time of default by the DT including relevant procedures of ICA, DRT / National Company Law Tribunal (NCLT) and IBC. vi. The procedure and manner of calling meeting of debenture holders. Following additional disclosures shall be made by the issuer in DTD as well: i. The rights and duties of the DT. ii. The detailed procedure to be followed at the time of default by the DT including relevant procedures of ICA, DRT / NCLT and IBC. iii. The procedure and manner of calling of meeting of debenture holders, responsibility of debenture holders in such situations etc. iv. Bearing of recovery expenses in case of default. |

| A framework for imposing fines and Standard Operating Procedure (SOP) for the same | An SOP shall be prepared that shall list out the penalties for specific violations by the issuer company for the listed debt |

–

| Law/section/rule/regula tion amended | Regulatory Framework for Corporate bonds and Debenture Trustees |

| Due date of submission of Comments | 17 March 2020 |

| Link to access | https://taxguru.in/sebi/consultation-paperreview-regulatory-framework-debenture-trustees-dts.html |

C. SEBI INFORMAL GUIDANCES

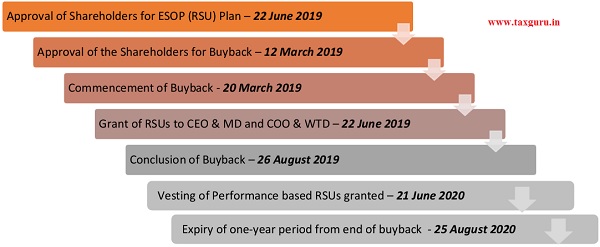

I. Infosys Limited – Issue of shares pursuant to completion of one year of Vesting of RSUs but prior to the one year from the end of Buyback Period

Facts and timeline of the facts of the case:

| Queries Raised: | SEBI’s Views |

| Can Company allot equity shares prior to expiry of one-year period from the end of the buy-back period upon exercise of vested RSUs after completion of their minimum vesting. period i.e. on 21 June 2020

(as Regulation 24(i)(f) of the Buy-back Regulations prohibits a Company to raise further capital for a period of one year from the expiry of buy-back, except for the discharge of its subsisting obligations.) |

Regulation 24(i)(f) of the SEBI Buyback Regulations restricts further issue of capital for a period of 1 year from the expiry of the Buy-back period, except in discharge of subsisting obligations.

Section 68(8) of the Act places a restriction on further issue of the same kind of shares or other specified securities, including allotment of new shares under Section 62(1)(a) of the Act (further issue of share capital) or other specified securities for a period of six months from the date of conclusion of buyback period except by way of a bonus issue or in the discharge of subsisting obligations such as conversion of warrants, stock option schemes, sweat equity or conversion of preference shares or debentures into equity shares. Therefore, subsisting obligations include conversion of stock options schemes. Therefore, the interpretation of “subsisting obligations” used in the SEBI Buyback Regulations may be considered as same as provided in the Act. In view of the above, the issuance of shares pursuant to conversion of RSUs would be considered as “subsisting obligations” as indicated in Regulation 24(i)(f) of SEBI Buyback Regulations and the applicant may issue the equity shares after the completion of one year vesting period as stipulated under Regulation 18(1) of the SBEB Regulations, subject to compliance of other provisions of SBEB Regulations, SEBI Buyback Regulations and Companies Act, 2013. |

| Can Company consider ESOPs granted during the buy-back period, as subsisting obligations as on the closure of the buy-back under Regulation 24(1)(f) of the Buyback Regulation |

–

| Link to access the Informal Guidance | https://www.sebi.gov.in/enforcement/informal-guidance/feb-2020/informal-guidance-in-the-matter-of-m-s-infosys-limited-regarding-sebi-buy-back-of-securities-regulations-2018-and-sebi-share-based-employee-benefits-regulations-2014_45898.html |

II. JSW Limited – Applicability of SEBI (Share Based Employee Benefits) Regulations, 2014 to Joint Ventures and Promoter Controlled Entities

Facts of the case:

1. JSW Group, comprises of various subsidiaries, joint venture companies, associates and other related party entities form an integral part of JSW Group and have contributed significantly to the growth of JSW Steel. JSW Entities are desirous of granting cash-based SARs linked to the share of JSW Steel, to certain identified employees, though a Trust established by JSW Entities, which shall be managed by professional trustees appointed by JSW Entities. order to retain talented human resources and recognize the efforts of employees of these entities.

2. The mechanism for implementation of Proposed Scheme is given below:

i. Each of the JSW entities will formulate a cash-based Stock Appreciation Scheme (“Scheme”) for employees. Each unit of SAR will derive value from 1 equity share of JSW Steel.

ii. The Scheme will be implemented through a discretionary trust to be settled by JSW Entities and will be managed by professional trustees appointed by JSW Entities.

iii. While granting SAR, Trust will acquire requisite no of shares of JSW Steel through secondary market by procuring interest bearing loan from the JSW entity.

iv. On redemption / settlement of SAR, Trust will sell requisite no of shares of JSW Steel representing the relevant SAR.

v. Difference between market price of equity shares of JSW Steel on the date of redemption of SAR and Exercise price (net of taxes) will be distributed to employees.

vi. The Trust will utilize the balance funds to repay the loan and interest therein to JSW entity.

vii. Upon closure of Scheme, the Trust will terminate.

3. None of the Proposed Schemes will be administered or implemented by JSW Steel or its subsidiaries.

4. Compliance with relevant Insider Trading Regulation will be ensured.

5. In the proposed scheme, SAR is proposed to be set up for:

Case A – Joint Ventures (Group entity as per definition of Regulation 2(1)(o) of SEBI SBEB Regulations) for the benefit of employees of the Joint Venture and not for the benefit of the employees of JSW Steel of its subsidiaries and

Case B – Promoter Controlled Entities (Not a Group entity as per definition of Regulation 2(1)(o) of SEBI SBEB Regulations) for the benefit of employees of the Promoter Controlled Entities and not for the benefit of the employees of JSW Steel of its subsidiaries.

| Query raised: | SEBI’s views on the Query: |

| Whether the scheme under Case A and Case B as mentioned above falls under purview of SBEB Regulations, and if not, whether there is a prohibition under any SEBI Regulations in executing such a Scheme. | As per the definitions given below*, the provisions of the SEBI SBEB regulations shall apply to those companies whose shares are listed on any recognized stock exchange in India and has a scheme, which is set up, funded or guaranteed and controlled or managed by the company or any other company in its group for the direct or indirect benefit of the employees.

The proposed Schemes mentioned in Case A and Case B, is being set up by entities which are: (a) Group entities of the JSW Steel and are JVs with JSW Steel but with less than 50% stake of JSW Steel. (b) Promoter controlled companies (but not group entities as per the above definition of group in SEBI SBEB Regulations) of the JSW Steel. The said Scheme is for the benefit of the employees of the respective group entities. Thus, the said schemes Case A and Case B does not come under the ambit of the said SEBI SBEB Regulations, as the said Scheme is not being issued for the benefit of the employees of the listed company, i.e. JSW Steel or its subsidiaries or holding company, as mentioned in Regulation 2(1)(f) of the SEBI SBEB Regulations. |

*As per Regulation 1(4) of SEBI SBEB Regulations, 2014:

“The provisions of these regulations shall apply to any company whose shares are listed on a recognised stock exchange in India, and has a scheme:

i. for direct or indirect benefit of employees; and

ii. involving dealing in or subscribing to or purchasing securities of the company, directly or indirectly; and

iii. satisfying, directly or indirectly, any one of the following conditions:

> the scheme is set up by the company or any other company in its group;

> the scheme is funded or guaranteed by the company or any other company in its group;

> the scheme is controlled or managed by the company or any other company in its group.”

As per Regulation 2(1)(f) of the SEBI SBEB Regulation, 2014:

“Employee means –

i. a permanent employee of the company who has been working in India or outside India; or

ii. a director of the company, whether a whole time director or not but excluding an independent director; or

iii. an employee as defined in clause (i) or (ii) of a subsidiary, in India or outside India, or of a holding company of the company but does not include—

a. an employee who is a promoter or a person belonging to the promoter group; or

b. a director who either himself or through his relative or through any body corporate, directly or indirectly, holds more than ten per cent of the outstanding equity shares of the company;

As per Regulation 2(1)(o) of the SEBI SBEB Regulation, 2014:

“group” means two or more companies which, directly or indirectly, are in a position to,

(i) exercise twenty-six percent or more of the voting rights in the other company; or

(ii) appoint more than fifty per cent of the members of the board of directors in the other company; or

(iii) control the management or affairs of the other company;”

| Link to access the Informal Guidance | https://www.sebi.gov.in/sebi_data/commondocs/feb- 2020/ SEBI%20Informal%20Guidance%20Letter%20JSW% 20Steel%20Ltd_p.pdf |

III. Shri Dinesh Mills Limited – Exemptions from open offer under the SEBI Takeover Regulations in case of inter-se transfer amongst Promoter/Promoter Group entities, restriction of contra trade under SEBI PIT Regulations

As part of overall succession planning between the promoter families of Shri Dinesh Mills Limited, it is desired by the Promoters/Promoter Group to transfer their current shareholding as well as all the shares received pursuant to conversion of warrants to their respective trusts (collectively referred to as Acquirer Trusts). Promoters / members of Promoter Group are evaluating to migrate their shareholding in the Company to Acquirer Trusts as per the below steps:

a. Conversion of outstanding warrants into equity shares by Promoters

b. Off-market transfer of shares by way of gift between family members

c. Migration of shares held by Promoters and Promoter Group to Acquirer Trusts

d. Acquirer Trusts (falling under the definition of promoter group under SEBI ICDR Regulations) are controlled by the Trustees (who are members of the Promoter / Promoter Group. Further, beneficiaries of the Trusts are also members of the Promoter and Promoter Group.

| Query raised: | SEBI’s views on this matter: |

| Whether the proposed inter-se off-market transfer of shares between insiders within a period of six months post receipt of shares by the same Promoters /members of the Promoter group pursuant to conversion of warrants will violate provisions regarding contra trade of the SEBI (Prohibition of Insider Trading) Regulations, 2015 and attract any penal provisions? | In the instant case, the said promoters have option to convert warrants any time within 18 months from the date of allotment in one or more tranches. The subsequent sale within 6 months may attract the contra trade restrictions under the PIT Regulations. Likewise, if the promoters / members of the promoter group who had acquired shares through inter-se off-market transfer of shares or through block deal window mechanism between promoters/members of the promoter group want to transfer shares to the Acquirer trusts within 6 months, the proposed transfer to the acquirer trusts within 6 months may also attract the contra trade restrictions specified under the PIT Regulations. |

| If the Promoters/members of the Promoter group who had acquired shares through inter-se off-market transfer of shares or through block deal window mechanism between Promoters / members of the Promoter group, wants to transfer shares to the Acquirer Trusts within 6 months, whether the proposed transfer to the Acquirer Trusts within 6 months would violate the provisions regarding contra trade as provided in the SEBI (Prohibition of Insider Trading) Regulations, 2015? | |

| Whether the equity shares acquired by the members of the Promoter and promoter group of SDM, pursuant to the exemption under Regulation 10(1)(a) and Regulation 11(1) of the Takeover Regulations respectively in the Financial Year 2019-20 consume or reduce the creeping acquisition limit of 5% in the same Financial Year 2019-20 in terms of Regulation 3(2) of the Takeover Regulations? | The acquisition which are otherwise exempt under Takeover Regulations may not be counted towards computing acquisitions on a gross basis under the creeping acquisition limit in terms of Regulation 3(2) of SAST Regulations. |

| Whether the specified securities held by promoters/members of the promoter group and locked-in as per Regulation 167(1) of ICDR Regulations can be transferred to Acquirer Trusts as per Regulation 168(1) of ICDR Regulations, 2018? | The specified securities i.e. shares of SDM, held by promoters / members of the promoter group and locked-in as per Regulation 167 (1) of ICDR Regulations, 2018 (i.e. 3 years from the trading approval), may be transferred to the Acquirer Trusts under Regulation 168 (1) of ICDR Regulations, 2018 (for inter-se transfer amongst promoter/promoter group, said lock in to continue for remaining period). However, the said transferability, is subject to the provisions of SEBI (Substantial Acquisition of shares and Takeovers) Regulations, 2011. |

–

| Link to access the Informal Guidance | https://www.sebi.gov.in/enforcement/informal-guidance/feb-2020/in-the-matter-of-nimish-upendrabhai-patel-under-sebi-substantial-acquisition-of-shares-and-takeovers-regulations-2011-sebi-prohibition-of-insider-trading-regulations-2015-and-sebi-issue-of-ca-_45888.html |

D. NATIONAL COMPANY LAW TRIBUNAL ORDERS (“NCLT”)

“NCLT orders inclusion of Videocon’s overseas assets in insolvency”

NCLT order dated 12 February 2020: State Bank of India V/s. Videocon Industries Limited

Petitioner – State Bank of India (“SBI”)

Respondent No. 1 – Videocon Industries Limited (“VIL”) Respondent No. 2 – VOVL Ltd. (“VOVL”)

Respondent No. 3 – Videocon Hydrocarbon Holdings Ltd. (“VHHL”)

Respondent No. 4 – Videocon Energy Brasil Ltd. (“VEBL”) Respondent No. 5 – Videocon Indonesia Nunukan Inc. (VINI)

Facts of the Case:

The timeline of the above case is as under:

| June 2018 |

|

| Oct 2018 |

|

| July 2019 |

|

| Aug 2019 |

|

| Aug 2019 |

|

| Nov 2019 |

|

| Feb 2020 |

|

Mr. Venugopal Dhoot, guarantor, shareholder, former MD/Chairman of VIL, opposed the sale of assets of the Oil & Gas business and plead to consider and treat all assets, properties (tangible and intangible), rights, claims, benefits of the Respondent Nos. 2 to 5 as assets and properties of VIL for the purpose of present CIRP and to include the assets, liabilities, claims of Respondent Nos. 2 to 5 of the present Corporate Debtor, VIL on, inter alia, the following grounds:

- The foreign oil and gas assets, properties, claims and participating interests were initially acquired by VIL and then subsequently Respondent Nos. 2 to 5 were incorporated just to ostensibly hold these foreign oil and gas assets for and on behalf of the present Corporate Debtor / VIL.

- The Respondent Nos. 2 to 5 are the special purpose vehicles (SPVs) created only to ostensibly hold the foreign oil and gas assets, properties and interests therein. The said Respondents are acting like extended branch of the present Corporate Debtor / VIL and had no separate control and management and decision-making power on its own.

- The entire management, operation and Board of the Respondent No. 2 was completely controlled and was acting under the instructions of VIL and it never enjoyed any independent decision-making power. The Board of these companies did not have any independent decision-making authority. that they belonged to VIL overseas arms, which were set up as special purpose vehicles to act as trustee and hold the assets on behalf of VIL .

- The Respondent Nos. 2 to 5 never had any independent means of income and/ or assets and/ or business to acquire / subscribing shareholding or assets but solely on the basis of the financial assistance from VIL, the foreign oil and gas assets, properties and/ or interests therein was acquired

- The present holding structure to hold the participating interests in the foreign oil and gas assets through the Respondent Nos.2 to 5 (SPVs) was created for the convenience purpose as it was practically difficult for the present Corporate Debtor / VIL to fund the operation costs of these foreign oil and gas assets (cash calls) from India to foreign countries under the provisions of the FEM Act.

- The lenders have treated the Videocon Group as a single economic entity for CHA, Telecom and Oil and Gas Business while lending the money for these businesses through various facility agreements.

- The Lenders i.e. the financial creditors of Respondent Nos.1 and other 12 companies referred in CIRP had second charge on the foreign oil and gas assets as specifically referred in the Rupee Term Loan Agreement as well as LOC/ SBLC Facility Agreement. Therefore, clearly qualifies the criterion laid down in the consolidation order to treat the assets of Respondent Nos.2 to 5 as assets of Respondent No.1 i.e. the present Corporate Debtor / VIL.

- That it shall be in public interest to lift the corporate veil of Respondent Nos.2 to 5.

In light of the submissions and contentions of the parties, including the various provisions of the Code and the case laws relied upon by the parties, the following contentions were raised and considered by NCLT while passing the order:

a) Whether the foreign oil and gas assets and properties, including any claim, interest therein, of Videocon Group held through Respondent Nos.2 to 5 can be said to be the property of Respondent No.1, the present Corporate Debtor/ VIL for the purpose of the present CIRP.

b) Whether the provision of Section 14 of the Code would apply to the said foreign oil and gas assets and properties, including any claim, interest therein?

c) This Bench on 08.08.2019 had passed a Consolidated Order in case of VIL. While doing so this Bench had framed certain parameters on the touchstone of which the rationale or otherwise regarding consolidation was decided. It would be worthwhile to see whether in this case those parameters stands or not.

| SBI contention | NCLT views |

| The Code envisage the CIRP process is basically creditor driven process, therefore it should be left at the choice of financial creditors and they are free to choose to independently liquidate the foreign oil and gas assets. | This is not the correct interpretation and it is worth to point out and request that the IB Code clearly envisages ‘to balance the interest of all stakeholders’ which includes not only the Financial Creditors but also the Operational Creditors, employees etc. |

| The foreign oil and gas assets are not shown in the balance sheet of the Respondent No.1/ VIL in view of Section 18 of the Code it cannot be said to be assets of Respondent No.1/ VIL. | Section 18 of the Code deals with the duties of the Resolution Professional and Section 18 (f) therein is just indicator that what assets to be taken over in the custody by the Resolution Professional. However, in our opinion in the case like this, the 18(f) will have limited role to play. In our opinion, in the case like this wherein initially assets is acquired in the name of Respondent No.1/ VIL and the Share Sale Agreements as well as Quotaholder Agreement clearly mentions name of Respondent No.1/ VIL as joint owner/ purchaser with BPCL/ BPRL. Any subsequent creation of the structure of Respondent Nos.2 to 5 and in absence of any legal transfer of all rights, interests and ownership in the said properties, assets by the Respondent No.1/ VIL, at market value in favour of Respondent Nos.2 to 5, will not make Respondent Nos.2 to 5 as owners of these assets in exclusion of Respondent No.1/ VIL. Therefore, the Balance Sheet cannot be sole criteria of deciding ownership of the assets when the other documents and evidences are in place. |

| Section 18 of the Code, which inter alia, mentions that assets of any Indian and foreign subsidiary of the Corporate Debtor shall not be deemed to be assets of the Corporate Debtor | This explanation comes into play in case it is established that the assets in question are undoubtedly held and purchased by the subsidiaries from its sources. However, in the present case as stated above the crucial acquisition documents still mentions that name of Respondent No.1/ VIL as the Purchaser and there is no subsequent transfer of these rights in favour of the Respondent Nos.2 to 5. |

NCLT further assessed and noted that all the 13 parameters (viz. Common control, Common directors, Inter-dependence, Pooling of resources, Co-existence for survival, Intricate link of subsidiaries, Intertwined accounts, Inter-looping of debts, Singleness of economics of units, Common Financial Creditors) which were enunciated in the Order dated 08.08.2019 in the consolidation of 13 Videocon Group Companies is fully met and satisfied in this case also.

Order Passed by NCLT

A. The Mumbai bench of NCLT on 12 February 2020 concluded that assets of the foreign oil and gas business of Videocon Group held through Respondent Nos. 2 to 5 was in fact, asset and property of Respondent No.1 i.e. VIL on the count of being original acquirer or alternatively even for qualifying all tests to lift corporate veil in between Respondent No.1 i.e. VIL and Respondent Nos. 2 to 5. Therefore, the assets held by them can be said to be “its” assets i.e. the assets of Respondent No.1 (VIL, the Present Corporate Debtor) which is under the CIRP.

B. The tribunal also directed the resolution professional to include the assets, liabilities, claims of the above mentioned overseas assets, companies in the information memorandum of Videocon.

| Link to access the NCLT Order | https://nclt.gov.in/sites/default/files/Feb-final-orders-pdf/State%20Bank% 20of%20India%20MA%202385%20of%202020%20in% 20CP%28IB%29-02_2018%20NCLT%20ON%2012.02.2020%20FINAL.pdf |

E. MCA UPDATES

♦ New rules for takeover of unlisted companies

SYNOPSIS

Section 230 of the Act sets out the process for a scheme of compromise and arrangement between a company and its creditors and shareholders (“Scheme”), requiring approval of the National Company Law Tribunal (“NCLT”).

The MCA, has notified and brought into effect the provisions of sub-sections (11) and (12) of section 230 of the Act and amended the rules framed thereunder, effective 3 February 2020 whereby

– takeover offers in case of unlisted companies can be made through Scheme of compromise or arrangement, while in case of listed companies, takeover offers must be made as per regulation prescribed by the Securities and Exchange Board of India.

– An aggrieved party having grievances with respect to the takeover offer of unlisted companies can make an application to Tribunal in the prescribed manner.

– Prescribed a mechanism and the process for the above by making suitable amendments to the rules framed thereunder.

Key highlights of the amendments are thereunder:

- Any member who along with other member(s), holds 75 percent or more of the “shares” of the Company, can make an application for the purpose of takeover offer.

- Such an application should be made for acquiring any part of the remaining shares of the Company.

- Takeover offer can only be made by an existing shareholder, unlike in case of listed companies where an open offer can be made by an acquirer proposing to acquire shares in the company which would entitle the acquirer and persons acting in concert to exercise 25% or more of the voting rights in the company.

- Takeover offer for listed companies will continue to be governed by SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011.

- The new Rules will not apply to any transfer or transmission of shares through a contract, arrangement or succession, as the case may be, or any transfer made in pursuance of any statutory or regulatory requirement.

BRIEF OF AMENDMENTS in the Sections and Rules is given here under:

> Notification of sub-sections 11 and 12 of Section 230 Act – 3 February 2020

Section 230 (11) of the Act – Any compromise or arrangement may include takeover offer made in the prescribed manner and in case of listed companies, takeover offer shall be as per the regulations framed by the Securities and Exchange Board of India.

Section 230(12) of the Act An aggrieved party may make an application to the Tribunal in the event of any grievances with respect to the takeover offer of companies other than listed companies in the prescribed manner and the Tribunal may, on application, pass such order as it may deem fit.

| Law/section/rule/regulation amended | Notification of Section 230(11) and (12) of the Act |

| Effective date of amendment | 3 February 2020 |

| Link to access | https://taxguru.in/company-law/mca-notifies-sub-sections-11-12-section-230-wef-03-02-2020.html |

♦ The Companies (Compromises, Arrangements and Amalgamations) Amendment Rules, 2020 – 3 February 2020

Insertion of new sub-rule 5 and 6 in the existing Rule 3 of the said Rules as provided under:

- Sub-rule 5 (New Provision):

A member of the company along with other member, holding not less than 3/4th of shares* in the company can make a takeover offer by making an application for acquiring remaining minority shares of the company in terms of Section 230 (11) of the Act.

*shares means the equity shares of the company carrying voting rights, and includes any securities, such as depository receipts, which entitles the holder thereof to exercise voting rights.

Nothing in the sub-rule shall apply to transfer or transmission of shares through a contract, arrangement or succession or any transfer made in pursuance of any statutory or regulatory requirement.

- Sub-rule 6 (New Provision):

An application of arrangement for takeover offer under Section 230 shall contain:-

(b) Report of a Registered Valuer – Disclosing the details of valuation of shares proposed to be acquired by the member after taking into account the following factors:

i. the highest price paid by any person or group of persons for acquisition of shares during last 12 months;

ii. the fair price of shares of the company to be determined by the registered valuer after taking into account valuation parameters including return on net worth, book value of shares, earning per share, price earning multiple vis-d-vis the industry average and such other parameters as are customary for valuation of shares of such companies.

(c) Details of Bank Account opened separately, by the member, wherein at least 1/2 of the total consideration of takeover offer is deposited.

(d) The Fees for making application for compromise, arrangement and amalgamation under Rule 3 of the said Rules shall be Rs. 5,000/-.

| Law/section/rule/regulation amended | Companies (Compromises, Arrangements and Amalgamations) Rules, 2016 |

| Effective date of amendment | 3 February 2020 |

| Link to access | Companies (Compromises, Arrangements and Amalgamations) Amendment Rules, 2020 |

♦ The National Company Law Tribunal (Amendment) Rules, 2020 – 3 February 2020

Introduction of Rule 80A vide an amendment to the National Company Law Tribunal Rules, 2016 prescribing the manner and procedure in which applications shall be made to the Tribunal, as summarized hereunder:

– Application under section 230(12) shall be made in Form NCLT-1 along with attachments as under:

1. Affidavit verifying the petition;

2. Memorandum of appearance with copy of the Board’s Resolution or the executed vakalatnama, as the case may be;

3. Documents in support of the grievance against the takeover;

4. Any other relevant document;

– The fees for the aforesaid application shall be Rs. 5,000/-.

| Law/section/rule/regu lation amended | National Company Law Tribunal Rules, 2016 |

| Effective date of amendment | 3 February 2020 |

| Link to access | https://taxguru.in/company-law/national-company-law-tribunal-amendment-rules-2020.html |

♦ New integrated web-based incorporation process – Form SPICe+ :- 18 February 2020

SYNOPSIS

The MCA, vide notification dated 18 February 2020, has amended the Companies (Incorporation) Rules, 2014 to introduce new e-forms to reduce procedures, time and cost for all new company incorporation, with effect from 23 February 2020.

SPICe+ is an integrated web form which has to be filed online using the MCA-21 login services and once the SPICe+ is filled completely with all relevant details, the same would then have to be converted into pdf format, with just a click of the mouse button, for affixing DSCs.

SPICe+ will have two parts viz.:

Part A-for Name reservation for new companies;

Part B – offering a bouquet of services as follows:

(i) Incorporation

(ii) DIN allotment

(iii) Mandatory issue of PAN

(iv) Mandatory issue of TAN

(v) Mandatory issue of EPFO registration

(vi) Mandatory issue of ESIC registration

(vii) Mandatory issue of Profession Tax registration (Maharashtra)

(viii) Mandatory Opening of Bank Account for the Company and

(ix) Allotment of GSTIN (if so applied for)

New companies incorporated through SPICe+ and thereby have obtained EPFO/ESI numbers will have to file statutory returns only when they cross thresholds prescribed under the relevant Acts.

MCA has issued the key features of SPICe+ on its website and the said features can be accessed through the following link:

http://www.mca.gov.in/Ministry/pdf/EaseofBuisness_24022020.pdf

BRIEF OF AMENDMENTS are here under:

> The Companies (Incorporation) Amendment Rules, 2020 – 18 February 2020

i. Rule 9 – Reservation of name – e-form SPICe+

An application for reservation of name shall be made through the web service at www.mca.gov.in by using SPICe+ (Simplified Proforma for Incorporating Company Electronically Plus: INC-32), along with fees as prescribed.

ii. Rule 9 – Change of name – RUN

Application for change of name by using web service RUN (Reserve Unique Name) along with fees as prescribed,

The Registrar, Central Registration Centre may either approve or reject the e-forms, as the case may be, after allowing resubmission of such web form within 15 days for rectification of the defects, if any.

iii. Rule 38A – Application for registration – e-form AGILE-PRO

The application for incorporation of the Company, shall be accompanied by e-form AGILE PRO (INC-35) which in addition to registration of GST Tax Identification Number (GSTIN) and Employee State Insurance Corporation (ESIC) will also facilitate Employees’ Provident Fund Organisation (EPFO) Registration, Profession Tax Registration and Opening of Bank Account.

| Law/section/rule/regulation amended | Companies (Incorporation) Rules, 2014 |

| Effective date of amendment |

23 February 2020 |

| Link to access | https://taxguru.in/company-law/companies-incorporation-amendment-rules-2020.html |

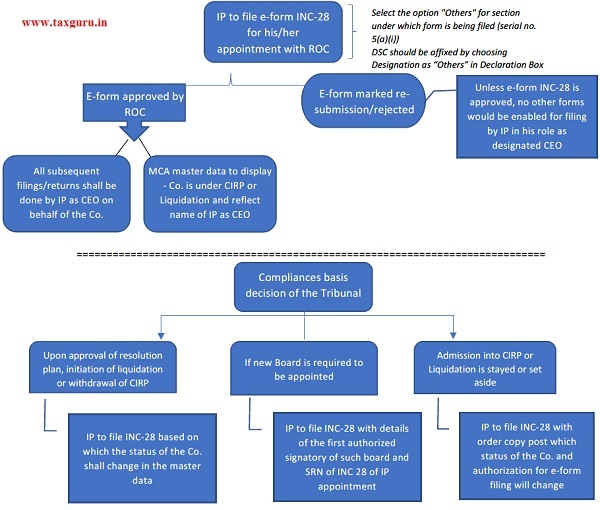

♦ MCA allows Insolvency Professionals to file eforms on MCA portal

SYNOPSIS

To enable companies undergoing insolvency resolution process to comply with statutory compliances, MCA vide its circular dated 17 February 2020 has detailed out the procedures to be followed by Insolvency Professionals viz. lnterim Resolution Professional (lRP) or a Resolution Professional (RP) or a Liquidator (“IPs”), appointed under IBC, 2016, with respect to filing of required e-forms on behalf of such companies.

BRIEF OF AMENDMENTS is here under:

| Law/section/rule/regu lation amended | Compliances to be done by Insolvency Professionals appointed under IBC. 2016 |

| Effective date of amendment | 17 February 2020 |

| Link to access | https://taxguru.in/company-law/filing-forms-registry-mca-21-irp-rp-or-liquidator.html |

♦MCA amends Companies (Issue of Global Depository Receipts) Rules, 2014 replacing the term “abroad” with “convenient jurisdiction”

SYNOPSIS

Under the earlier rules, depository receipts can be issued by way of public offering or private placement or in any other manner prevalent abroad and may be listed or traded in an overseas listing or trading platform.