Article discuss the Criticalities in preparation of MSME-1 Data and form for the half year ended 30.09.2019 and for subsequent half year periods. It discusses What should be financial year for form MSME-1, which period data should be considered and many more things. In this editorial we will discuss the most asked questions on Filing of MSME Form 1.

Extract of Act:

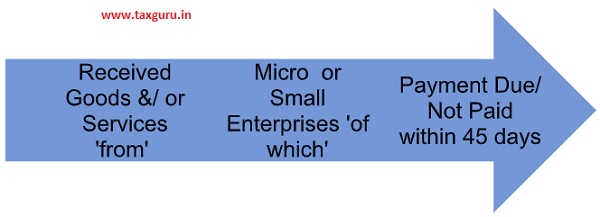

2. Every specified company shall file in MSME Form I details of all outstanding dues to Micro or small enterprises suppliers more than 45 days as at end of half year.

3. Every specified company shall file a return as per MSME Form I annexed to this Order, half Year as per details given below

| S. No. | Period | Due Date |

| 1. | Period April to September | 31st October |

| 2. | Period October to March | 30th April |

As per provisions of Companies Act, 2013 Specified Companies are required to file e-form MSME-1 till 31st October, 2019 for the outstanding as on 30.09.2019.

FAQ’s

Q.1 If payment of any MSME vendor is outstanding as on 30.09.2019 and date of invoice is any period before 01.04.2019.

Whether details of such outstanding invoice need to mention in MSME-1 filed for half year ended 30.09.2019?

Ans. As per provisions of the Act and language of the form, Companies have to give details of outstanding payment to MSME vendor as on 30.09.2019.

Therefore, one can opine that even the date of invoice is before 01.04.2019 Companies have to give details of same in MSME-1.

Q.2 What would be the financial year to date in form MSME since it doesn’t accept date beyond system date?

Ans. There are two situations to mention the financial year.

If date of invoice between 01.04.2019 to 30.09.2019

Financial year shall be 01.04.2019 to 30.09.2019

Q.3 If as on 30.09.2019 the is no outstanding payment to MSME vendor, Whether companies need to file MSME-1?

Ans. If there is no outstanding payment as on 30.09.2019, then there is no need to file e-form MSME-1. Even form also not accepts with NIL Data.

Q.4 If as on 30.09.2019 the is no outstanding payment to MSME vendor, But there was delay in payment of some MSME vendor more than 45 days which has been paid on or before 30.09.2019. Whether Company needs to give details of such invoices in the form?

Ans. As per provisions of the Act and language of the form, Companies have to give details of outstanding payment to MSME vendor as on 30.09.2019.

Therefore, one can opine that if company has already made payment to vendors before 30.09.2019, then company is not required to give details of such transaction in MSME-1.

Q.5 What are the consequences if company files e-form MSME-1 after due date i.e. 31.10.2019.

Ans.

| Penalty on | Minimum Fine | Fine can Extend Upto |

| Company | Rs. 25,000/- | Rs. 25,000/- |

| Officer in Default (KMP, Directors) | Rs. 25,000/- | Rs. 300,000/- |

Q.6 If there is any payment outstanding to MSME Vendor as on 30.09.2019. However, delay is less than 45 days whether companies need to give details of same in the form MSME-1?

Ans. As per provisions of the Act, Company have to follow two conditions to fall under limits of Specified Company:

- Vendor is Register under MSME-1

- Payment is delayed by more than 45 days

Q.7 If company has entered into agreement with MSME vendor for payment within 60/90 days. Whether such agreement shall be valid as per MSME Act.

Ans. As per section 15 of MSME Act, “in no case period agreed between supplier and buyer in writing shall exceed 45 days from day of acceptance.

Therefore one can opine that, agreement between supplier and buyer for payment after 45 days doesn’t have any effect in filing of MSME-1. Because as per MSME Act, supplier and buyer cannot decide day more than 45 days.

A. Which Companies falls under MSME

The limit for investment in plant and machinery / equipment for manufacturing / service enterprises, as notified, vide S.O. 1642(E) dtd.29-09-2006 are as under

| Manufacturing Sector | |

| Enterprises | Investment in plant & machinery |

| Micro Enterprises | Does not exceed Rs. 25,00,000/- (Twenty Five Lakh) |

| Small Enterprises | More than Twenty Five Lakh (25,00,000) rupees but does not exceed Five Crore Rupees (50,000,000) |

| Medium Enterprises | More than Five Crore (50,000,000) rupees but does not exceed Ten Crore (100,000,000) rupees |

| Service Sector | |

| Enterprises | Investment in equipments |

| Micro Enterprises | Does not exceed Ten Lakh rupees (Rs. 1,000,000): |

| Small Enterprises | More than Ten Lakh rupees(Rs. 1,000,000) but does not exceed Two Crore (20,000,000) rupees |

| Medium Enterprises | More than Two Crore (20,000,000) rupees but does not exceed five core rupees (50,000,000) |

B. Which are Specified Companies:-

Every Company “PUBLIC OR PRIVATE” if falls in below mentioned condition:

C. Which type of entities cover under Micro and Small entities?-

C. Which type of entities cover under Micro and Small entities?-

| Proprietorship, | Hindu Undivided Family, |

| Association of Persons, | Co-Operative Society, |

| Partnership Firm, | Company or |

| Undertaking |

D. Which form Specified Company required to file with ROC:-

Specified Companies are required to file returns with ROC in e-form MSME-1:

Two Type of Returns required filing by “Specified Companies” like:

- One Time Return

- Half Yearly Return

E. If a Company falls in criteria of MSME, However not registered under MSME Act. Whether Company need to mention details of such MSME in their reporting?

As per language of Notification, If a Company registered under MSME Act and having a valid MSME certificate. Then only required to include in reporting while filing of MSME-1.

Therefore, one can opine that, Details of only registered MSME required filing with ROC in form MSME-1.

F. Whether Udyog Aadhar Registration shall be considered as MSME Registrations.

As per MSME Act Udyog Aadhar is a way out to get registration of MSME. Therefore, such registration shall be considered as MSME Register.

G. Whether there is any limit on amount of transaction with MSME?

As per MSME Act, 2006; Limit of amount doesn’t matter to check whether payment made in 45 days or not.

For an EG. If due amount is Rs. 100/- only and doesn’t made payment in 45 days. Specified Companies needs to report the same to ROC in e-form MSME-1.

H. How to identify whether creditors entity falls under Micro and Small or not?-

For the purpose of reporting under MSME Form-1. Company should be aware that creditor’s entity is Micro or Small or not.

Therefore,

- Company have to ask a declaration from the creditors whether they falls under Micro or small or not and whether as on date they meet criteria of MSME.

- Company has to ask for copy of certificate of registration under MSME.

I. Whether Traders and Retailers can get registration under MSME?

As per our understanding of MSME Act, Only manufactures and service provides as mentioned above can get registration under MSME.

J. What are consequences for non filing of the MSME form?

As per section 16 of MSME Act, if buyer make

- Delay in payment more than 45 days or

- Delay in payment from agreed term or

- Delay in 15 days payment where no term agreed

In such case buyer is liable to pay compound interest with monthly restes to the supplier on that amount from the appointed day, at three times of the bank rate notified by RBI.

Therefore one can opine that, consequences nonpayment within above mentioned specified time buyer liable to make payment of heavy interest.

(Author – CS Divesh Goyal, GOYAL DIVESH & ASSOCIATES Company Secretary in Practice from Delhi and can be contacted at csdiveshgoyal@gmail.com).

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness and reliability of the information provided, I assume no responsibility therefore. Users of this information are expected to refer to the relevant existing provisions of applicable Laws. The user of the information agrees that the information is not a professional advice and is subject to change without notice. I assume no responsibility for the consequences of use of such information. IN NO EVENT SHALL I SHALL BE LIABLE FOR ANY DIRECT, INDIRECT, SPECIAL OR INCIDENTAL DAMAGE RESULTING FROM, ARISING OUT OF OR IN CONNECTION WITH THE USE OF THE INFORMATION

Author Bio