Introduction

Debenture: The word ‘debenture’ has been derived from a Latin word ‘debere’ which means to borrow. Debenture is a written instrument acknowledging a debt to the Company. It contains a contract for repayment of principal after a specified period or at intervals or at the option of the company and for payment of interest at a fixed rate payable usually either half-yearly or yearly on fixed dates.

Debenture includes debenture stock, bonds and any other securities of a company whether constituting a charge on the assets of a company or not as defined in the Companies Act. This is an inclusive definition and amounts to borrowing of monies from the holders of debentures on such terms and conditions subject to which the debentures have been issued.

This is an inclusive definition and amounts to borrowing of monies from the holders of debentures on such terms and conditions subject to which the debentures have been issued. Basically it is a document or certificate signed by the authorized officers of a company acknowledging money lent and guaranteeing repayment with interest and creating security on the assets of the company for due performance of its obligation.

A debenture means a document, which creates or acknowledges a debt. [Levy vAbercorries State Co. (1887) 37 Ch D 260]

GOVERNING SECTIONS:

- Section 2(30): Definition of Deposit: “debenture” includes debenture stock, bonds or any other instrument of a company evidencing a debt, whether constituting a charge on the assets of the company or not.

- Section 44: Nature of Share and Debenture.

- Section 71: Provision relating to Debentures.

- Section 117(3) (a)A copy of every resolution or any agreement, in respect of the matters specified in sub-section [1](3) of section 17 together with the explanatory statement under section 102, if any, annexed to the notice calling the general meeting in which the resolution is proposed, shall be filed with the Registrar within thirty days of the passing of resolution.

- Section 179 (3) (c,d): (c) to issue securities, including debentures, whether in or outside India;

*(d) to borrow monies;

- Section 180(1) (c): The Board of Directors of a company shall exercise the powers “borrow money”, where the money to be borrowed, together with the money already borrowed by the company will exceed aggregate of its paid-up share capital and free reserves, only with the consent of the company by a special resolution, namely.

- Section 56(4) (d):within a period of six months from the date of allotment in the case of any allotmentof debenture.

- Section 42: Offer or invitation for subscription of securities on Private Placement.

- GOVERNING RULES:

- Rule 18of the Companies (Share Capital and Debentures) Rules, 2014:

- Rule 24 The Companies (Management and Administration) Rules, 2014: Resolutions and agreements to be filed.

- Rule 1(c) of The Companies (Acceptance of Deposits) Rules, 2014: “Deposit” does not include

“Any amount raised by the issue of debentures secured by a first charge or a charge ranking paripassu with the first charge on any assets referred 73 Proviso to in Schedule III of the Act excluding intangible assets of the company or debentures compulsorily convertible into shares of the company within five years.”

- Rule 14 of the Companies (Prospectus and Allotment of Securities) Rules, 2014: Process of Issue and allotment of Securities (Debentures).

- FORMS INVOLVED:

- MGT– 14: Filing of Special Resolutions to the Registrar of Companies.

- [2]MGT – 14: Filing of resolution for issue of Debenture.

- PAS-4: Letter of offerfor Private Placement of Securities

- PAS-5: Record of a private placement offer to be kept by the company

- GNL: 2 Form for submission of PAS-4 & PAS-5 with Registrar of Companies

- SH-12: Debenture Trust Deed

- PAS-3: Return of allotment

- CHG-9: forcreation of charge on assets of the Company

- DRAFTING INVOLVED:

- Debenture Subscription Agreement.

- Letter of offer of Private Placement of Shares

- Debenture Trustee Agreement, if required.

- Mortgage Agreement for creation of charge on assets of the company, if required.

PURPOSE OF FILING OF FORMS:

- MGT-14:This form is required to be filed within 30 days of passing of Special resolution for All The Companies including Private Limited Company {Section 117(3)(a)}.

- MGT-14:This form is required to be filed within 30 days of passing of resolution to issue securities, including debentures, whether in or outside India {Section 179(3)(c)}.

- GNL-2:PAS-4 & PAS-5 are physical form will file with ROC in e-form GNL-2.

RESOLUTION REQUIREMENT:

Special Resolution:A Special resolution is required to be passed at a General Meeting of the Company for following purposes:

- To issue Debentures.[Section 71(1)first proviso].

- To increase borrowing power of the Company, if Required.

First Board Resolution:Board resolution is required to be Pass for following purposes:

- Pass resolution to increase borrowing power of the Company, subject to approval of Shareholders.

- Pass resolution to issue Debentures, subject to approval of Shareholders.

- Approval of draft offer letter (PAS-4) for issue of Debentures.

- Take note of valuation report

- Approval of draft Debenture Trustee Agreement and appointment of a Debenture Trustee.

- Issue the Notice of General Meeting along with explanatory statement. (According to SS-2).

- Authorize a Company Secretary or director of company to issue notice of General Meeting.

- Open Separate Bank Account: for receipt of money on issue of debentures.

Second Board Resolution:Board resolution is required to be Pass for following purposes:

- To allot Debentures.

- To authorize directors to issue and sign the debenture certificates.

- To authorize director of the company to file e-form PAS-3 for allotment of Security.

- To authorize director of the company to file e-form CHG-9 for Creation of Charge.

CIRCULARS/ NOTIFICATIONS/ AMENDMENT RULES:

- The Companies (Share Capital and Debentures) first Amendment Rules, 2014 dated 18th June, .2014

- The Companies (Share Capital and Debentures) Second Amendment Rules, 2015 dated 18th March, 2015.

| Section

under CA 2013 |

Section

under CA 1956 |

Matters dealt with |

| 2(30) | 2(12) | Meaning of Debentures |

| 56(4)(d) | 108, 108A to 108L, 109, 110, 113 | Issuance of debenture certificate within 6 months from the date of allotment |

| 71 | 117, 117A to 117C, 118, 119 122 | Debentures |

| 77 | 125, 128, 129, 132, 133, 145 | Duty to Register charges on secured debentures |

| 136 | 219 | Right of Debenture holders to obtain copy of the Annual Accounts |

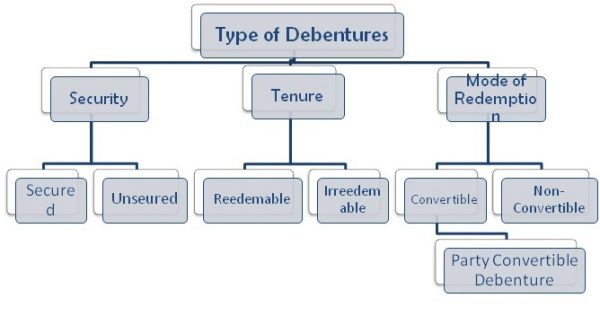

Security:

(a)Secured Debentures: Secured debentures refer to those debentureswhere a charge is created on the assets of the company for the purposeof payment in case of default. A charge ranking PariPassu with the first charge on any assets referred to in Schedule III of the Act excluding intangible assets of the company.

The secured debentureholders have greater protection. Holders of secured debentures remainconvinced about the payment of interest and payment of principal in the event of redemption.

(b) Unsecured Debentures:These debentures are also known as naked debentures. These debenturesare not secured by way of charge on the company’s assets. Interest rate payable on unsecureddebentures is generally higher than that which is payable on secured debentures.

Tenure

- Redeemable Debentures: Redeemable debentures are those which are payable on the expiry of the specific period (Maximum period 10 years from the date of issue) either in lump sum or in Installments during the life time of the company. Debentures can be redeemed either at par or at premium.

- Irredeemable Debentures: Irredeemable debentures are also known as Perpetual Debentures because the company does not give any undertaking for the repayment of money borrowed by issuing such debentures. These debentures are repayable on the winding-up of acompany or on the expiry of a long period.

- Debentures may be for fixed terms or payable on demand:

- Debentures may be for fixed term of years or repayable on notice. [Wiley v Stocks (1909) 26 TLR 41]

- They can legally be framed as payable to bearer [Edlstein v Schubrelo (1902) 2 KB 144]

Convertible:

These debentures are issued by a company on the basis of option provided to them for conversion of debenture in the equity shares of the company after a certain period. It may be classified in the following categories:—

a. Convertible Debenture:These debentures are converted into equity shares of the company on the expiry of a specified period.

b. Non- Convertible Debenture:Partly convertible debentures are divided into two portions, viz., convertible and non-convertible portion. The convertible portion is converted into equity shares of the company at the expiry of specified period. The non-convertible portion is redeemed at the expiry of the specified period in terms of the issue.

c. Partly Convertible Debenture:Non-convertible debentures do not have any option to convert the same into equity shares and are redeemed at the expiry of specified period(s).

Basis of negotiability

Debentures issued by a company may be negotiable or non-negotiable. There are following two types of debentures:—

Bearer Debentures.-These debentures are payable to bearer of the debentures and transferable by mere delivery. These debentures are also known as unregistered debentures.

Registered Debentures- These debentures are not transferable by mere delivery of debenture certificates and shall be transferred as per the provisions of the Companies Act, by executing transfer deeds and the transfer registered by the company. Registered debentures are not negotiable instruments. A registered holder of a debenture means a person whose name appears both in the debenture certificate and in the register of debentureholders. Principal and interest amount, when due in respect of these debentures are payable to the registered holders thereof only.

Let’s Discuss Provision of Issue of Debentures:

- Which type of debentures is allowed to issue by Companies under Companies act, 2013?

i. Any amount raised by the issue of debentures SECURED BY

• a first charge or

• a charge ranking PariPassu with the first charge on any assets referred to in Schedule III of the Act excluding intangible assets of the company OR

ii. Debentures COMPULSORILY convertible into shares of the company within five years:

According to the above mentioned statement it’s clear that Company can issue two types of Debentures:

i. Debentures secured by charge on any assets referred to in Schedule III of the Act.

ii. Debentures COMPULSORILY convertible into shares of the company within five years.

There is an exemption as per Deposit Rules, company issue debentures on conditions other than mentioned above to Directors, Relative of Directors, Companies and Foreigners.

- Whetherdebenture is part of Share Capital?

Debentures are not part of share capital, it is a loan capital and company is liable to pay interestthereon whether there are profits or not.

- Debentures with voting right:

As per 71(2) Company can’t issue debentures carrying voting rights. Therefore, Debentures holders don’t have any voting rights.

- Provisions regarding Issue of Secured Debenture?

If Company is issuing secured debentures T & C for issuance of such debentures are given in Rule 18of the Companies (Share Capital and Debentures) Rules, 2014.

- Debentures are normally secured by a charge on the undertaking of the company and all its property, present and future.

- Debentures can be secured by mortgage of immovable property or hypothecation or pledge of movable property, they constitute actionable claims.

- Charge can’t be creating on the intangible assets of the Company.

- Whether secured debentures can be issue as floating charge?

In case of issue of secured debentures charge can’t be floating charge, Charge will be only fixed charge. Because act says that, any amount raised by the issue of debentures secured by a charge ranking PariPassu with the first charge on any assets referred to in Schedule III of the Act.

Floating charge will be on stock or receivable of the Company. Stock or receivables are not the part of Assets under schedule III. Therefore, charge can’t be create as floating charge in case of issue of secured debentures.

- Debentures may be issued and kept with the company’s bankers as collateral security in respect ofloans obtained from banks. [Samuel v Jarrah Timber Corporation (1904) AC 330].

- Period of Redemption of Debenture:

- The date of itsredemption shall not exceed 10 (ten) years from the date of issue.

- The following classes of companies may issue secured debentures for a period exceeding 10 (ten) years but not exceeding 30 (thirty) year

i. Companies engaged in setting up of infrastructure projects;

ii. ‘Infrastructure Finance Companies’ as defined in clause (viia) of sub-direction (1) of direction 2 of Non-Banking Financial (Non-deposit accepting or holding) Companies Prudential Norms (Reserve Bank) Directions, 2007;

iii. Infrastructure Debt Fund Non-Banking Financial companies’ as defined in clause of (b) direction 3 of Infrastructure Debt Fund Non-Banking FinancialCompanies (Reserve Bank) Directions, 2011.]

- Debenture Warrant:

A company may issue the convertible debentures, whether fully convertible or partly convertible withdetachable warrant. The warrant gives a right to the holder to get equity shares mentioned in the warrant after the expiry of a certain period at a price not exceeding the price fixed in the warrant

- Debenture at Discount:

As per section 54 of the Companies Act, 2013 there is restriction on the Companies for the issue of shares at a discount. But there is no prohibition on issue of Debentures on discount.

- Interest on Debenture:

- As stated in section 71(8) a company shall pay interest and redeem the debentures in accordance with the terms and conditions of their issue.

- Interest rate in respect of debentures is freely determinable by the issuer company.

- The interest may be paid quarterly, half-yearly or on any other terms of its issue.

- Zero Rates of Interest Debentures: Company can issue this type of debenture, Rate of interest in these debentures will be zero.

- Debenture Redemption Reserve:

- As stated in section 71(4) the company shall create a debenture redemption reserve account out of the profits of the company available for payment of dividend.

- The amount credited to such account shall not be utilised by the company except for the redemption of debentures.

- In case of partly convertible debentures, Debenture Redemption Reserve shall be created in respect of non-convertible portion of debenture issue in accordance with this sub-rule.

Rule 18(7) of the Companies (Share Capital and Debentures) Rules, 2014 provides that the company shall create a Debenture Redemption Reserve for the purpose of redemption of debentures, in accordance with the conditions given below:

- It shall be created out of the profits of the company available for payment of dividend

- No need of creation of DRR:No need of creation of DRR for debenture issued by

- All India Financial Institutions (AIFIs) regulated by Reserve Bank of India.

- Banking Companies.

- Financial Institutions(FIs) within the meaning of clause (72) of section 2 of the Companies Act,2013.

- [3]NBFCs registered with RBI.

- Percentage of contribution in DRR:

- For other companies including manufacturing and infrastructure companies, the adequacy of DRR will be 25% of the value of debentures

<in case of issued through public issue as per present SEBI (Issue and Listing of Debt Securities), Regulations 2008 and

<in the case of privately placed debentures by listed companies

- For unlisted companies issuing debentures on private placement basis, the DRR will be 25% of thevalue of debentures.

- Partly Convertible Debenture: in case of partly convertible debentures, Debenture Redemption Reserveshall be created in respect of non-convertible portion of debenture

- Method of investment in DRR:Every company shall invest or deposit, as the case may be

- Date of Deposit:on or before the 30th day of April in each year,

- Amount of Deposit: At least 15% (fifteen percent), of the amount of its debentures maturing during the year ending on the 31st day of March of the next year,

- In any one or more of the following methods, namely:-

i. in deposits with any scheduled bank, free from any charge or lien

ii. in unencumbered securities of the Central Government or of any StateGovernment

iii. in unencumbered securities mentioned in sub-clauses (a) to (d) and (ee) of section 20 of the Indian Trusts Act, 1882

iv. in unencumbered bonds issued by any other company which isnotified under sub-clause (f) of section 20 of the Indian Trusts Act, 1882

- Use of the earning form the above investments:the amount invested or deposited as above shall not be used for any purpose other than for redemption of debentures maturing during the year referred above.

- Debenture Trust Deed:-

- Rule 18(5) of the Companies (Share Capital and Debentures) Rules, 2014 state that – A trust deed in Form No. SH-12 or as near thereto as possible shall be executed by the Company issuing debentures in favour of the debenture trustees 68.

- The Trust deed shall be executed within three months of closure of the issue or offer.

- Open for Inspection: A trust deed for securing any issue of debentures shall be open for inspection to any member or debenture holder of the company, in the same manner, to the same extent and on the payment of the same fees, as if it were the register of members of the company

- Copy of Deed: A copy of the trust deed shall be forwarded to any member or debenture holder of the company, at his request, within seven days of the making thereof, on payment of fee.

- Debenture Trust Deed Contain: The debenture trust deed shall, inter alia, contain the following:

- Description of Debenture Issue

- Details of Charge Created (in case of Secured Debentures)

- Particulars of the Appointment of Debenture Trustee(s)

- Events of Default

- Obligations of Company

- Miscellaneous

[1](g) resolutions passed in pursuance of sub-section (3) of section 179;

[2] Not required to file in case of Private Limited Company.

[3]For NBFCs registered with the RBI under Section 45-IA of the RBI (Amendment) Act, 1997, [and for Housing Finance Companies registered with the National Housing Bank] ‘the adequacy’ of DRR will be 25% of the value of debentures issued through public issue as per present SEBI (Issue and Listing of Debt Securities) Regulations, 2008, and no DRR is required in the case of privately placed debentures.

(Author – CS Divesh Goyal, ACS is a Company Secretary in Practice from Delhi and can be contacted at csdiveshgoyal@gmail.com)

(Author – CS Divesh Goyal, ACS is a Company Secretary in Practice from Delhi and can be contacted at csdiveshgoyal@gmail.com)

Read Other Articles Written by CS Divesh Goyal

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. The observations of the author are personal view and the authors do not take responsibility of the same and this cannot be quoted before any authority without the written consent of the author.

Author Bio

Can Debentures attached with Detachable Warrants Forfeited by defaults of non payment of Calls If any? At the same time Detachable warrants has no meaning as the Market Value of Shares fallen below the Issue Price of Warrants conversion? What remedy is possible under Companies Act 1956?

Hi,

Lets say a company issues a convertible debentures worth 1Crs, expiry 1 year. So in this case can a convertible debenture convert in to equity share at the end of 1 year if the company Doest pay the Rs 1 cr amount. Does the companies act restrict the convertible debentures to be exercised in 1, 2, 3 Years or it does it say it can’t be exercised before certain year.

Will appreciate you answer.

Hello & Good Afternoon sir,

Can you just tell me maximum term for which unsecured debentures can be issued, as Rule. 18 states the term of 10 years (with some exceptional cases) for secured debentures.

Where it is mentioned that Company can issue Zero Rates of Interest Debentures?

WE ARE UNLISTED ,LTD, COMPANY HAD ISSUED DEBENTURES TO UTI 5.00CR IN 1998 WITH REDEMPTION UPTO 7YEARS 2+5 EXPIRING 2005 DUES STILL NOT PAID UTI SOLD TO PHOENIX @ 3.00CR 2014 PHOENIX HAS CLAIMED 96CR ON 6NOV18 IN NCLT WHAT IS RIGHT VALUATION PHOENIX CAN CLAIM