CS S. Dhanapal

INTRODUCTION

INTRODUCTION

Corporate Social Responsibility (CSR) has been in existence for a long time and is almost as old as civilization. It is based on the Gandhian Principle of “trusteeship concept” whereby business houses are looked upon as trustees of the resources they draw from society and thus are expected to return them back manifold. CSR is extremely important for sustainable development of all stakeholders (all the people, on whom the business has an impact, including the society at large). Proponents of CSR argue that companies make more long term profits by operating with a perspective, while critics argue that CSR distracts from the economic role of businesses. Nevertheless, the importance of CSR cannot be undermined.

Section 135 of the Companies Act, 2013 contains provisions exclusively dealing with Corporate Social Responsibility. Schedule VII contains a list of the activities which a company can undertake as part of its CSR in initiatives.

PROVISIONS OF COMPANIES ACT, 2013 ON CSR (READ WITH NOTIFIED RULES)

♦ Meaning of CSR

“Corporate Social Responsibility (CSR)” means and includes but is not limited to

(i) Projects or programs relating to activities specified in Schedule VII to the Act; or

(ii) Projects or programs relating to activities undertaken by the board of directors of a company (Board) in pursuance of recommendations of the CSR Committee of the Board as per declared CSR Policy of the company subject to the condition that such policy will cover subjects enumerated in Schedule VII of the Act.

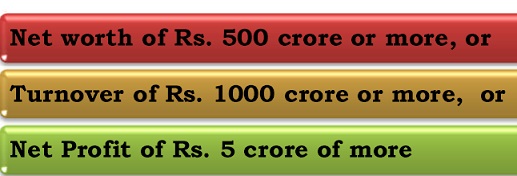

♦Applicability

- Every company including its holding or subsidiary and a foreign company having branch or project office in India which fulfills the criteria given below:

- CSR rules shall be applicable commencing from financial year 2014-15 onwards. i.e. from 01.04.2014.

- Every company which ceases to be covered by the above criteria for 3 consecutive financial years shall not be required to comply with the CSR provisions till such time it again falls within the limits.

♦ CSR Committee

- CSR Committee should consist of atleast 3 directors out of which atleast 1 director should be independent director.

Explanations:

(i) an unlisted public company or a private company covered under subsection (1) of section 135 which is not required to appoint an independent director pursuant to sub-section (4) of section 149 of the Act, shall have its CSR Committee without such director.

(ii) a private company having only two directors on its Board shall constitute its CSR Committee with two such directors;

(iii) with respect to a foreign company covered under CSR rules, the CSR Committee shall comprise of at least two persons of which one person shall be as specified under clause (d) of sub-section (1) of section 380 of the Act and another person shall be nominated by the foreign company.

- Board’s Report to disclose composition of CSR Committee.

- Functions of CSR Committee:

v Formulate and recommend to the Board, a Corporate Social Responsibility Policy which shall indicate the activities to be undertaken by the company as specified in Schedule VII of the Act.

v Recommend the amount of expenditure to be incurred on the activities referred to in clause (a); and

v Monitor the Corporate Social Responsibility Policy of the company from time to time.

v Prepare a transparent monitoring mechanism for ensuring implementation of the projects / programmes / activities proposed to be undertaken by the company.

♦ Responsibility of the Board of Directors

- To ensure that atleast 2% of average net profit of 3 immediately preceding years is spent on CSR activities every year.

“Net profit” means the net profit of a company as per its financial statement prepared in accordance with the applicable provisions of the Act, but shall not include the following, namely:

i) any profit arising from any overseas branch or branches of the company, whether operated as a separate company or otherwise; and

ii) any dividend received from other companies in India, which are covered under and complying with provisions of Section 135 of the Act

- Average net profit shall be calculated in accordance with provision of Section 198.

- To approve the CSR Policy after considering recommendations of CSR Committee.

- To disclose CSR policy and initiatives in Board’s report and Company’s website.

- To ensure that activities reflected in CSR policy are actually undertaken by company.

- To ensure that activities included by a company in its Corporate Social Responsibility Policy are related to the activities included in Schedule VII of the Act.

- The Board’s Report of a company covered under these rules pertaining to a financial year commencing on or after the 1st day of April, 2014 shall include an annual report on CSR containing particulars specified in Annexure to the CSR Rules.

- If the company does not spend 2% of net profits as required, then Board to report the reasons in the Board’s report.

♦ CSR Policy & expenditure

- ‘CSR Policy” relates to the activities to be undertaken by the company as specified in Schedule VII to the Act and the expenditure thereon, excluding activities undertaken in pursuance of normal course of business of a company. The CSR Policy of the company shall, inter-alia, include the following, namely :-

– a list of CSR projects or programs which a company plans to undertake falling within the purview of the Schedule VII of the Act, specifying modalities of execution of such project or programs and

– monitoring process of such projects or programs:

- The CSR Policy of the company shall specify that the surplus arising out of the CSR projects or programs or activities shall not form part of the business profit of a company.

- CSR expenditure shall include all expenditure including contribution to corpus, or on projects or programs relating to CSR activities approved by the Board on the recommendation of its CSR Committee, but does not include any expenditure on an item not in conformity or not in line with activities which fall within the purview of Schedule VII of the Act.

♦ Other points relating to CSR

- The Board of a company may decide to undertake its CSR activities approved by the CSR Committee, through a registered trust or a registered society or a company established by the company or its holding or subsidiary or associate company under section 8 of the Act or otherwise, provided that –

(i) if such trust, society or company is not established by the company or its holding or subsidiary or associate company, it shall have an established track record of three years in undertaking similar programs or projects;

(ii) the company has specified the project or programs to be undertaken through these entities, the modalities of utilization of funds on such projects and programs and the monitoring and reporting mechanism.

- A company may also collaborate with other companies for undertaking projects or programs or CSR activities in such a manner that the CSR Committees of respective companies are in a position to report separately on such projects or programs in accordance with these rules.

- Only such CSR activities will be taken into consideration as are undertaken within India.

- Only activities which are not exclusively for the benefit of employees of the company and their family members shall be considered as CSR activity.

- Company shall give preference to the local area and areas around it where it operates, for spending the amount earmarked for Corporate Social Responsibility activities.

- Companies may build CSR capacities of their own personnel as well as those of their Implementing agencies through Institutions with established track records of at least three financial years but such expenditure shall not exceed 5% of total CSR expenditure of the company in one financial year.

- Contribution of any amount directly or indirectly to any political party under section 182 of the Act, shall not be considered as CSR activity.

- In case of a foreign company, the balance sheet filed under sub-clause (b) of sub-section (1) of section 381 shall contain an Annexure regarding report on CSR.

♦ Activities which may be included by companies in their Corporate Social Responsibility Policies ( Amended Schedule VII)

(i) Eradicating hunger and poverty and malnutrition, promoting preventive healthcare and sanitation and making available safe drinking water;

(ii) Promoting education including special education and employment enhancing vocational skills especially among children, women, elderly, and the differently abled and livelihood enhancement projects;

(iii) Promoting gender equality, empowering women, setting up homes and hostels for women and orphans, setting up old age homes, day care centres and such other facilities for senior citizens and measures for reducing inequalities faced by socially and economically backward groups.

(iv) Ensuring environmental sustainability, ecological balance, protection of flora and fauna, animal welfare, agro forestry, conservation of natural resources and maintaining quality of soil, air and water;

(v) Protection of natural heritage, art and culture including restoration of buildings and sites of historical importance and works of art, setting up public libraries, promotion and development of traditional arts and handicrafts

(vi) Measures for the benefits of armed forces veterans, war widows and their dependents

(vii) Training to promote rural sports, nationally recognised sports, paraolympic sports and Olympic sports;

(viii) Contribution to the Prime Minister’s National Relief Fund or any other fund set up by the Central Government for socio-economic development and relief and welfare of the Scheduled Castes, the Scheduled Tribes, other backward classes, minorities and women; and

(ix) Contributions or funds provided to technology incubators located within academic institutions which are approved by the Central Government.

(x) Rural development projects

(Written by S.Dhanapal, Senior Partner, S Dhanapal & Associates, A firm of Practising Company Secretaries, Chennai.)

how to register under CSR , and what are the keys for registered

whether gaushala is covered under CSR

Why only preventive healthcare is included in CSR? Why not healthcare of patients too? Or did I not understand it correctly?

Sir,

Thanks for this. I have a question about CSR. It is about the expenditure on account of CSR incurred by Companies. ARe they allowable expenses under IT act?

Thanks

Harison

If a compnay has financial year ending 31st Dec and not 31st March , then whether it comply with CSR from year ending 31st Dec 2014 or 31st Dec 2015. Please advise

Expenses incurred on CSR activities should be exempted from tax liability of companies.