Moving from the Companies Act 1956 to the Companies Act 2013 is like shifting from your old house to a new one. All the provisions become changed with new Act, 2013. Due to new act many amendments were introduce by Central Government from time to time by Notification, Amendments etc. Same like this many amendments have been made in last approximately 4 years in relation to Incorporation of New Company.

INTRODUCTION

The concept of Non-Profit making Company is quite old in India. In erstwhile, Companies Act, 1956 it was regulated by Section 25 and that is why it was popular as Section 25 Company. However in Companies Act 2013 provisions related to Non-Profit making Company are given in Section 8 read with Rule 19 and 20 of Companies (Incorporation) Rules, 2014.

Under Indian law, 3 legal forms exist for NGO or Non-Profit Organizations:

1. => Trusts

2. => Societies

3. => Section 8 Companies

Due to better laws, Section 8 Companies have the most reliable strongest organizational structure

1. => Indian Trusts have no central law.

2. => Indian Societies have different legal and institutional frameworks from state to state.

3. => Indian Companies (incl. Sec 8 companies), have one uniform law across the country – Companies Act, 2013.

It is this robust Act that regulates the formation, management and accountability of a Section 8 company, thus making it more closely regulated and monitored than trusts and societies, and recognized all over the world.

Through this article we shall talk about the basic provisions and procedure for incorporation of a Non-Profit creation Company as given in Section 8 read with Rule 19 and 20 of Companies (Incorporation) Rules, 2014.

Section 8 Company or a Non-Profit organization (NPO) is a Company established for promoting commerce, art, science, religion, charity or any other useful object, provided the profits, if any, or other income is applied for promoting only the objects of the Company and no dividend is paid to its members.

A NPO/NGO can be formed for promotion of any useful object like sports, education, research activities etc. The term Non Profit does not mean that the Company cannot generate profit or income, but it essentially means applying the income for further promotion of the object and not for distributing it to the promoters. It means that the Company can earn profits but the promoters cannot be benefited out of those profits.

Corresponding provisions of the Companies Act, 1956:

Section 25

Corresponding provisions of the English Companies Act, 2006:

Sections 42, 181 and 226

A COMPANY INCORPORATED UNDER SECTION 8 OF THE COMPANIES ACT 2013 IS:

As per Section 8 (1): A Non-Profit making Company is a Company which:

(a) Has in its objects the promotion of commerce, art, science, sports, education, research, social welfare, religion, charity, protection of environment or any such other object;

(b) Intends to apply its profits, if any, or other income in promoting its objects; and

(c) Intends to prohibit the payment of any dividend to its members.

IMPORTANT PROVISIONS:

IMPORTANT PROVISIONS RELATING TO SECTION- 8 COMPANIES:

> These Companies are incorporated only for promotion of commerce, art, science, sports, education, research, social welfare, religion, charity, protection of environment or any such other object.

> Non- Small Company:As per Section 2 (85) Proviso(B) – Section-8 Company will not be treated as Small Company.

> Status of Limited Company:As per Section 8(2) – Section 8 Company shall enjoy all the privileges and be subject to all the obligations of Limited Company.

It is the duty of Company to prove to Central Government that it will incorporate for above mentioned purpose only.

> License by Central Government:The Central Government may issue license with such conditions as it deems fit and allow the registration of such person or association of persons as a limited company without the addition to its name of the word “Limited”, or as the case may be, the words “Private Limited”.

> Power of CRC: The power of the Central government is delegated to the CRC, Registrar of Companies (‘CRC – ROC’) having Jurisdiction over the area where the Registered office of the company is proposed to be situated.Hence, the application for registering such Company is to be made to the CRC.

> Firm as a member of Non-Profit Making Company:As per section 8(3) a partnership firm may become a member of the Non-Profit making Company registered under section 8. Membership of such firm shall cease upon dissolution of the firm. However, partners of the dissolved firm may continue to be the members of such Company in their individual capacity

> Key Benefits:

- Many privileges and exemptions under Company Law vide notification dated 05thJune, 2015 and 13th June, 2017.

- Exemption of Stamp duty for registration.

- Registered partnership firm can be a member in its own capacity.

- Tax deductions to the donors of the Company u/s. 80G of the Income Tax Act.

> Without Share Capital: These Companies can be formed with or without share capital, in case they are formed without capital, the necessary funds for carrying the business are brought in form of donations, subscriptions from members and general public.

> Not Required To Add The Suffix: Section 8 Companies are not required to add the suffix Limited or Private Limited at the end of their name. All Companies having limited liability are required to use the term ‘limited’ or ‘private limited’ as the case may be in their names as required by section 13. But section 25 companies are allowed to dispense with the use of term ‘limited’ or ‘private limited’ from their names [sub-sec. (6)]. This helps the Company to enjoy limited liability without disclosing to the public the nature of liability of its members.

Suffix that can be use for incorporation: The name shall include the words Foundation, Forum, Association, Federation, Chambers, Confederation, council, Electoral trust and the like etc.

At present following words are not allowed for Incorporation of Section 8 Company; “Organization”, “Institute”, “word other than mentioned above”

Earlier these words were allowed for incorporation of Section 8 Company and even there are many section 8 companies ending with such prefix. Therefore, It can be opine “and the like etc” can’t use for incorporation of Section 8 Company as per latest Resubmissions or Rejections.

> Easy Transferable Ownership:The shares and other interest of any member in the Company shall be a movable property and can be transferable in the manner provided by the Articles, which is otherwise not easily possible in other business forms. Therefore, it is easier to become or leave the membership of the Company or otherwise it is easier to transfer the ownership.

DISADVANTAGE:-

The DISADVANTAGES of section 8 Companies over other Companies registered under Companies Act are discussed below:

Though a Section 8 Company has many advantages and enjoys many privileges yet there are some statutory obligations which are required to be complied with and taken care of by such companies.

> Key Conditions:

Profit or Income of the Company shall be applied for the promotion of the main object.

- Declaration of dividend or distribution of profit to the promoters is not allowed.

- No member shall be appointed as a remunerated officer.

- No remuneration / benefit shall be paid to a member being a servant / officer of the Company (except reimbursement of out of pocket expenses, reasonable interest on money lent or reasonable rent on the premises).

> Utilization of Profit:A Section 8 Company has to ensure that its profits and all other incomes are utilized only for the purpose of promoting its objects and not for any other purpose.

> It should also ensure that its profits are not distributed as dividend among its members.

> No Change in AOA and MOA:A Company registered under this section shall not alter the provisions of its Memorandum or Articles except with the previous approval of the Central Government. Power of Central government has been delegated to ROC,

> Condition by Central Government:If the Central Government has imposed some conditions and regulations upon the Company for granting a license under section 8 then such a Company is bound by such conditions and has to ensure adequate compliance with them. Where such conditions and regulations have been imposed then such conditions and regulations are required to be included in the Articles or/and Memorandum of the Company as may be directed by the Government.

> Tax Liability:Section 25 Company is regarded as a ‘Company’ within the meaning of the Income Tax Act, 1961 and as such its income is taxable according to the applicable rates similar to those applying to other Companies.

THE PROCEDURE FOR INCORPORATION OF SECTION-8 COMPANY IS AS FOLLOWS:-

PRE INCORPORATION:

1. NORMAL CONDITIONS:

- At Least 2 Promoters: Promoters who will promote/ incorporate the Company. Promoters may be individual or body corporate.

- At Least 2 Directors:Directors should be individual only. No Body corporate/ HUF or Partnership Firm can be appointed as Directors.

- Generally, in most of the cases, Promoters and Directors are the same in Private Limited Companies.

2. OBTAIN DIGITAL SIGNATURE–All the Subscribers required DSC. As per Ministry of Corporate Affairs, Class-II DSC is required for e-Filings under MCA21. Subscriber can apply with any of DSC Vender i.e. E Mudra/ Siffy/ TCS etc

3. OBTAIN DIN–As envisaged under section 153, an individual intending to become Director needs to obtain DIN. In case of proposed director doesn’t having DIN, in such case he have to apply for DIN along with Incorporation in SPICE+ Form.PROCESS OF

INCORPORATION

SPICe+ would have two parts viz.:

A. Part A – Name Approval

B. Part-B- Incorporation of Company

STEP – I:

PART A-for Name reservation for new companies

A. Login on MCA Website

Applicant have to login into their account on MCA Website. (Pre-existing users can use earlier account or new users have to create a new account.)

After Login the following screen will appear:

B. Steps: II Click on New Application and following window will open:

(This form can’t be downloaded; it has to be filled on real time basis)

Details required to be mentioned in online form:

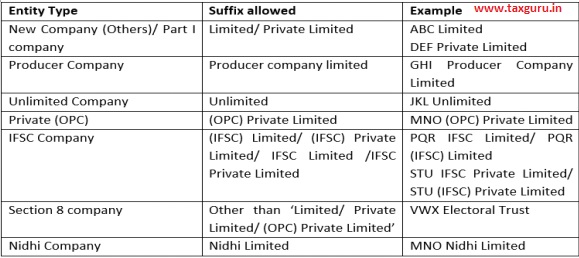

(i) Type of Company (i.e. Producer, Part I, OPC, Section 8 etc.)(below table taken from MCA link: http://www.mca.gov.in/MinistryV2/SPICePlusFAQs.html

(ii) Class of Company (whether Private, Public, OPC)

(iii) Category of Company (whether Company limited by shares, limited by Guarantee or unlimited)

(iv) Sub-category Union Government, State Government, Non-Government Company, Subsidiary of Company incorporated outside India)

(v) Main Division of Industrial Activity (enter number belonging to Industrial Activity)

(vi) Description of main division

(vii) Particulars of Proposed or Approved Name. (User has to enter the name he wants to reserve, for incorporation of a new company. Users are requested to ensure that the proposed name selected does not contain any word which is prohibited under Section 4(2) & (3) of the Companies Act, 2013 read with Rule 8 of the Companies (Incorporation) Rules, 2014. Users are also requested to read and understand Rule 8 of the Companies (Incorporation) Rules, 2014 in respect of any proposed name before applying for the same. For Name Search: http://www.mca.gov.in/mcafoportal/showCheckCompanyName.do)

Stakeholders are requested to also check the Trademark search to ensure that the proposed name is not in violation of provisions of Section 4(2) of the Companies Act, 2013, failing which it is liable to be rejected. For Trade Mark Search: http://www.ipindia.nic.in/index.htm

Note: Two fields are available ie the two proposed names can be entered

(i) Choose File (Any attachment)

This option is available to upload the PDF documents. It is not mandatory to attach any document except in case where a name which requires the approval of a Sectoral Regulator or NOC etc, if applicable, as per Companies(Incorporation) Rules, 2014. Only one file is allowed, if have multiple then scan into one document. The attachment size cannot exceed 6 MB for both Part A and Part B taken together.

Steps: III Fill the given Information and save the application as follows:

- Fill the Information

- Save the Application

- Submit the Application

After Submit below given window will open:

C. Here stake holder having two options:

C. Here stake holder having two options:

Option 1: Submit Name application and make payment of the same for name approval. Payment of Rs. 1,000/-

Option 2: Click on “Proceed for Incorporation”

After click on “Proceed for Incorporation” below given window will open:

NOTE: * Approval of Name through “PART-A” is an optional way. Companies can also directly apply for the Information after continuation with PART B form.

It is advisable to go through PART-A route

Part B- Incorporation of Company

AFTER NAME APPROVAL PROCESS:

Once Name is approved by ROC, following are the Pre-Incorporation Steps:

DRAFTING OF MEMORANDUM OF ASSOCIATION (MOA) AND ARTICLE OF ASSOCIATION (AOA):

MOA: FORM NO. INC 13

Drafting of Memorandum of Association (MOA) and Article of Association (AOA) is generally a step subsequent to the availability of name made by the registrar. It should be noted that the main objects should match with the objects shown in RUN.

These two documents are basically the charter and internal rules and regulations of the Company. Therefore, it must be drafted with utmost care and with the advice of the professional. The Directors/ promoters with the help of professional draft MOA and AOA.

AOA:

Article of Association contains the internal regulations of the Company so care should be taken while drafting it. The model articles are given under table F of Schedule I. Now under Companies Act, 2013 requirement for making alteration to certain clauses of AOA can be made more stringent by way of inserting entrenchment provision.

Also ensure that the MOA & AOA are not ultra-vires the law (Section 6)

MOA:

- The formats of MOA are given inForm INC-13.

- Format of MOA and AOA revised from time to time because of change in Companies Act and recently Companies Act 2013 laid down another form of MOA which has total twelve clause.

- MOA of Section 8Company registration (previously called section 25 companies) has been prescribed in form INC-13 by the Companies Act 2013 followed by rule 19 sub rule 2 of Companies Incorporation Rule 2014.

Procedure for drafting MOA of section 8 Company start from:

1st clause which contain name of the section 25 or 8 company example XYZ Foundation or XYZ association etc.

Second clause state to mention state in which registered office of the proposed section 8 Company will be situated example NCT of Delhi for Delhi or State of Haryana for Haryana etc.

Third clause of INC-13 i.e. MOA contains charitable object of section 8 company i.e. to establish industrial training center or college or social service center etc. i.e. only object having charitable purpose and restricted company to support with its fund which will make trade union or other company which are observed by its member.

Clause 4 of moa clearly mention that object of the company extend whole of India except J & K.

Clause 5 of the MOA restricted diversion of section 8 company income or property to any of its member or its related party in any form. It has also been clarified that profit of such company can only be utilized for its charitable object. Prudent Remuneration allowed to its member only when he actually provides services to the company.

Clause 6 provides that Memorandum of Association cannot be altered unless alteration has been previously approved by the registrar of company

Clause 8 state liability of the member is limited

Clause 9 required to maintain certain record and books for expenditure income assets etc. and once in an every year accounts shall be examined by auditor about correctness of balance sheet and income & expenditure.

Clause 10 mentioned about dissolution of Section 8 Company and whereas

Clause 11 states section 8 company can be amalgamated only with section eight company having similar object and

Clause 12 contains detail of subscriber of MOA. Format of AOA of section eight company is same as for Private Limited Company registration.

STEP – II: Preparation of Documents for Incorporation of Company:

| Form | Attachments | |

|

SPICE |

1. Memorandum of Association – INC 13 2. Articles of Association 3. Copy of PAN Card 4. Copy of ID proofs 5. Copy of Address Proofs 6. Directorship/Promoter ship in other companies(if more than 3) 7. Consent in DIR-2 along with ID& Address proof 1. Utility Bill, not older than 2 months old 2. Proof of registered office address 8. No objection certificate in case registered office is not taken on lease |

MANDATORY |

| 9. Board Resolution (Body corporate subscriber)

10. Certificate of Incorporation & proof of registered office (Foreign Body corporate subscriber) 11. Proof of Nationality(In case of foreign national) 12. Declaration by foreigner if he does not possess PAN (as per MCA circular 16/2014) 13. NOC in case there is change in the promoters 14. Principal approval taken from RBI for carrying NBFC activity 15. Declaration By Professionals INC-14 16. Declaration By Promoters INC-15 17. Estimated Annual Income: An estimate of the future annual income and expenditure of the company for Next Three Years, specifying the sources of the income and the objects of the expenditure 18. Brief profile of all the promoters: List of names, descriptions, addresses & occupation of the promoters as well as Board Members of the proposed company and ID Proof, Directorship, Shareholder ship etc |

AD-HOC | |

# Obtains Following Documents/Information from Subscribers: –

| S. NO. | PROVISION | PARTICULARS | REMARKS |

|

A. |

Section 8(1)

+ Rule 19 |

ID Proof (PAN + Voter ID/Passport /Driving License/Aadhar Card) | For foreign nationals and NRI only passport will suffice |

| Address Proof both permanent & present (Electricity/Telephone/ Mobile Bill/ Bank Statement) | The proofs should not be 2 months old | ||

| Proof of nationality (Applicable only to foreign nationals) | Although all subscribers can be foreigners but at least 1 director should be resident (section 149(3)) | ||

| Disclosure of Directorship /promotership in other companies | Refer definition of promoter (Sec. 2(69)) | ||

| B. | Section 7(1)(e) + Rule 16 |

In case subscriber is a Body Corporate: –

|

· In case Body Corporate is LLP the resolution should be approved by all partners.

(Proviso to rule13(4)) |

| C. | Section 7(1)(e) + Rule 16 |

Following information is also required from subscriber: –

|

Address, e-mail id & phone no. should be of subscriber only and not professional. |

OBTAIN FOLLOWING DOCUMENTS/INFORMATION FROM DIRECTORS:

| S. NO. | PROVISION | PARTICULARS |

| A. | Section 7(1)(g)

+ Rule 17 |

|

| B. | Form DIR-2 | Following information is also required from subscriber: –

|

OBTAIN FOLLOWING DOCUMENTS/INFORMATION FOR SITUATION OF REGISTERED OFFICE:

Situation of Registered Office: – The address of registered office may be intimated by the Promoters at the time of Incorporation or as per section 12 within maximum 30 days of Incorporation. In case address of registered office is not decided then address for correspondence needs to be given. The documents/information required in case the address of registered office is to be intimated at the time of Incorporation are: –

| S. NO. | PARTICULARS |

| A. | Complete address of Police station in whose jurisdiction the registered office is situated |

| B. | Utility Bill, not older than 2 months old(electricity/gas/telephone/mobile bill) |

| C. | Proof of registered office address(Conveyance/lease deed/rent agreement along with rent receipts) |

| D. | No objection certificate in case registered office is not taken on lease |

STEP – III: Fill the Information in Form:

Once all the above-mentioned documents/ information is available. Applicant has to fill the information in the e-form “Spice+”.

Features of SPICe+ form:

√ Web based: This is web-based form, that means this form can’t be download. It will be filled on MCA website online only.

√ Online Information:This form once online information filed will be save there only and can be access in dash board of the Log in ID.

√ Fill details of PAN & TAN:

I is mandatory to mention the details of PAN & TAN in the Incorporation Form Spice+. Link to find out of Area Code to file PAN & TAN are given in Help Kit of SPICE+.

√ Attachment of Documents:In web-based form only promoters have to attach documents pdf files.

√ Download PDF form:After complete filing of information in web-based form. Download PDF file of the form from dashboard.

√ Process after Downloading of PDF:Below given steps have to use for incorporation of company.

STEP – IV: Preparation of MOA & AOA (Electronic or Physical):

After proper filing of SPICE+ form applicant has to move on filling of information in MOA and AOA form Dashboard Link. All the information which are common in PART-B and MOA/AOA shall be auto fill in MOA and AOA.

- MOA and AOA are also web-based forms which shall be available on dash board in particular link.

- After opening of web-based form fill all the information in the MOA/ AOA as per requirement of Table A to J of Schedule I.

- After completely filing of the MOA/ AOA download PDF MOA/AOA.

- After download PDF affix DSC of all the subscribers and professional on subscriber sheet of the MOA & AOA.

(Make Sure Professional and Subscriber sign the form on same date)

STEP – V: Fill details of GST, EPFO, ESIC, BANK Account in AGILE PRO:

After proper filing of SPICE+, Moa, AOA form applicant has to move on filling of information in the AGILE PRO form Dashboard Link. All the information which are common in PART-B and AGILE PRO shall be auto fill in AGILE Pro. It is also web based form.

- GST:If Company wants to apply for GST it has to select YES in the form and fill the information in the form.

- EPFO/ ESIC:It is mandatory to apply for ESIC and EPFO.

- However, as per their concerned department company not required to file return till the date applicability of provisions of same on such company.

- Bank Account:It is mandatory to open bank account through this form. Bank account branch shall be assigned according to nearest branch to the Registered office of the Company.

STEP – VI: Fill details of INC-9:

INC-9 shall also be generated web-based and need affixation of Directors/ subscribers on the same. It shall not be generated web-based in one situation when atleast one directors/ subscriber not having DIN and PAN both.

STEP – VII: Download PDF of all the web-based forms-:

After filing of all web-based form i.e.

- Spice+

- MOA/ AOA

- Agile Pro

- INC-9

Download PDF of such forms from dash board given link. After downloading of PDF affix DSC on all the forms accordingly.

STEP – VIII: Filing of forms with MCA-:

Once all forms ready with the applicant, upload all four document as Linked form on MCA website and make the payment of the same.

STEP – IX: Certificate of Incorporation-:

Incorporation certificate shall be generated with CIN, PAN & TAN details over it.

KEY POINTS OF SPICE+:

a) Stakeholders will not be required to even enter the SRN of the approved name as the approved Name will be prominently displayed on the Dashboard and a click on the same will take the user for continuation of the application through a hyperlink that will be available on the SRN/application number in the new dashboard.

b) From 15th February 2020 onwards, RUN service would be applicable only for ‘change of name’ of an existing company

c) The approved name and related incorporation details as submitted in Part A, would be automatically Pre-filled in all linked forms also viz., AGILE-PRO, eMoA, eAoA, INC-9

d) Registration for EPFO and ESIC shall be mandatory for all new companies incorporated w.e.f 15 February 2020 and no EPFO & ESIC registration nos. shall be separately issued by the respective agencies

e) Registration for Profession Tax shall also be mandatory for all new companiesincorporated in the State of Maharashtra w.e.f 15th February 2020

f) All new companies incorporated through SPICe+ (w.e.f 15th February 2020) would also be mandatorily required to apply for opening the company’s Bankaccount through the AGILE-PRO linked web form.

g) Declaration by all Subscribers and first Directors in INC-9 shall be auto-generated in pdf format and would have to be submitted only in Electronic form in all cases, except where:

(i) Total number of subscribers and/or directors is greater than 20 and/or

(ii) Any such subscribers and/or directors has neither DIN nor PAN.

POINTS TO REMEMBER WHILE FILLING THE INFORMATION IN FORM:

- Maximum details of subscribers are SEVEN (7). In case of more subscribers, physically signed MOA & AOA shall be attached in the Form.

- Maximum details of directors are TWENTY (20).

- Maximum THREE (3) directors are allowed for filing application of allotment of DIN while icorporating a Company.

- Person can apply the Name also in this form.

- By affixation of DSC of the subscriber on the INC-33 (e-moa) date of signing will be appear automatically by the form.

- Applying for PAN/TAN/EPFO/ESIC/Bank Account will be compulsory for all fresh incorporation applications filed in the new version of the SPICe plus form.

- Company can apply for GST, also through AGILE PRO form.

- In case of companies incorporated, with effect from the 26th day of January, 2018, with a nominal capital of less than or equal to rupees fifteen lakhs or in respect of companies not having a share capital whose number of members as stated in the articles of association does not exceed twenty, ROC fee on SPICE+ shall not be applicable

————————————————————-

FEATURES – SINGLE WINDOW FORM:

Earlier if a Person wants to incorporate Company then it has to apply for the DIN, Approval of the Name Avaibility, Separate form for first Director, Registered office address, PAN, TAN etc. But this form is a single window for Incorporation of Company.

This form can be used for the following purposes:

- Application of DIN (upto 3 Directors)

- Application for Avaibility of Name

- No need to file separate form for first Director (DIR-12)

- No need to file separate form for address of registered office (INC-22)

- No need to file separate form for PAN & TAN

- No need to file separately for GST,

- No need to file separate form for EPFO, ESIC, Profession tax

- No need to file separate application with bank for Bank account number..

QUICK QUESTION – SPICE+

i. How to file the SPICe+ form in case of more than 7 subscribers in the Company?

In case of incorporation of a company having more than 7 subscribers, MOA & AOA shall be filled with SPICE+ in the respective format as specified in Table A to J in Schedule I without filing form INC 33 and INC 34.

(Means Physical attachment of MOA & AOA in e-form INC 32)

ii. Whether e-MOA & AOA can be filed in case of MOA & AOA is signed by a person at a place outside of India?

In case of incorporation of a company where any of the subscribers of the MOA/AOA is signing at place outside India, MOA & AOA shall be filled with SPICE+in the respective format as specified in Table A to J in Schedule I without filing form INC 33 and INC 34.

(Means Physical attachment of MOA & AOA in e-form INC 32)

iii. Whether Companies are required to make payment of Stamp Duty in case of incorporation of Company with authorized Capital of Rs. 10 Lakh or below?

Yes, Company has to pay the Stamp Duty. Because Stamp Duty is state’s matter. Companies Act, has given exemptions for the ROC fees not for the stamp duty.

iv. ow many DIN can be apply through SPICE+ Form?

Maximum 3 (Three) DIN can be apply through SPICE+ form.

If applicant want to incorporation Company with more than 3 Directors and more than 3 persons doesn’t have DIN. In such situation applicant have to incorporate Company with 3 Directors and have to appoint new directors later on after incorporation.

v. Whether there is need to file any separate form for PAN & TAN?

No need to file any separate form. Details in relation to Area Code and other details shall be mention in the form SPICE+ itself and PAN & TAN shall be generate with Certificate of Incorporation.

OTHER FORMALITIES:

OTHER INCORPORATION FORMALITIES: After obtaining license under section 8, the company shall be formed as a normal company and the other formalities of incorporation shall be complied with.

REGISTRATION UNDER SECTION 80G: If a section 8 company gets itself registered under section 80G then the person or the organization making a donation to the NGO will get a deduction of 50% from his/its taxable income. The Company has to apply in Form10G to the Commissioner of Income Tax for such registration. Normally this approval is granted for 2-3 years but can be granted earlier depending upon the situations.

Author – CS Divesh Goyal, GOYAL DIVESH & ASSOCIATES Company Secretary in Practice from Delhi and can be contacted at csdiveshgoyal@gmail.com).

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness and reliability of the information provided, I assume no responsibility therefore.

(Republished with amendments)

Author Bio

Are CRC And ROC Same?

Very informative article.

Very informative and helpful.

What is the rough estimate of ROC fees for Filing SPICE+ for SEction Company having no Share Capital?

very much informative and clear. Thanks a lot for your uploadings.