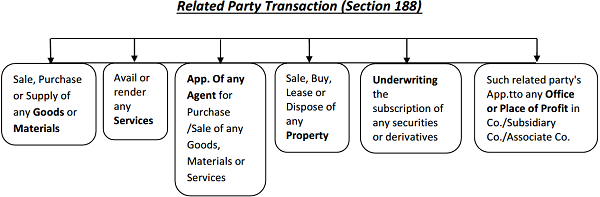

Related Party Transactions are a common occurrence in the business marketplace. Companies often seek business deals with entities to which they are familiar with or have been connected with their directors and KMPs. While these types of transactions are legal and ethical, the special relationship inherent between the involved parties creates potential conflicts of interest, which must be regulated because they can result in actions that benefit the people involved as opposed to the shareholders. Related party transactions have been an area that has received considerable attention in India and across the globe. Significant corporate frauds have happened connected to Related Party Transactions or similar arrangements.

Earlier, in the Companies Act, 1956, contracts or transactions in which directors or their relatives are interested, had been regulated through a “Government approval-based regime” now as per Companies Act, 2013 this has been shifted to “Shareholder approval and disclosure-based regime”.

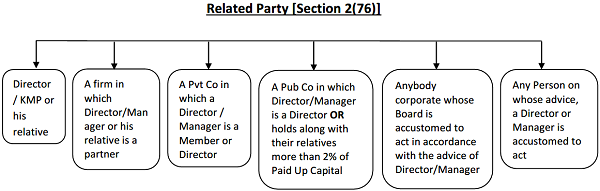

As Per Companies (Amendment) Act, 2017, following parties included in the definition of related party:

- Anybody corporate (Earlier, it was written as ‘Company’) which is holding, subsidiary or an associate company of such company or a subsidiary of a holding company to which it is also a subsidiary or an investing company or venture of the Company, shall be considered as a related party.

- An investing company or the venturer of the company” will mean a body corporate whose investment in the company would result in the company becoming an associate company of the body corporate.

Approvals Required for Carrying out RPTs

Approvals Required for Carrying out RPTs

1) Board Approval

- No company shall enter into any contract or arrangement with a related party with respect to above mentioned transactions except with the approval of Board by way of resolution (Not Circular Resolution).

- Approval of Board of Directors is required for each and every related party transaction irrespective of capital of the company and the value of the transactions.

- If a Director is interested in any contract or arrangement with a related party he shall not be present at the meeting during discussions on such resolution, Moreover, he shall neither discuss nor vote and also not be counted for quorum in respect of such transaction. Provided this is not applicable to a company in which 90 % or more members, in number, are relatives of promoters or are related parties. (Companies Amendment Act, 2017)

2) Audit Committee Approval

All related party transactions shall require approval of the Audit Committee and the Audit Committee may make ‘omnibus approval’ for related party transactions proposed to be entered into by the company subject to the certain conditions like:

- Omnibus approval shall be valid for a period not exceeding one financial year and for Transaction upto Rs. 1 Crore and shall require fresh approval after the expiry of such financial year;

- the Audit Committee shall, after obtaining approval of the Board of Directors, specify the criteria for making the omnibus approval which shall include the following, namely:-

- Name of the related parties;

- Maximum value of the transactions, in aggregate, which can be allowed under the omnibus route in a year;

- Maximum value per transaction which can be allowed;

- Extent and manner of disclosures to be made to the Audit Committee at the time of seeking omnibus approval;

- Review, at such intervals as the Audit Committee may deem fit, related party transaction entered into by the company pursuant to each of the omnibus approval made;

- Transactions which cannot be subject to the omnibus approval by the Audit Committee.

However, Omnibus approval shall not be made for transactions in respect of selling or disposing of the undertaking of the company.

Whether RPT should be first approved by Board or Audit Committee?

The Companies Act doesn’t specify whether any related party transactions should be first approved by Board or Audit Committee. In bigger transactions, the board may first refer proposed related party transactions to the audit committee and upon receiving the audit committee approval; the board will make its decision and approve the transactions. It would not be appropriate if the Audit Committee rejects a transaction, which has already been approved by the board. Hence, all matters relating to related party transactions and other matters involving conflicts of interest should be first referred to the Audit Committee.

3) Approval of Members (Shareholders)

- Approval of Members by way of Ordinary Resolution (Earlier, it was ‘Special Resolution’) required if the transactions value increased from above threshold.

- The transactions between Holding Company and its Wholly Owned Subsidiary are exempted from taking member approval.

What if Post transaction approval is not received?

Where any Related Party Transactions entered into without obtaining the consent of the Board or approval by Members and if it is not ratified by the Board or by the members at a meeting within 3 months from the date on which such contract or arrangement was entered into, such contract or arrangement shall be voidable at the option of the Board or members and if the contract or arrangement is with a related party to any director, or is authorized by any other director, the directors concerned shall indemnify the company against any loss incurred by it.

Duties of Directors

The act imposes a duty on every director to disclose the contracts or arrangements with the company, whether existing or proposed or acquired subsequently, in which he, directly or indirectly, has any interest or concern.

The notice for relevant disclosure should be made by the interested director to the Board of Directors at a meeting of the Board in which the transaction is to be discussed, so that information is available to the Board in a timely manner.

Failure to make disclosure should be treated as a default. Director concerned should be held liable to penalties and he should be deemed to have vacated his office. This should also be a condition of disqualification to hold office of director of that company for a prescribed period.

Register

The company should maintain a register, in which all transactions above a prescribed threshold value in respect of contracts/arrangements, in which directors are interested, should be entered. The register should be kept at registered office of the company and should be open to inspection to all members.

Complete Exemption from Section 188

The provisions of this section are not applicable if the transactions are in Ordinary Course of Business and at Arm’s Length Basis.

Ordinary Course of Business

The phrase “ordinary course of business” is not defined under the Companies Act 2013 or rules made thereunder. It seems that the ordinary course of business will cover the usual transactions, customs and practices of a business and of a company.

The Allahabad High Court has observed that for a transaction to be construed to have occurred in the ordinary course of business, there must be “an element of continuity and habit for it to constitute the exercise of a profession and business.” However, the frequency of transactions over a period of time should not be the only criterion and it cannot be restricted to the core business activities of a company alone. Support services that do not form part of the main core activity of a business, but are necessary and ancillary for running the core business, can also be considered as transactions that happen during the ordinary course of business.

The assessment of whether a transaction is in ordinary course of business is very subjective, judgemental and can vary on case-to-case basis giving consideration to nature of business and objects of the entity. Companies should consider variety of factors like size and volume of transactions, arms-length, frequency, purpose, etc, to make this assessment.

Arm’s Length Basis

Arm’s length transaction means a transaction between two related parties which is conducted as if they were unrelated, so that there is no conflict of interest.

For e.g, let’s assume a bank whose normal course of business provides 9% rate to its customers for placing fixed deposit for 2 year tenure. It offers 9.25%, higher rate, to all its group employees. One may argue that the same is not at arm’s length. The arm’s length assessment is subjective exercise and requires judgement after considering various parameters.

Offence & Penalty

Any director or other employee of a company, who had entered into or authorized the contract or arrangement in violation of the provision of this section shall, in case of listed company, be punishable with imprisonment for a term which may extended to one year or fine which shall not be less than twenty-five thousand but which may be extended to five lakh rupees or with both; and in case of any other company, be punishable with fine which shall not be less than twenty-five thousand but which may be extended to five lakh rupees.

Author Bio