Introduction:

Overseas mergers and acquisitions (M&A) have become a popular strategy for Indian companies to achieve corporate development, expand into new markets, and acquire new technologies and resources. According to Merger market, Indian outbound M&A surged to $20.5 billion in Q3 2021, up 49% YoY[1] and according to the Institution of Mergers, Acquisition & Alliances, the growth prospect of India in the global M&A strategy as per 2022 is 135 billion dollars[2] in Q3 2022 surpassing the pre-covid levels however globally there seem to be a decline in multiples and a mid-year pause in megadeals were the key contributors to a 36% decline in deal value in 2022 from a record high in 2021[3]. This research note will examine the regulatory landscape, risks and challenges, recent case laws and developments for Indian companies engaging in overseas M&A for corporate development.

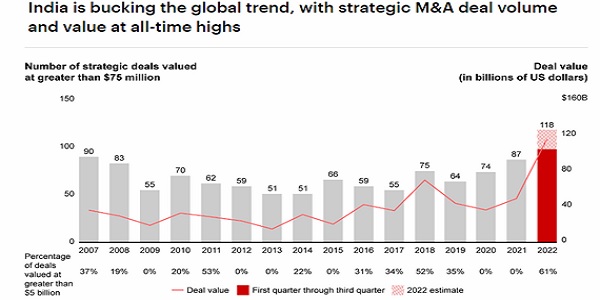

M&A Growth in India 2022

Regulatory Landscape:

Indian companies engaging in overseas M&A for corporate development must comply with the regulatory landscape in both India and the target country. In India, the Foreign Exchange Management Act (FEMA) regulates foreign investment, including inbound and outbound M&A. The Reserve Bank of India (RBI) is the primary regulatory body responsible for administering FEMA. Indian companies engaging in overseas M&A must also comply with the regulations of the target country, including antitrust, national security, and foreign investment regulations.

Mergers and acquisitions (“M&A”) in India are primarily governed by the following laws:

1. The Companies Act, 2013[4] and the rules, orders, notifications and circulars issued thereunder (as amended) (the “Companies Act”), which prescribes the general framework governing companies in India, including the manner of issuance and transfer of securities of a company incorporated in India and the process for schemes of arrangements of such companies;

2. The Indian Contract Act, 1872[5] (as amended) (the “Contract Act”), which governs contracts and the rights that parties can agree to contractually under Indian laws;

3. The Specific Relief Act, 1963[6] (as amended) (the “Specific Relief Act”), which prescribes remedies available to private parties for breach of contract;

4. The Income Tax Act, 1961[7] (as amended), which prescribes taxation-related considerations with respect to M&A in India, and to transactions that have cross-border elements. Double taxation-avoidance treaties also play an important role;

5. The Competition Act, 2002[8] (as amended) (the “Competition Act”), which regulates combinations (such as M&A) of companies and prohibits anti-competitive agreements, which have or are likely to have an appreciable adverse effect on competition in India;

6. The Foreign Exchange Management Act, 1999[9] and the rules and regulations issued thereunder (as amended) (the “FEMA”), read together with the circulars, directions and rules issued by the Reserve Bank of India (the “RBI”), which, collectively, regulate foreign investment in India (the “Foreign Exchange Regulations”), including the Foreign Exchange Management (Cross Border Merger) Regulations, 2018 (the “Cross Border M&A Regulations”), which govern mergers between Indian companies and foreign companies;

7. The consolidated Foreign Direct Investment Policy Circular of 2020[10] (as amended), read together with the press notes issued by the Department of Promotion of Industry and Internal Trade, Ministry of Commerce and Industry, Government of India (the “DPIIT”);

8. Various pieces of Central Government and State Government labour legislation, which govern employment- related matters (such as terms of service, payment of wages, work conditions, safety, health and welfare of workers, etc.); and the Securities and Exchange Board of India Act, 1992 and the rules and regulations issued thereunder (as amended) (the “SEBI Act”) read together with the circulars, notifications, guidelines and directions issued by the Securities and Exchange Board of India (the “SEBI”), which regulate the securities markets in India including acquisitions involving companies listed on stock exchanges in India (the “SEBI Regulations”).

Recent Developments:

Some of the notable legal updates in M&A in India are set out below:

1. Foreign Exchange Management (Overseas Investment) Rules 2022 (the “OI Rules”)[11]: Previously, transactions involving overseas investment/acquisition and the transfer of immovable property outside India by a person resident in India were governed by the Foreign Exchange Management (Transfer or Issue of Any Foreign Security) Regulations, 2004 and the Foreign Exchange Management (Acquisition and Transfer of Immovable Property Outside India) Regulations, 2015 (collectively, the “Prior Regulations”). On 22 August 2022, the Central Government notified the OI Rules and the RBI notified the Foreign Exchange Management (Overseas Investment) Regulations, 2022 (the “OI Regulations”), which subsume the Prior Regulations, to streamline and liberalize the regulatory framework. In addition, the RBI has issued the Foreign Exchange Management (Overseas Investment) Directions, 2022 (the “OI Directions”) in line with the OI Regulations. The OI Rules set out the provisions in relation to overseas investment by residents, which will be administered by the RBI. In addition, the OI Regulations and the OI Directions outline the operational aspects/conditions for undertaking financial commitment, investments in debt instruments, mode of payment, deferred payment of consideration, reporting realization, and other requirements. While the new framework largely incorporates the provisions under the Prior Regulations, a snapshot of key changes under the new regime are set out below.

i. Overseas direct investment vs. overseas portfolio investment: The OI Rules provide a clear distinction between overseas direct investment (“ODI”) and overseas portfolio investment (“OPI”), the segregation of which was not captured under the Prior Regulations. Under the OI Rules, the term ODI is defined to mean (A) acquisition of any unlisted equity capital or subscription as a part of the memorandum of association of a foreign entity; (B) investment in 10% or more of the paid-up equity capital of a listed foreign entity, or (C) investment with control where investment is less than 10% of the paid-up equity capital of a listed foreign entity. Once an investment in a foreign entity is classified as ODI, the investment will continue to be treated as ODI even if such investment falls below 10% of the paid-up equity capital or the investor loses control in the foreign entity. On the other hand, the term OPI means any overseas investment which is not ODI, other than investment in any unlisted debt instruments or any security issued by a person resident in India who is not in an International Financial Services Centre (the “IFSC”).

ii. Foreign entity, limited liability and strategic sector: The erstwhile terms “wholly owned subsidiary and joint venture” have been replaced by the term “foreign entity” which means an entity formed or registered or incorporated outside India, including in an IFSC in India, which has limited liability. While the new definition is conceptually similar to the erstwhile phrases, the OI Rules has newly introduced the construct of limited liability. Under the OI Rules, ‘limited liability’ means a structure where the liability of the person resident in India making the investment is clear and limited (in the case of a limited liability company or limited liability partnership) or does not exceed the interest or contribution in the fund (in the case of a foreign entity being an investment fund or vehicle set up as a trust and where the trustee is a person resident outside India). However, the limited liability structure of foreign entity is not mandatory for entities with core activity in any ‘strategic sector such as oil, gas, coal, mineral ores, submarine cable system and start-ups and any other sector or sub-sector’ as deemed fit by the Central Government (where ODI is permissible in unincorporated entities as well). An Indian entity is also permitted to participate in a consortium with other international operators to construct and maintain submarine cable systems on co-ownership basis. Such provision indicates the intention of the Government to promote overseas investments by persons resident in India in such key/identified foreign sectors.

iii. Round tripping: Under the previous regime, an Indian party was restricted from: (A) setting up a subsidiary in India through a foreign entity, and (B) investing in a foreign entity that has made any prior investments in India, without a prior approval from the RBI. The OI Rules now permit financial commitments by persons resident in India in a foreign entity that does not have (directly/indirectly) more than two layers of subsidiaries. In addition, the above restriction does not apply to certain identified classes of companies (such as a Government company, a (systemically important) non-banking financial company, a banking company or an insurance company).

iv. Dispensation with other prior approval requirements: Under the Prior Regulations, a prior approval of the RBI was required for any deferred payment of consideration, issuance of corporate guarantees to or on behalf of second or subsequent level step down subsidiary, write off on account of disinvestment and investment/disinvestment by persons resident in India who are under investigation by any investigation/enforcement agency or regulatory body. However, prior approval for the above instances is no longer required under the new framework.

v. ODI in the financial services sector: Under the new regime, an Indian entity that is not engaged in the business of financial services can also invest in a foreign entity which is engaged in financial services (except banking and insurance business), subject to posting net profits during the preceding three financial years, which was not permitted under the Prior Regulations. In addition, if an Indian entity does not meet the stipulated net profits due to the impact of COVID-19 during the period from 2020-2021 to 2021-2022, then the financial results of such period may be excluded for considering the profitability period of three years. The OI Guidelines further clarify that a foreign entity will be considered to be engaged in the business of financial services activity if it undertakes an activity, which if carried out by an entity in India, requires registration with or is regulated by a financial sector regulator in India.

2. Review of the FDI Policy and Amendment under the NDI Rules: Pursuant to Press Note No. 1 (2022 Series) dated 14 March 2022[12], the DPIIT has reviewed the extant Consolidated FDI Policy Circular of 2020 effective from 15 October 2020 (the “FDI Policy”) and made, inter alia, the following amendments:

i. Allowing foreign investment of up to 20% under the automatic route (subject to compliance with specified conditions) in the Life Insurance Corporation of India;

ii. Amending the definition of foreign investment to clarify that if a declaration is made by a person under the Companies Act or any other applicable law, about a beneficial interest being held by a person resident outside India, then even though the investment may be made by a resident Indian citizen, such investment will be construed as a foreign investment;

iii. Including a new definition of ‘share based employee benefits’ to mean the issue of equity instruments to employees or directors of the holding company, joint venture, wholly owned overseas subsidiary or subsidiaries who are resident outside India, pursuant to share-based employee benefits schemes formulated by an Indian company. Related changes have also been made under the provisions of the issuance of employees’ stock options (“ESOPS”) and sweat equity shares to include references to share-based employee benefits. Prior to the amendment, ESOPs and sweat equity shares were the only recognized forms of incentives that an Indian company could issue to its non-resident employees, etc. Accordingly, going forward, any employee incentive scheme (framed in accordance with applicable law) of an Indian company involving issuance of equity instruments to its non-resident employees, etc. will be covered under the above definition and such Indian companies will need to ensure compliance with the NDI Rules. Suitable amendments have also been made under the NDI Rules pursuant to the Foreign Exchange Management (Non-debt Instruments) (Amendment) Rules, 2022 dated 12 April 2022 to align the NDI Rules with the above changes under the FDI Policy.

3. Amendments by the MCA in relation to the Restricted Countries: Considering the restrictions set out under the Foreign Exchange Regulations regarding the Restricted Countries, the Ministry of Corporate Affairs (the “MCA”) has amended the following rules framed under the Companies Act to require the relevant company/body corporate to declare as to whether it needs to obtain prior Government approval under the NDI Rules and, if so, a copy of such approval needs to be attached:

i. Companies (Compromises, Arrangements and Amalgamations) Rules, 2016[13]: A declaration regarding the applicability of the Government approval under the NDI Rules will need to be furnished by the relevant company/body corporate at the stage of submission of application under section 230 of the Companies Act.

ii. Companies (Prospectus and Allotment of Securities) Rules, 2014[14]: A prior Government approval under the NDI Rules is now mandatory for an offer/invitation of securities to be made to a body corporate incorporated in a Restricted Country. Such approval (if applicable) will need to be attached with the private placement offer cum application letter.

iii. Companies (Share Capital and Debentures) Rules, 2014[15]: A transferee of securities must make a declaration removing the applicability of a prior Government approval for the transfer of shares.

iv. RBI’s liberalization of forex flows[16]: Pursuant to the press release dated 6 July 2022, the RBI has decided to, temporarily increase the limit from USD 750 million to USD 1.5 billion under the automatic route for external commercial borrowings until 31 December 2022, and allow foreign portfolio investors to invest in government securities and corporate bonds through the specified channels.

4. Disclosure of complimentary linkages to the CCI on 31 March 2022[17], the CCI has modified the (long) Form II (i.e., the form used to notify a combination if the parties to a combination are: (i) Competitors and have a combined market share of more than 15% in the same market; or (ii) Vertically linked and the combined/individual market share in any of these markets is more than 25%), to include additional disclosures/information with respect to the complimentary linkages between them and their impact on the market. In addition, the companies need to declare five years’ worth (instead of the earlier requirement of one year) of market-facing data relating to market share, their competitors, customers and suppliers. Further, such companies must declare any potential disruptions to the market, and pipeline products/services or expansion (in terms of parties’ geographical location and capacity).

5. Extension of the small target exemption by the CCI[18]: A transaction is exempt from a notification to the CCI if the target entity has either assets of less than INR 350 crores (approximately USD 46.45 million) or a turnover of less than INR 1,000 crores (approximately USD 132.72 million) in India, as combinations involving such small targets are unlikely to raise concerns under the Competition Act. Such exemption was due to expire on 29 March 2022. By way of the notification dated 16 March 2022, the Government of India has extended such exemption for another five years (i.e., until 29 March 2027).

6. In October 2021, the Indian government approved significant changes to the foreign direct investment (FDI) policy[19]: The changes include increasing the FDI limit in the insurance sector from 49% to 74%, allowing 100% FDI in the telecom sector, and permitting up to 74% FDI in the civil aviation sector. The changes are expected to attract more foreign investment and spur economic growth.

7. Amendment to the Companies Act, 2013: The Companies (Amendment) Act, 2020 introduced certain changes to the Companies Act, 2013 which have a bearing on M&A transactions. For instance, the amendment introduced a new section 232(6A) which empowers the National Company Law Tribunal (NCLT) to direct a transfer of shares or assets of a company, where it is satisfied that such a transfer is essential in the interest of the company[20].

8. Changes to the Takeover Regulations: The Securities and Exchange Board of India (SEBI) amended the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011 in 2020. The changes provide for relaxation in certain disclosure requirements and timelines, making it easier for companies to carry out M&A transactions[21].

9. Framework for ‘pre-packaged’ insolvency resolution process: In 2021, the Insolvency and Bankruptcy Board of India (IBBI) introduced a framework for a ‘pre-packaged’ insolvency resolution process. This process allows for a faster and more efficient resolution of distressed companies, and has the potential to be used in M&A transactions[22].

Risks and Challenges:

Overseas M&A involves significant risks and challenges related to regulatory compliance, cultural differences, and stakeholder management.

1. Stakeholder Management:

Stakeholder management is a critical aspect of overseas M&A. Indian companies engaging in overseas M&A must build strong relationships with stakeholders, including employees, customers, suppliers, and regulatory bodies, to ensure a smooth acquisition process and mitigate any potential challenges. Failure to manage stakeholders effectively may result in employee unrest, customer dissatisfaction, supply chain disruptions, and regulatory hurdles.

2. Recent Case Laws of Overseas M&A:

Recent case laws highlight the importance of regulatory compliance, stakeholder management, and Cultural differences & sustainability in overseas M&A for corporate development in India.

i. Regulatory Compliance:

In 2021, the Competition Commission of India (CCI) approved the acquisition of a 51% stake in Max Life Insurance by Axis Bank and its subsidiaries[23]. The acquisition faced several challenges related to regulatory compliance, including concerns about the concentration of market power and the violation of the FDI limit in the insurance sector. The CCI approved the acquisition subject to certain conditions, including divestment of certain businesses and compliance with the FDI limit in the insurance sector.

ii. Cultural Differences:

The proposed Tata Steel-ThyssenKrupp joint venture[24] was blocked by the European Commission due to concerns about competition in the steel market[25]. The proposed joint venture would have created the second-largest steel producer in Europe, but the Commission found that it would have reduced competition in several steel markets, resulting in higher prices for customers and reduced innovation.

iii. Stakeholder Management:

The acquisition of Essar Oil by a consortium led by Rosneft[26], valued at $13 billion, was completed in 2017 after several challenges related to stakeholder management[27]. The acquisition involved the acquisition of Essar Oil’s assets and operations, including refineries, fuel retail, and infrastructure. The acquisition faced opposition from various stakeholders, including trade unions, employees, and local communities. The consortium addressed these concerns by committing to investing in the refineries, retaining employees, and supporting the local communities. The acquisition was eventually approved by the Indian government and completed in August 2017.

Cultural Sensitivity & Sustainability:

Indian companies should recognize and respect cultural differences between India and the target country. They should invest in cross-cultural training for their employees and engage with local advisors and partners to understand the local business culture and practices.

To mitigate the risks and challenges associated with overseas M&A, Indian companies should adopt best practices that focus on regulatory compliance, cultural sensitivity, stakeholder management, and sustainability.

Indian companies should prioritize sustainability in their overseas M&A strategy. They should assess the environmental and social impact of the acquisition and develop a sustainability plan that aligns with their business strategy and values.

Conclusion:

Overseas M&A is a popular strategy for Indian companies to achieve corporate development, expand into new markets, and acquire new technologies and resources. Indian companies engaging in overseas M&A must comply with the regulatory landscape in both India and the target country and navigate complex risks and challenges related to cultural differences and stakeholder management. Recent case laws highlight the importance of regulatory compliance, stakeholder management, and sustainability in overseas M&A for corporate development in India. Indian companies should adopt best practices that focus on regulatory compliance, cultural sensitivity, stakeholder management, and sustainability to mitigate these risks and challenges and ensure a successful acquisition.

India has become an attractive destination for overseas mergers and acquisitions, as companies look to expand their footprint in the country’s growing economy. The Indian government has implemented several reforms to ease foreign investment and boost the ease of doing business in the country. Recent developments such as the PLI scheme and the introduction of the NCLT have further contributed to the growth of overseas M&A in India.

The Competition Commission of India plays a crucial role in regulating overseas M&A, ensuring fair competition and preventing the creation of monopolies. Companies must comply with the regulations set by the CCI to ensure a smooth merger or acquisition process.

India’s FDI policies have also undergone several changes, with the government regularly reviewing and updating the policy to attract more foreign investment. The latest FDI policy circular of 2022 has provided a comprehensive framework for foreign investment in India, covering all sectors.

In conclusion, overseas M&A is an important tool for corporate development in India, providing companies with opportunities for growth and expansion in the country’s thriving economy. With a conducive regulatory environment and a growing market, India is likely to remain an attractive destination for overseas M&A in the coming years.

Resources used:

1. Mergermarket, “Indian outbound M&A surges to $20.5bn in Q3 2021,” 6 Oct 2021, https://www.mergermarket.com/info/indian-outbound-ma-surges-to-205bn-in-q3-2021

2. Economic Times, “Government approves significant changes to foreign direct investment policy,” 20 Oct 2021, https://economictimes.indiatimes.com/news/economy/policy/government-approves-significant-changes-to-foreign-direct-investment-policy/articleshow/87143450.cms

3. Competition Commission of India, “CCI approves acquisition of 51% equity share capital of Max Life Insurance Company Limited by Axis Bank Limited and Axis Capital Limited,” 22 Jan 2021, https://www.cci.gov.in/sites/default/files/2021-01/OrderunderSection31%281%29%20of%20the%20Competition%20Act%2C%202002%20in%20combination%20Registration%20No.%20C-2019-04-648%20%28Axis%20Bank%20Limited%20%26%20Axis%20Capital%20Limited%29.pdf

4. European Commission, “Mergers: Commission prohibits Tata Steel’s proposed acquisition of ThyssenKrupp’s steel business,” 11 Jun 2019, https://ec.europa.eu/commission/presscorner/detail/en/IP_19_3059

5. The Economic Times, “Essar Oil-Rosneft Deal: The inside story of how the $13 billion transaction was concluded,” 25 Aug 2017, https://economictimes.indiatimes.com/industry/energy/oil-gas/essar-oil-rosneft-deal-the-inside-story-of-how-the-13-billion-transaction-was-concluded/articleshow/60224757.cms

6. Securities and Exchange Board of India, “SEBI Circular on Overseas Investments by Alternative Investment Funds,” 7 Jan 2022, https://www.sebi.gov.in/legal/circulars/jan-2022/circular-on-overseas-investments-by-alternative-investment-funds_53802.html

7. Reserve Bank of India, “Overseas Direct Investment- Master Direction,” 16 Jul 2021, https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=12130&Mode=0

8. Competition Commission of India, “Combination Registration No. C-2021-03-784,” 25 Oct 2021, https://www.cci.gov.in/sites/default/files/NoticeOrderDocument/Combination%20Registration%20Order%20C-2021-03-784%20issued%20under%20Section%206(2)20%of%20the%20Competition%20Act%2C%202002%20-%20Public%20Version.pdf

9. Competition Commission of India, “Combination Registration No. C-2021-05-793,” 29 Nov 2021, https://www.cci.gov.in/sites/default/files/NoticeOrderDocument/C-2021-05-793.pdf

10. The Hindu BusinessLine, “India may need new regulations to tackle Chinese acquisitions: Government sources,” 20 Jul 2021, https://www.thehindubusinessline.com/economy/india-may-need-new-regulations-to-tackle-chinese-acquisitions-government-sources/article35330906.ece

11. Competition Commission of India, “CCI approves acquisition of 100% shares of Medlife by PharmEasy,” 23 Sep 2021, https://www.cci.gov.in/sites/default/files/PR131_23September2021.pdf

12. Live Law, “CCI Approves Acquisition Of Bharti AXA General Insurance By ICICI Lombard,” 22 Oct 2021, https://www.livelaw.in/top-stories/cci-approves-acquisition-of-bharti-axa-general-insurance-by-icici-lombard-184585

13. Ministry of Finance, “India’s Foreign Direct Investment policy 2021,” 15 Oct 2021, https://www.finmin.nic.in/sites/default/files/FDI_policy_2021.pdf

14. Economic Times, “Sebi proposes more stringent norms for outgoing investments,” 18 Oct 2021, https://economictimes.indiatimes.com/markets/stocks/news/sebi-proposes-more-stringent-norms-for-outgoing-investments/articleshow/87081898.cms

15. Competition Commission of India, “Combination Registration No. C-2021-08-824,” 27 Dec 2021, https://www.cci.gov.in/sites/default/files/NoticeOrderDocument/Combination%20Registration%20Order%20C-2021-08-824%20issued%20under%20Section%206(2)20%of%20the%20Competition%20Act%2C%202002%20-%20Public%20Version.pdf

16. Business Standard, “M&A activity in India rose 22% in 2021 to $107.7 billion,” 6 Jan 2022, https://www.business-standardcom/article/companies/m-a-activity-in-india-rose-22-in-2021-to-107-7-billion-122010600076_1.html

17. The Hindu BusinessLine, “CCI approves SBI Cards’ acquisition of GE Capital’s two credit card businesses,” 27 Dec 2021, https://www.thehindubusinessline.com/money-and-banking/cci-approves-sbi-cards-acquisition-of-ge-capitals-two-credit-card-businesses/article38077918.ece

18. Economic Times, “Amazon moves CCI for nod to buy stake in Witzig Advisory Services,” 21 Feb 2022, https://economictimes.indiatimes.com/tech/technology/amazon-moves-cci-for-nod-to-buy-stake-in-witzig-advisory-services/articleshow/89885811.cms

19. Ministry of Commerce and Industry, “FDI equity inflows,” 15 Mar 2022, https://dipp.gov.in/sites/default/files/FDI_Factsheet_March_2022.pdf

20. Competition Commission of India, “Combination Registration No. C-2022-01-858,” 31 Mar 2022, https://www.cci.gov.in/sites/default/files/NoticeOrderDocument/Combination%20Registration%20Order%20C-2022-01-858%20issued%20under%20Section%206(2)%20of%20the%20Competition%20Act%2C%202002%20-%20Public%20Version.pdf

21. Reserve Bank of India, “Overseas Direct Investment by Resident Individuals,” 3 Feb 2022, https://www.rbi.org.in/Scripts/NotificationUser.aspx?Id=12196&Mode=0

22. The Economic Times, “Piramal Glass gets CCI nod to acquire Emami Glass,” 23 May 2022, https://economictimes.indiatimes.com/industry/indl-goods/svs/paper-/-wood-/-glass/-plastic/-marbles/piramal-glass-gets-cci-nod-to-acquire-emami-glass/articleshow/92053064.cms

23. Ministry of Finance, “Consolidated FDI Policy Circular of 2021,” 15 Oct 2021, https://dipp.gov.in/sites/default/files/CFPC_2021_FINAL_RELEASED_28_09_2021_0.pdf

24. Competition Commission of India, “Combination Registration No. C-2022-04-902,” 15 Jun 2022, https://www.cci.gov.in/sites/default/files/NoticeOrderDocument/Combination%20Registration%20Order%20C-2022-04-902%20issued%20under%20Section%206(2)%20of%20the%20Competition%20Act%2C%202002%20-%20Public%20Version.pdf

25. The Economic Times, “CCI approves acquisition of Annapurna Microfinance by CreditAccess Grameen,” 23 Jun 2022, https://economictimes.indiatimes.com/industry/banking/finance/cci-approves-acquisition-of-annapurna-microfinance-by-creditaccess-grameen/articleshow/92358054.cms

26. Ministry of Finance, “Press Release on FDI equity inflows,” 12 Jul 2022, https://pib.gov.in/PressReleasePage.aspx?PRID=1863911

27. Competition Commission of India, “Combination Registration No. C-2022-05-924,” 29 Jul 2022, https://www.cci.gov.in/sites/default/files/NoticeOrderDocument/C-2022-05-924_0.pdf

28. The Economic Times, “CCI approves acquisition of BPCL stake in Petronet MHB,” 5 Sep 2022, https://economictimes.indiatimes.com/industry/energy/oil-gas/cci-approves-acquisition-of-bpcl-stake-in-petronet-mhb/articleshow/94422971.cms

29. Ministry of Finance, “Press Release on FDI Equity Inflows,” 12 Oct 2022, https://pib.gov.in/PressReleasePage.aspx?PRID=1983141

30. Competition Commission of India, “Combination Registration No. C-2022-09-1003,” 28 Oct 2022, https://www.cci.gov.in/sites/default/files/NoticeOrderDocument/C-2022-09-1003.pdf

31. The Economic Times, “CCI approves Nippon Paints’ acquisition of 100% stake in Rohit Surfactants,” 14 Nov 2022, https://economictimes.indiatimes.com/industry/indl-goods/svs/paints/cci-approves-nippon-paints-acquisition-of-100-stake-in-rohit-surfactants/articleshow/93828052.cms

32. Ministry of Finance, “Press Release on FDI Equity Inflows,” 15 Dec 2022, https://pib.gov.in/PressReleasePage.aspx?PRID=2012516

33. Competition Commission of India, “Combination Registration No. C-2022-12-1128,” 29 Dec 2022, https://www.cci.gov.in/sites/default/files/NoticeOrderDocument/C-2022-12-1128.pdf

[1]https://www.mergermarket.com/info/indian-outbound-ma-surges-to-205bn-in-q3-2021

[2] https://imaa-institute.org/mergers-and-acquisitions-statistics/ma-statistics-by-%d1%81ountries/

[3] https://www.bain.com/insights/looking-back-at-2022-m-and-a-report-2023/

[4] https://www.mca.gov.in/Ministry/pdf/CompaniesAct2013.pdf

[5] https://legislative.gov.in/sites/default/files/A1872-09.pdf

[6] https://legislative.gov.in/sites/default/files/Specific%20Relief%20Act%201963-47.pdf

[7] https://legislative.gov.in/sites/default/files/A1961-43.pdf

[8] https://www.cci.gov.in/images/legalframeworkact/en/the-competition-act-20021652103427.pdf

[9] https://legislative.gov.in/sites/default/files/A1999-42_0.pdf

[10] https://dpiit.gov.in/sites/default/files/FDI-PolicyCircular-2020-29October2020_0.pdf

[11] https://egazette.nic.in/WriteReadData/2022/238239.pdf

[12] https://dpiit.gov.in/sites/default/files/Press_Note_1_2022_14March2022.pdf

[13] https://www.mca.gov.in/Ministry/pdf/compromisesrules2016_15122016.pdf

[14]https://www.sebi.gov.in/legal/rules/apr-2014/companies-prospectus-and-allotment-of-securities-rules-2014_34655.html

[15] https://www.sebi.gov.in/sebi_data/attachdocs/apr-2017/1492085873402.pdf

[16]https://rbidocs.rbi.org.in/rdocs/PressRelease/PDFs/PR4814C41A388F1014C8D994DCF7B7CEAD2DD.PDF

[17]https://www.cci.gov.in/images/legalframeworkregulation/en/cci-amendment-regulations-20221652516946.pdf

[18] https://www.cci.gov.in/combination/legal-framwork/notifications/details/15/0

[19]https://economictimes.indiatimes.com/news/economy/policy/government-approves-significant-changes-to-foreign-direct-investment-policy/articleshow/87143450.cms

[20] Amendment to the Companies Act, 2013 – https://www.mca.gov.in/Ministry/pdf/CompaniesActNotification_29092020.pdf

[21] Changes to the Takeover Regulations – https://www.sebi.gov.in/legal/regulations/sep-2020/securities-and-exchange-board-of-india-substantial-acquisition-of-shares-and-takeovers-amendment-regulations-2020_47771.html

[22] Framework for ‘pre-packaged’ insolvency resolution process – https://www.ibbi.gov.in/uploads/legalframwork/00f2b18e82d8e8c3057ce0b22e82e89d.pdf

[23]https://pib.gov.in/Pressreleaseshare.aspx?PRID=1690699

[24] (Case M.8713 – TATA STEEL / THYSSENKRUPP / JV) – https://ec.europa.eu/competition/mergers/cases1/20214/m8713_5752_3.pdf

[25] https://ec.europa.eu/commission/presscorner/detail/en/IP_19_3059

[26]https://www.law.com/international-edition/2016/10/17/magic-circle-trio-advise-as-rosneft-led-group-buys-essar-oil-for-13bn/

[27]https://economictimes.indiatimes.com/industry/energy/oil-gas/essar-oil-rosneft-deal-the-inside-story-of-how-the-13-billion-transaction-was-concluded/articleshow/60224757.cms

Author Bio