According to the Companies Act, 1956 / Companies Act, 2013, Companies are required to file certain documents every year like Financial Statements, Annual Return with the Registrar of Companies. However, in practice, there are many Companies which were not filing their yearly reports and returns due to several reasons which constitute an offence under the Act.

Such inaction by the company besides other consequence, also lead to serious impact like prosecutions and financial burden in the form of additional fees on the Company and its Directors. Section 164(2) read with section 167 of the Companies Act, 2013 [the Act], the provisions of which have commenced with effect from 01.04.2014, provide for disqualification of a director on account of default by a company in filing an annual return or a financial statement for a continuous period of 3 years.

Recently, in September, 2017, the Ministry of Corporate Affairs (MCA) identified over 3 lakh directors associated with Companies that had failed to file financial statements or annual returns in the MCA21 online registry for a continuous period of three financial years i.e. FYs 2013-14 to 2015-16. The MCA also struck-off names of many companies from the Register of Companies maintained by the Registrar pursuant to provisions of Section 248 of the Act on grounds of continuous failure to file financial statements or annual returns. Bank accounts of such “struck-off” companies were also frozen for operations.

The Director Identification Number (DIN) of the disqualified directors was deactivated to the effect that such directors are barred from accessing the online registry and a list of such directors was published on the website of MCA.

There appear number of representations were made to the Ministry of Corporate Affairs in this matter by Corporate / industry / Chamber and other bodies seeking an opportunity to complete the pending filings and normalize operations..

On 29.12.2017, vide General Circular No. 16/2017, a Condonation of Delay Scheme, 2018 (CODS-2018/Scheme) has been introduced by MCA with a view to giving an opportunity to the defaulting companies to rectify the default and complete all their pending annual filings with the MCA.

| HIGHLIGHTS OF CONDONATION OF DELAY SCHEME, 2018 |

| Limited time opportunity has been given for defaulting companies to complete their pending annual filings. |

| Scheme is available only for 3 months, starting from 01.01.2018 and ending on 31.03.2018. |

| Scheme is applicable only to “active defaulting companies”. |

| DIN of Directors associated with “active defaulting companies” will be temporarily activated to facilitate the overdue filings.

As per update available on MCA website as on 04.01.2018, the process for ‘reactivating’ the DINs in system in respect of disqualified Directors is in progress and status may be checked by 12th January, 2018. |

| Scheme is not applicable for thoseDirectors who may have been associated with a company which was struck off under Section 248(1) of the Companies Act-2013 and such DINs shall be activated only upon receipt of orders for revival of the said company as per due process laid down under Section 252 of the Companies Act, 2013. |

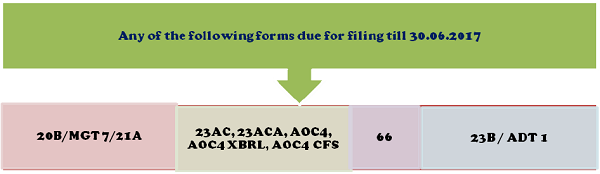

| Only forms relating to annual filing such as Form AOC 4, Form 20B and other annual filing forms can be filed under this scheme. |

| Only forms such as AOC 4, 20B and other annual filing forms, due for filing till 30.06.2017 can be filed under this scheme. |

| After filing of all pending annual filings, e-form CODS has to be filed by each defaulting company with filing fees of Rs. 30,000/-. |

| The Registrar concerned shall withdraw the prosecution(s) pending if any before the concerned Court(s) for all documents filed under the scheme. |

| While filing form CODS, company has to make a declaration that the company has withdrawn the appeal(s)/writ(s) pending before any Court or NCLT/NCLAT or Regional Director or any other adjudicating authority. |

| This scheme is without prejudice to action under section 167(2) of the Act or civil and criminal

liabilities, if any, of such disqualified directors during the period they remained disqualified. |

| At the conclusion of the Scheme, if the directors are still found to be disqualified (pending forms or e-form CODS 2018 not filed / not approved), their DIN shall be liable to be deactivated again. |

| At the conclusion of the Scheme, the Registrar shall take all necessary actions under the Companies Act, 1956 / 2013 against the companies who have not availed themselves of this Scheme and continue to be in default in filing the overdue documents. |

| The e-Form CODS 2018 would be available from 20.02.2018 or an alternate date,which will be intimated by the ministry on MCA website. |

IMPLEMENTATION OF CODS-2018

Q.1 WHICH COMPANIES CAN AVAIL THIS SCHEME?

Companies (other than companies whose name has been struck-off from the Register of Companies) which have not filed financial statements or annual returns under the Companies Act, 1956 or Companies Act, 2013 for a continuous period of 3 years. These Companies are referred as “DEFAULTING COMPANIES” under the Scheme.

Q.2 FROM WHEN TO WHEN IS THE SCHEME APPLICABLE?

| Starting date | Ending date |

| 01.01.2018 | 31.03.2018 |

Q. 3 WHAT DOCUMENTS CAN BE FILED UNDER THIS SCHEME?

Q. 4 WHAT ACTION IS TO BE TAKEN AFTER COMPLETING ALL PENDING FILINGS?

Once all the pending forms are filed, e-form CODS needs to be filed with filing fees of Rs. 30,000/-.

E-Form CODS will be available for filing by February, 2018 or other date to be intmated by MCA.

Q. 5 WHAT IS THE OBJECT OF THIS SCHEME?

This is an one time opportunity given to active defaulting companies, whose directors have been disqualified and their DIN blocked, to complete their pending annual filings.

During the operation of the Scheme, the DINs of such directors will be temporarily activated to facilitate the pending annual filings.

Q. 6 WHAT ACTION CAN BE TAKEN AGAINST COMPANIES WHO DO NOT AVAIL THIS SCHEME?

If the pending filings are not completed or if the form CODS-2018 is not filed / approved by MCA – On conclusion of Scheme, DIN of Directors associated with such companies will be deactivated again!

At the conclusion of the Scheme, the Registrar shall take all necessary actions under the Companies Act, 1956 / 2013 against the companies who have not availed themselves of this Scheme and continue to be in default in filing the overdue documents.

PROCEDURE TO BE FOLLOWED BY “DEFAULTING COMPANIES” FOR FILING PENDING DOCUMENTS UNDER CODS-2018

| STEP 1 | Ensure that the company is active on the MCA portal for e-filing |

| STEP 2 | Check the status of DIN of all the directors associated with the Company as on date of filing. Only if the DIN is active, e-filing can be undertaken. Ensure DSC of director, authorized to e-file the forms,is registered on the MCA platform. |

| STEP 3 | Keep all the pending requisite documents ready for filing, duly signed and scanned. |

| STEP 4 | Prepare and file all the necessary pending e-forms on the MCA portal, as permitted under the Scheme, digitally signed and duly certified as required, along with payment of filing fees and additional fees as per Section 403 of the Act read with the Rules as applicable on date of filing. |

| STEP 5 | Withdraw the appeal(s)/writ(s), if any pending, before any Court or NCLT/NCLAT or Regional Director or any other adjudicating authority. |

| STEP 6 | Prepare and file form e-CODS 2018, digitally signed, with filing fees of Rs. 30,000/-supported by necessary attachments. |

| STEP 7 | Maintain a copy of the all the documents and forms filed under the Scheme with their challans and ensure that all forms including e-CODS 2018 has been approved by the ROC. |

PROCEDURE TO BE FOLLOWED BY “STRUCK-OFF COMPANIES”

A. PROVISIONS RELATING TO RESTORATION OF NAME OF COMPANY

B. PROCEDURE FOR MAKING APPLICATION TO NCLT FOR RESTORATION OF NAME OF COMPANY STRUCK-OFF U/S 248

STEP 1 – DRAFTING AND FILING OF PETITION TO NCLT

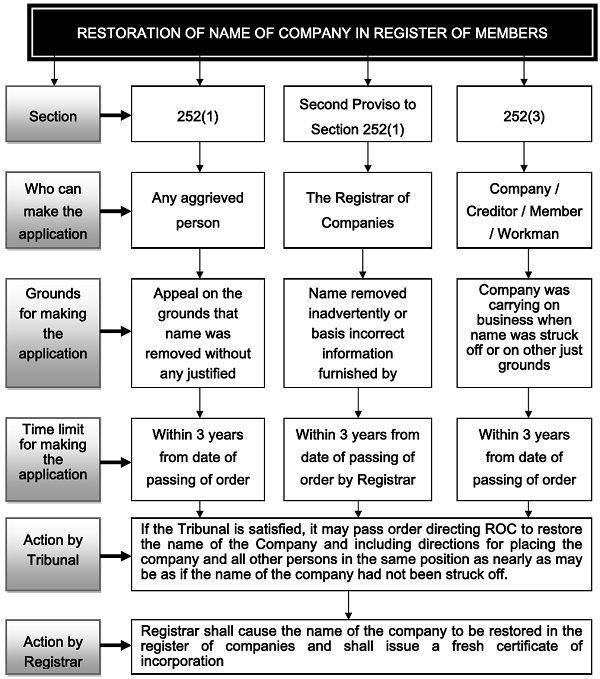

An appeal under sub-section (1) or an application under sub-section (3) of section 252, may be filed before the Tribunal in Form No. NCLT. 9, with such modifications as may be necessary and such application shall be accompanied by following documents as mentioned below:

- Document and / or other evidence in support of the statement made in the petition, as are reasonably open to the petitioner(s);

- Documentary evidence in proof of the eligibility and status of the petitioner(s) with the voting power held by each of them, wherever applicable;

- Where the petition is presented on behalf of members, the letter of consent given by them, if applicable;

- Statement of particulars showing names, address, number of shares held, and whether all calls and other monies due on shares have been paid in respect of members who have given consent to the petition being presented on their behalf;

- Affidavit verifying the petition in form NCLT 6

- Notice of Admission in Form NCLT 2

- Memorandum of Appearance in Form NCLT 12 or Vakalatnama by authorized representatives along with Board Resolution / Power of Attorney by applicant authorising the representative, as the case may be

- Bank draft evidencing payment of application fee

- Two extra copies of the petition

- Any other relevant document.

The Application under Section 252 in Form NCLT 9 should be accompanied with fee of Rs.2000/- by Bank Draft in favour of “Pay and Accounts officer, Ministry of Corporate Affairs”, payable in the City where the Jurisdictional Bench is located.

STEP 2 – NOTICE TO REGISTRAR AND OTHER PERSONS

A copy of the appeal or application, needs to be served on the Registrar and on such other persons as the Tribunal may direct, atleast 14 days before the date fixed for hearing of the appeal or application. Copy to Registrar may be filed in form GNL-1.

STEP 3 – HEARING THE PARTIES AND PASSING OF ORDER BY TRIBUNAL

Upon hearing the appeal or the application or any adjourned hearing thereof, the Tribunal may pass appropriate order, as it deems fit.

Where the Tribunal makes an order restoring the name of a company in the register of companies, the order shall direct that-

(a) the appellant or applicant shall deliver a certified copy to the Registrar of Companies within 30 days from the date of the order;

(b) on such delivery, the Registrar of Companies do, in his official name and seal, publish the order in the Official Gazette;

(c) the appellant or applicant do pay to the Registrar of Companies his costs of, and occasioned by, the appeal or application, unless the Tribunal directs otherwise; and

(d) the company shall file pending financial statements and annual returns with the Registrar and comply with the requirements of the Companies Act, 2013 and rules made thereunder within such time as may be directed by the Tribunal.

The order may provide for such provisions as deemed just for placing the company and all other persons in the same position as nearly as may be as if the name of the company had not been struck off from the register of companies.

STEP 4 – FILING OF ORDER COPY WITH REGISTRAR (ROC)

A certified copy of the order has to be filed with ROC within 30 days in eform INC 28.

STEP 5 – RESTORATION OF NAME OF COMPANY

The Registrar shall publish the order passed by NCLT in the Official Gazette, under his official name and seal and shall cause the name of the company to be restored in the register of companies and shall issue a fresh certificate of incorporation.

FEW POINTS THAT DEMAND LITTLE MORE UNDERSTANDING

- The time period of the Scheme is quite short, especially in relation to Struck-off Companies which are required to follow the entire procedure for restoration of their name and then to complete all the pending filings and also to file form e-CODS 2018 within the given span of 3 months.

- Even though the Scheme has already become operational w.e.f 01.01.2018, the DIN of the disqualified directors is yet to be activated for e-filing. As per update posted on the MCA portal today, the MCA is in process of reactivation of DIN and status may be checked by 12.01.2018. The companies have been advised by MCA to keep all the documents ready for filing in the meantime.

- The position of a director associated both with an active defaulting company as well as a struck off company where struck off company is not revived during the Scheme period, is not clear. Whether DIN will be activated for filing pending documents of active defaulting company and whether DIN will remain active after conclusion of the Scheme if pending documents of active defaulting company are filed remains to be seen.

- Whether on filing of all pending documents and form e-CODS 2018, the disqualification will be automatically removed or further action like filing of Form DIR 10 will be required.

(Written by S.Dhanapal, Senior Partner, S Dhanapal & Associates, A firm of Practising Company Secretaries, Chennai.)