Significant Beneficial Ownership (SBO)

MCA on 15th February, 2018, came out with draft of Companies (Beneficial Interest and Significant Beneficial Interest) Rules, 2018

On June 13, 2018, MCA issued the Companies (Beneficial Interest and Significant Beneficial Interest) Rules, 2018 (‘Final Rules’) and enforced section 90 of the Amendment Act

On February 08, 2019, MCA issued the Companies (Significant Beneficial Owner) Amendment Rules, 2019. These rules shall be in force from date of Publication of Notice.

BACKGROUND:

The Provisions of SBO, in a different form, been part of the Companies Act, 1956, under section 180(7) (3). The new avatar comes under Section 90 of the Companies Act, 2013, as amended in 2017.

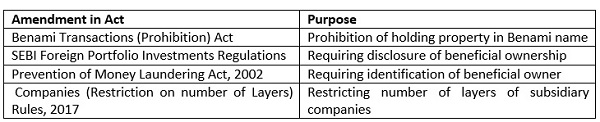

The issue of the misuse of multi-layered corporate entities has grabbed attention of various policymakers and regulators. Regulatory authorities have adopted a step-by-step approach and tried to address this issue by enacting various legislations, notable among them being:

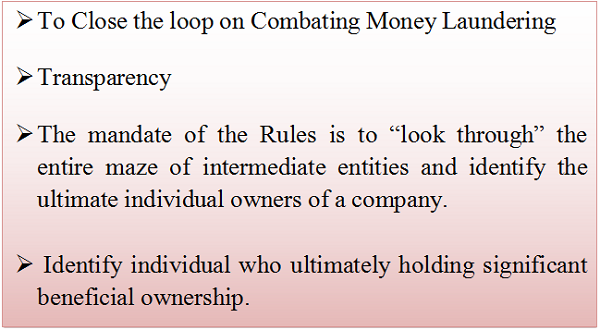

OBJECTS

Basic Terms to understand the Concept:

Registered Owner: means a person whose name is entered in the register of members of a company as the holder of shares in that company but who does not hold beneficial interest in such shares;

> In general words,this person are not an actual owner of shares.

> Only his name is entered into register of members.

> He is not entitled to dividend, officer for right issue of shares, bonus shares etc.

However, this person having

> voting rights in the Company,

> Vote on poll,

> name shall be entered in registered of member,

> entitle to sign proxy form,

> shall be count for the quorum etc.

Example:

Mr. A holds shares of XYZ Private Limited. However, Name of Mr. B entered into registered of members as registered member. In this case Mr. B is registered owner of Shares of XYZ Pvt Ltd. But the actual Owner is Mr. A.

Beneficial Owner: Every individual, who acting alone or together, or through one or more persons or trust, including a trust and persons resident outside India, holds beneficial interests, in shares of a company or the right to exercise, or the actual exercising of significant influence or control.

In general words,

> Beneficial owner is actual owner of the shares.

> Only his name is not entered in register of members.

> He is entitled to all beneficial interest as mentioned below.

Example:

Mr. A holds shares of XYZ Private Limited. However, Name of Mr. B entered into registered of members as registered member. In this case Mr. A is beneficial owner of Shares of XYZ Pvt Ltd. But the Mr. B name mentioned in Registered of Members.

Beneficial Interest: Beneficial interest in a Share includes,

> directly or indirectly,

> through any contract, arrangement or otherwise,

> the right or entitlement of a person alone or

> together with any other person to;

(i) Exercise or cause to be exercised any or all of the rights attached to such share; or

(ii)Receive or participate in any dividend or other distribution in respect of such share.

In general words, beneficial owner is entitled to exercise all the rights of the shares like: Dividend, right issue, bonus of shares etc.

Significant Beneficial Owner:

Every individual,

> who acting alone or together, or

> through one or more persons or trust,

Possesses one or more of the following rights or entitlement in such reporting Company

Hold Directly OR together with Direct Holding

I. Not Less than 10% of Shares;

II. Not less than 10% of Voting Right in the shares;

III. Has right to receive or participate in not Less Than 10% of the total distribution of Dividend, or any other distribution, in a financial year (through indirect holding or together with any direct holding)

IV. Has right to exercise, or actually exercises, significant influence or control, in any manner other than through direct holdings along.

NOTE:

EXPLANATION-1: If an individual does not hold any right or entitlement indirectly under clause (i), (ii) and (iii) as mentioned above. He shall not be considered to be a significant beneficial owner.

DIRECT HOLDING OF RIGHT AND ENTITLEMENT:

Meaning of Hold ‘Right or Entitlement Directly” an individual shall be considered to hold a right or entitlement directly in the reporting company, if he satisfies any of the following criteria, namely:-

a. The shares in reporting company representing such right or entitlement are held in the name of Individual;

b. The individual holds or acquires a beneficial interest in the share of the reporting company under section 89(2), and has made a declaration in this regard to the reporting company

INDIRECT HOLDING OF RIGHT AND ENTITLEMENT:

Meaning of Hold ‘Right or Entitlement Indirectly” an INDIVIDUAL shall be considered to hold a right or entitlement directly in the reporting company, if he satisfies any of the following criteria, in respect of a member of the reporting company, namely:

A. Body Corporate Member:

Where the member of reporting Company is a body corporate.

Note:

- Whether incorporated or registered in India Or

- Whether Incorporated or registered in abroad.

- Other than a Limited Liability Partnership and

- the Individual-

a. Hold majority stake in that Member (means such individual hold majority stake in that body corporate member); or

b. Hold majority stake in the ultimate holding Company of that Member

“Majority Stake” means;-

(i) holding more than one-half of the equity share capital in the body corporate; or

(ii) holding more than one-half of the voting rights in the body corporate; or

(iii) having the right to receive or participate in more than one-half of the distributable dividend or any other distribution by the body corporate.

B. HUF Member:

Where the member of reporting Company is a HUF and individual is Karta of the HUF

C. Partnership Entity Member:

Where the member of reporting Company is a Partnership Entity and the Individual

Note:

- Firm is member through itself or

- Firm is member through partners.

a. Is a partner; or

b. Holds majority stake in the body corporate which is a partner of the partnership entity; or

c. Holds majority stake in the ultimate holding company of the body corporate which is a partner of the partnership entity;

D. Trust Member:

Where the member of reporting Company is a Trust (through trustee) and the Individual

a. Is a trustee in case of a discretionary trust or a charitable trust;

b. Is a beneficiary in case of a specific trust;

c. Is the author or settler in case of a revocable trust.

Checks for SBO Disclosures:

1. There should be a Natural Person.

2. Individual having beneficial interest not less than 10% of shares.

3. Individual holding share indirectly or together with direct holding

4. Share capital includes (GDR+CCP’s+CCD’s)

Note: Only direct holding of shares shall not considered as SBO

Provisions of SBO applicable on all the Companies. (Here company means Reporting Company)

i. Listed Public

ii. Unlisted Public and

iii. Private

ii. The word “alone or together” includes interest of Relatives in shares also?

Computing threshold of 10%, the combined holding of the person along with the holding of such other persons (like: Body Corporate, Firm, Trust, HUF) having common interest shall also be considered.

iii. Whether a Company/ Trust/ Body Corporate/ Partnership firm can be Significant Beneficial Owner?

As per Section 90, only a Natural Person (individual) can be Significant Beneficial Owner. For the purpose of significant beneficial owner, in case of ‘person other than individuals or natural person’, shall be determined as under:

| S. No. | Where Member is | Along with | Percentage |

| A. | Body Corporate (Excluded LLP) |

|

Hold majority stake in that Member (means such individual hold majority stake in that body corporate member); or

Hold majority stake in the ultimate holding Company of that Member |

| B. | TRUST

Where the member of reporting Company is a Trust (through trustee) and the Individual |

|

|

| C. | PARTNERSHIP FIRM / LIMITED LIABILITY PARTNERSHIP FIRM | Where the member of reporting Company is a Partnership Entity and the Individual

Note:

|

|

| D. | HUF Member | Where the member of reporting Company is a HUF and individual is KARTA of the HUF | |

iv. If an individual holding interest in shares less than 10% whether SBO rules shall apply on such person

First Condition for applicability of SBO Rules and section 90 i.e. Natural person should have at least 10% of interest in ‘Shares’ indirectly or together with direct holding. (Indirect shareholding is mandatory)

Example:

Capital Structure of Company ABC limited is as following:

| Equity Share Capital of | Rs. 1,000 |

| CCD’s of | Rs. 1,500 |

| CCPS’ of | Rs. 500 |

| TOTAL | Rs. 3,000 |

Mr. A beneficially holds Rs. 260 equity shares in the Company. Whether Mr. A beneficially required giving disclosure under SBO?

Solution: In the above mentioned exampl; Mr. A holding shares as beneficially. As per

Explanation I:- Individual should hold atleast any no. shares Indirectly.

Explanation II:- A individual shall cosider holding of shares indirectly if, the individual holds or acquires a beneficial interest in the share of the reporting company.

Conclusion: Therefore, in above mentioned Example Mr. A shall not considered as Significant Beneficial Owner and no need to file any disclosure of SBO.

v. Meaning of Shares under Section 90 read with relevant rules.

As per Explanation VI of Rule 2 (h) of SBO Rules, For the purpose of calculation of 10% of beneficial interest in shares, Shares Includes…Instrument in form of

- Global Depository Receipts,

- Compulsorily Convertible Preference Shares or

- Compulsory convertible debentures.

vi. Whether SBO rules applicable on person resident outside INDIA (Non-Resident).

The definition of SBO includes non-residents as well. Therefore, the non-residents shall also be covered by the said provisions.

viii. Meaning of Direct Holding?

Meaning of Hold ‘Right or Entitlement Directly” an individual shall be considered to hold a right or entitlement directly in the reporting company, if he satisfies any of the following criteria, namely:-

c. The shares in reporting company representing such right or entitlement are held in the name of Individual;

d. The individual holds or acquires a beneficial interest in the share of the reporting company under section 89(2), and has made a declaration in this regard to the reporting company

ix. Meaning of Indirect Holding?

INDIRECT HOLDING OF RIGHT AND ENTITLEMENT:

Meaning of Hold ‘Right or Entitlement Indirectly” an INDIVIDUAL shall be considered to hold a right or entitlement directly in the reporting company, if he satisfies any of the following criteria, in respect of a member of the reporting company, namely:

A. Body Corporate Member:

Where the member of reporting Company is a body corporate.

Note:

- Whether incorporated or registered in India Or

- Whether Incorporated or registered in abroad.

- Other than a Limited Liability Partnership and

- the Individual-

c. Hold majority stake in that Member(means such individual hold majority stake in that body corporate member); or

d. Hold majority stake in the ultimate holding Company of that Member

B. HUF Member:

Where the member of reporting Company is a HUF and individual is Karta of the HUF

C. Partnership Entity Member:

Where the member of reporting Company is a Partnership Entity and the Individual

Note:

- Firm is member through itself or

- Firm is member through partners.

d. Is a partner; or

e. Holds majority stake in the body corporate which is a partner of the partnership entity; or

f. Holds majority stake in the ultimate holding company of the body corporate which is a partner of the partnership entity;

D. Trust Member:

Where the member of reporting Company is a Trust (through trustee) and the Individual

d. Is a trustee in case of a discretionary trust or a charitable trust;

e. Is a beneficiary in case of a specific trust;

f. Is the author or settler in case of a revocable trust.

HYPOTHETICAL SITUATIONS

A. If an Individual (‘a’) holding shares in any Company (Exp. Mr. A Holding 50% shareholding of ABC Pvt. Ltd. and his name entered into register of member)Whether provisions of SBO shall be applicable on Mr. A or Not?

As per meaning “Significant Beneficial Owner: means beneficial owner holding ultimate beneficial interest not less than 10% and Indirectly or together with direct holding.”

Therefore, One can opine that SBO provision applicable on person who is holding beneficial interest, indirectly or together with direct holding.

In above mentioned example individual holding shares directly in the company in his name therefore provision of SBO not applicable on such individual as per Explanation I.

B. If an Individual (‘a’) holding shares in any Company,(Exp. Mr. A Holding 5% shareholding of ABC Pvt. Ltd. and his name not entered into register of member).

On behalf of Mr. a name of Mr. B entered into register of Members. Whether provisions of SBO shall be applicable on Mr. A or Not?

Solution: In the above mentioned exampl; Mr. A holding shares as beneficially. As per

Explanation I:- Individual should hold atleast any no. shares Indirectly.

Explanation II:- A individual shall cosider holding of shares indirectly if, the individual holds or acquires a beneficial interest in the share of the reporting company.

Conclusion: Therefore, in above mentioned Example Mr. A shall not considered as Significant Beneficial Owner and no need to file any disclosure of SBO.

C. If in the question B; A Holding 18% shareholding of ABC Pvt. Ltd. And Not holding any direct shares). On behalf of Mr. a name of Mr. B entered into register of Members. Whether provisions of SBO shall be applicable on Mr. A or Not?

Solution: In the above mentioned exampl; Mr. A holding shares as beneficially. As per

Explanation I:- Individual should hold atleast any no. shares Indirectly.

Explanation II:- A individual shall cosider holding of shares indirectly if, the individual holds or acquires a beneficial interest in the share of the reporting company.

Conclusion: Therefore, in above mentioned Example Mr. A shall not considered as Significant Beneficial Owner and no need to file any disclosure of SBO.

D. What is Director Shareholding and Indirect Share holding?

- X hold 25% shares of XYZ limited in his Name.

- Y hold 99% shares of ABC Limited and ABC Limited Hold 70% shares in XYZ Limited in its name.

In the above mentioned case Mr. X hold Directly 25% shares in XYZ

And

Mr. Y holds indirectly 70% shares of XYZ Limited.

E. Mr. X hold beneficial interest in A Ltd, B Ltd, C LTD and D LTD. Should Mr. X disclose in BEN 1 to all the Companies?

Yes, Mr. X has to disclose to all the Companies.

F. Mr. X holds 80% of P Ltd, which holds 80% of Q Ltd. Can Mr. X claim that I have complied with my obligation having disclosed to P Ltd, and P Ltd should have disclosed my indirect holding to Q? Can Mr. X say that he has no idea about P’s holding of Q?

Mr. X indirectly hold 64% (i.e. 80*80%) shares in Q Limited. Therefore, The SBO should provide the declaration of its Indirect beneficial interest in all the companies. It is pertinent to note that the one who has control or significant influence cannot plead unawareness. Therefore, right upto the vertical spectrum, Mr. X will have to keep disclosing

G. Mr. A (Individual) holds 30% of P Ltd. (Reporting Company) Now, Q Ltd (Member of Reporting Company) holds 25% of P Ltd, and Mr. A hold 35% shares in Q Limited. Whether Mr. A needs to filed SBO declaration in BEN-1

As per Explanation III (i) to check for indirect holding, Individual should hold majority stake in member of reporting Company.

In the above example individual holding 35% stake of Member Company, Which is less than majority Stake.

Therefore, in above example Mr. A. shall not considered as SBO.

H. Situation

Mr. X Hold 10% share holding of PQR Limited (Reporting Company)

XYZ Limited hold 5% shareholding of PQR Limited

Mr. X Hold 60% shareholding of XYZ Limited (Member Company)

a. Whether Mr. X need to Give SBO disclosure to PQR Limited

As per Explanation III (i) to check for indirect holding, Individual should hold majority stake in member of reporting Company.

As Mr. X Hold 60% shareholding of XYZ (Majority Stake Condition Complied)

As Indirect holding of Mr. X 3% (5*60%) AND Direct Holding 10%. Therefore Total Holding (Indirect together with direct holding [3+10]) i.e. 13% Condition of Indirect together with direct holding 10% also complied.

Conclusiton: Mr. X met all the conditions to become SBO. Therefore, its need to file BEN-1 with PQR Limited.

I. COMPANY:

Ultimate Holding Company (H)

Member Subsidiary Company (S)

Reporting Company (T)

Individual Mr. A

Situation I:

Mr. A Directly holds 0% in Reporting Company (T).

Company S Hold 30% stake in Company T

Company H 60% shares in S.

Mr. A Hold 70% shares in Company H.

Solution: Whether A Need to file SBo with Company T:

Condition First: Mr. A hold Majority Stake (i.e. 70%) in ultimate Holding Company (i.e. H)

Condition Two: Member of Reporting Company (i.e. T) is Body Corporate (i.e. S)

Condition Three: Individual ultimately indirectly holding 12.6% in reporting Company (60*70%=42) (30*42%=12.6)

Conclusiton: Mr. A complied with all the condition of Explanation III (i) therefore, need to file BEN-1 SBO declaration to Reporting Company (i.e. T).

Compliance requirement –

SIGNIFICANT BENEFICIAL INTEREST

A. Compliance by Significant Beneficial Owner:

First Disclosure: Every significant beneficial owner (SBO) shall file a declaration in Form No.BEN-1 to company in which he holds the significant beneficial ownership on the date of commencement of these rules within 90 days from commencement of these rule i.e. 13th June, 2018.

Disclosure on change basis: Every SBO shall file any change in his significant beneficial ownership within 30 days to the Company. {Section 90(1) read with Rule 3 of SBO Rules}

Become Significant Beneficial Owner: Every individual, who acquires significant beneficial ownership in a Company, shall file a declaration in Form No.BEN-1to the Company within 30 days of acquiring such significant beneficial ownership.

B. Compliance by Company:

Registers: Every company shall maintain a register of the interest declared by individual’s u/s 90(1).

Return: Company shall file a return in Form No.BEN-2 with ROC within 30 days from the date of receipt of declaration in BEN-1. {Section 90(4) read with Rule 3 of SBO Rules}

Registers: The Company shall maintain a register of significant beneficial owner in Form No. BEN – 3.

Note:

Above compliances shall be done by Company after receipt of information from the Significant Beneficial Owner.

Food for thought………..

I. If Company has not received any such BEN-1 from significant beneficial Owner, then whether company have to take any actions to obtain such information?

As per provisions of Section 90(5) read with rule 6,7 of (SBN Rules, 2019),

Section 90(5) A company shall give notice, in the prescribed manner, to any person (whether or not a member of the company) whom the company knows or has reasonable cause to believe—

(a) To be a significant beneficial owner of the company;

(b) To be having knowledge of the identity of a significant beneficial owner or another person likely to have such knowledge; or

(c) To have been a significant beneficial owner of the company at any time during the three years immediately preceding the date on which the notice is issued,

and who is not registered as a significant beneficial owner with the company as required under this section.

Rule 6: Company shall give notice seeking information in Form No.BEN-4.

PROCESS:

STEP: 1 – Reply by Concerned Person:

The person to whom notice has been issue shall revert to the Company within 30 days of Notice.

STEP: 2- Action by Company

The company shall,—

(a) Where that person fails to give the company the information required by the notice within the time specified therein; or

(b) Where the information given is not satisfactory, {Section 90(7) read with Rule 7 of SBO Rules}

The Company shall apply to Tribunal within 15 days of the expiry of the period specified in Notice.

Notice for an order directing that the shares in question be subject to restrictions with regard to transfer of interest, suspension of all rights attached to the shares and such other matters as may be prescribed.

COMPLIANCE FOR PROFESSIONAL

I. Auditor/ Person who is signing MGT-7 of Company ‘S’

- Auditors’ while audit the Company have to check whether there is any body corporate is shareholder of Company ‘S’.

- If Yes, whether BEN-1 is received by the Company.

- If BEN-1 not received, whether Company sent notice to such persons.

- If Notice Sent, reply not received whether Company has taken action in Tribunal.

In case of non-compliance by the Company, auditor has to report the same in his Report.

II. Directors/ Officer in Default of Company ‘S’:

It is responsibility of the directors as officer in default to do followings:

- They shall check whether there is any beneficial owner of shares of Company.

- Whether there is any Holding Company

- Whether there is any Subsidiary, WOS, associate Company

If Company having any Holding Company has to follow process as mentioned in Section 90(5) discussed above.

If Company having Subsidiary, Associate Company they have to check whether their shareholders required to file BEN-1, If yes they will follow with them to file BEN-1 to subsidiary/ associate Company.

(Author – CS Divesh Goyal, GOYAL DIVESH & ASSOCIATES Company Secretary in Practice from Delhi and can be contacted at csdiveshgoyal@gmail.com)

Author Bio

A very informative article. Everything has been deeply explained.

Just one question:

For the purpose of calculating the shareholding percentage held by an individual in the member body corporate, whether diluted shareholding will be considered or basic shareholding ?

Thank You for sharing this informative blog.

is this applicable to a government company?

Very informative article. very well explained

very well explained

What would be the fate in case of cross holding? A Ltd. holds 40% in B Ltd. and B Ltd. holds 30% in A Ltd. Mr. X and his wife Mrs .X are holding 9% each in both the companies.

“Your article always gives much in-depth clarity on the subject matter”.

Hats off CS Divesh Goyal ji.!!

As per meaning “Significant Beneficial Owner: means beneficial owner holding ultimate beneficial interest not less than 10% and Indirectly or together with direct holding.”

as per notification its “or” not and kindly check, why SBO shall not be applicable on individual holding directly more than 10 pct of shares

Is this compliance is applicable in following case for Mr. A?

Individual Mr.A (Foreigner) have substantial Interest in LLP “B” (Foreign). “B” have substantial interest in LLP “C” (Foreign). “C” Have substantial Interest in Indian Company.

Very useful and detailed article. Professionalism to core. Great job.

if HUF is holding shares in a Company then disclosure requirement is mandatory?

LLP is not covered under the SBO rules so same is not applicable on LLP, for detail understanding lets take a example:-

LLP “S” hold 60% shares in the company “A”.

Mr. C and D both hold separately 50-50% holding in LLP “S”. As above Mr. C & D are SBO in “A” but due to non-applicability on LLP, disclosure by C & D is not required.

If i am wrong correct me.

1. Difference between Significant Benificial owner & Benificial owner viz a viz disclosures under Section 89 and 90. As both the sections states the same thing except the % of Benificial ownership. Meaning in case of a company is member position in both the case are the same. That means you have to make disclosures under both the sections. If it is so than what is the sanctity of two sections when one has to make disclosures under section 89 irrespective of % of shares held. A big question.

2. In case the above is true than in case of widely held company, there could be so many companies/body corporates who are the shareholders. In that event how to go about the disclosures.

3.Rules says 10% and Act says 25%. What should be taken as the rules cannot override the Act. Rules are only procedures and explanations to the Act.

The Rules are applicable to company.. food for thought.. whether any foreign company who is SBO could be covered under these rules?

Is there any clarity that which % shall be consider while making compliances as section 90 is not notified yet in the commencement notification ? Shall we consider these rules as commencement of section 90 of Comp. Amendment Act 2017.

Thanks for sharing this great post. It was really useful