1. The works contract (Including any transfer of property in goods in the execution of contract) related to immovable property shall be treated as supply of service. Works contract as well as sale of under construction apartment shall be subjected to GST. Currently service tax charge on 40% of project value, thus the effective service tax rate is 6%, similarly effective vat rate around 1% charge on project value in different state. In GST work contract service shall be taxable @ 18%.

2. The sale of under constructed property shall be liable to GST @ 12 %.( including value of land). Presently tax effective tax rate is 4.5% (15% of 30% value of project including land).

3. On other hand full credit of input tax is allowed comparing to current regime where input credit is not allowed, therefore it seem beneficial to real estate industries.

4. Now, question arises in mind what will be treatment of composite contract related to movable property, the concept of composite supply and mix supply has been insert in GST Bill, 2017.

5. Once it is clear that work contract will be tax in GST as service, the distinction between goods and service is relevant only for Place of supply and Point of Taxation.

6. The transaction of sale/ purchase of immovable property shall be constitutionally outside the ambit of GST and shall be liable to stamp duty and property tax under state law.

A transaction of works contract, is now, sometimes, taxed twice; firstly as sale by the State Government and secondly as service by the Central Government.

Works contracts can straddle two taxable activities as per the current law. There is of course supply of goods. Then, due to the very nature of the contract, there is supply of services.

As of now, the supply of goods is taxable in the form of Value Added Tax (VAT), while the services element is taxable as service tax.

In law, there have been differing views of the Supreme Court and the High Court’s on the applicability of this theory. The final word of the Apex court in BSNL and Others Vs. Union of India (SC 2006) was that the aspects doctrine pertains to legislative competence and not the application of taxation on the same components of a transaction.

Recently the judgment of Delhi High Court Judgment in case of Suresh Kumar Bansal Vs UOI & others in 2016 has come which struck down the levy of service tax on work contract where land is also transfer, in lack of valuation provision and Supreme court of India in case of L&T, 2017 in which it was held that that composite contract/ work contracts was not taxable prior to 01.06. 2007.

At present, State VAT laws have specific provisions for taxing works contracts. To avoid taxing the services element, these laws and associated rules provide for either separation of labor and materials or percentage deductions in transaction value. Another method is of prescription of a lower rate of tax in a composition/ lump-sum scheme for works contracts. The service tax law has also provided for similar treatment to avoid taxation of sale of goods as part of a works contract.

The overarching concept in a GST is one of supply which subsumes the concepts of sale of goods, provision of services and manufacture. In GST Model, goods as well as services will be taxed on a uniform rate. Therefore the dispute whether a transaction is subjected to VAT or Service tax comes to end.

After article 246 of the Constitution, the following article shall be inserted, namely:—

“246A. (1) Notwithstanding anything contained in articles 246 and 254, Parliament, and, subject to clause (2), the Legislature of every State, have power to make laws with respect to goods and services tax imposed by the Union or by such State.

(2) Parliament has exclusive power to make laws with respect to goods and services tax where the supply of goods, or of services, or both takes place in the course of inter-State trade or commerce.

In article 366 of the Constitution,—

(i) after clause (12), the following clause shall be inserted, namely:—

‘(12A) “goods and services tax” means any tax on supply of goods, or services or both except taxes on the supply of the alcoholic liquor for human consumption;’;

All supply of goods or services or both will attract CGST (to be levied by Centre) and SGST (to be levied by State) unless kept out of purview of GST. GST will be applicable even when the transaction involves supply of both (goods and services). In effect, woks contracts will also attract GST. As GST will be applicable on supply ‘the erstwhile taxable events such as manufacture‘, sale‘, provision of services etc. will lose their relevance.

For taxing a transaction in GST, two things are important one is supply and other is goods or service or both

Section 7

Supply includes—

(a) all forms of supply of goods and/or services such as sale, transfer, barter, exchange, license, rental, lease or disposal made or agreed to be made for a consideration by a person in the course or furtherance of business,

(b) Importation of services, for a consideration whether or not in the course or furtherance of business, and

(c) An activity specified in Schedule I, made or agreed to be made without a consideration and

(d) The activity is to be treated as a supply of goods or a supply of services as referred in schedule II.

(2) Notwithstanding anything contained in sub-section (1),

(a) activities or transactions specified in schedule III; or

(b) activities or transactions undertaken by the Central Government, a State Government or any local authority in which they are engaged as public authorities, shall be treated neither as a supply of goods nor a supply of services.

(3) Subject to sub-section (1) and sub-section (2), the Central or a State Government may, upon recommendation of the Council, specify, by notification, the transactions that are to be treated as—

(a) a supply of goods and not as a supply of services; or

(b) a supply of services and not as a supply of goods.

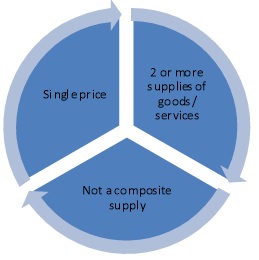

(a) a composite supply comprising two or more supplies, one of which is a principal supply, shall be treated as a supply of such principal supply;

(b) a mixed supply comprising two or more supplies shall be treated as supply of that particular supply which attracts the highest rate of tax.

Section 2(56)

“Goods” means every kind of movable property other than money and securities but includes actionable claim, growing crops, grass and things attached to or forming part of the land which are agreed to be severed before supply or under a contract of supply;

Section 2(102)

“Services’’ means anything other than goods, money and securities but Includes activity relating to use of money/ conversion by cash/ any other mode from one form, currency or denomination, to another form, currency or denomination for which a separate consideration is charged.

GST Scheme in relation to Composite contracts as follow;

Section 2(30)

“Composite supply” means a supply made by a taxable person to a recipient consisting two or more supplies of goods or services, or any combination thereof, which are naturally bundled and supplied in conjunction with each other in the ordinary course of business, one of which is a principal supply;

Section 2(90)

“Principal supply” means the supply of goods or services which constitutes the predominant element of a composite supply and to which any other supply forming part of that composite supply is ancillary.  Example: Indian Airlines provides passenger transportation service. They also supply food on board to passengers. Supply of transportation services would be the principal supply and the service as a whole would qualify as composite supply.

Example: Indian Airlines provides passenger transportation service. They also supply food on board to passengers. Supply of transportation services would be the principal supply and the service as a whole would qualify as composite supply.

Section 2(74)

“Mixed supply” means two or more individual supplies of goods or services, or any combination thereof, made in conjunction with each other by a taxable person for a single price where such supply does not constitute a composite supply

Examples: Supply of soap bars where soap boxes are given free of cost; supply of wheat for which a bottle of honey is given free of cost.

In the above example of honey being supplied with wheat, both wheat and honey will be taxed at the rate of tax applicable for honey (being commodity taxed at higher rate).

Job Work under GST– read sec 2(68) with schedule II

2(68) “job work” means any treatment or process undertaken by a person on goods belonging to another registered person and the expression “job worker” shall be construed accordingly;

Schedule II

ACTIVITIES TO BE TREATED AS SUPPLY OF GOODS OR SUPPLY OF SERVICES

3. Treatment or process

Any treatment or process which is applied to another person’s goods is a supply of services.

Note: Job work always be taxable as a service even if it is a composite contract as specified in schedule II.

The provision of declared service continue without any modification, in GST law also, for removing any ambiguity of taxation of work contract, the work contract and sale of under constructed property shall be subjected to tax as service under GST. Schedule II define the matters to be treated as supply of goods or service and Sec 2(119) defines the work contract.

Schedule II

MATTERS TO BE TREATED AS SUPPLY OF GOODS OR SERVICES

5. The following shall be treated as “supply of service”

(a)……………….

(b) Construction of a complex, building, civil structure or a part thereof, including a complex or building intended for sale to a buyer, wholly or partly, except where the entire consideration has been received after issuance of completion certificate, where required, by the competent authority or before its first occupation, whichever is earlier.

Explanation.- For the purposes of this clause-(1) the expression “competent authority” means the Government or any authority authorized to issue completion certificate under any law for the time being in force and in case of non-requirement of such certificate from such authority, from any of the following, namely:–

(i) an architect registered with the Council of Architecture constituted under the Architects Act, 1972; or

(ii) a chartered engineer registered with the Institution of Engineers (India); or

(iii) a licensed surveyor of the respective local body of the city or town or village or development or planning authority;

(2) the expression “construction” includes additions, alterations, replacements or remodeling of any existing civil structure;

6. Composite supply

The following composite supplies shall be treated as a supply of services, namely:—

(a) works contract as defined in clause (119) of section 2; and

(b) supply, by way of or as part of any service or in any other manner whatsoever, of goods, being food or any other article for human consumption or any drink (other than alcoholic liquor for human consumption), where such supply or service is for cash, deferred payment or other valuable consideration.

Schedule III

ACTIVITIES OR TRANSACTIONS WHICH SHALL BE TREATED NEITHER AS A SUPPLY OF GOODS NOR A SUPPLY OF SERVICES

5. Sale of land and, subject to clause (b) of paragraph 5 of Schedule II, sale of building.

Section 2 ((119) “works contract” means a contract for building, construction, fabrication, completion, erection, installation, fitting out, improvement, modification, repair, maintenance, renovation, alteration or commissioning of any immovable property wherein transfer of property in goods (whether as goods or in some other form) is involved in the execution of such contract;

The work contract as well as sale of under construction property shall be taxable as Supply of service, which also include the value of goods which is transfer in execution of work contract. Schedule II specifies that works contracts will be treated as supply of services and accordingly, provisions of time of supply and place of supply of services shall apply to works contract transactions.

Contract for Work Vs Contract of Sale

It shall be notable that if we constructed immovable property on its own and later on sale to other person then it is a contract for sale of immovable property and not work contract and shall be out of GST ambit, constitutionally sale and purchase of property, subject to clause (b) of para 5 of schedule II, shall be matter of state and liable to stamp duty and property tax.

Now it is very clear from the Schedule III paragraph 5, that sale of constructed property shall not be liable for GST.

Negative List of Credit;

Sec 17(4) notwithstanding anything contained in sub-section (1) of section 16 and subsection (1), (2), (3) and (4) of section 18, input tax credit shall not be available in respect of the following:

(a) …………………

(b)………………

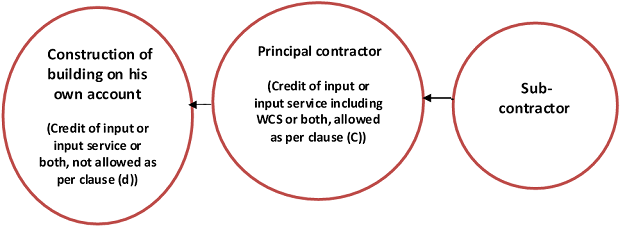

(c) Works contract services when supplied for construction of immovable property, other than plant and machinery, except where it is an input service for further supply of works contract service;

(d) goods or services received by a taxable person for construction of an immovable property on his own account, other than plant and machinery, even when used in course or furtherance of business;

Explanation 1.- For the purpose of this clause, the word “construction” includes re- construction, renovation, additions or alterations or repairs, to the extent of capitalization, to the said immovable property.

Explanation 2.- ‘Plant and Machinery’ means apparatus, equipment, machinery, pipelines, telecommunication tower fixed to earth by foundation or structural support that are used for making outward supply and includes such foundation and structural supports but excludes land, building or any other civil structures.

Note: Construction of building on his own account include the case where building has construct by builder for own purpose.i.e not intended for sale.

Note: Credit has been block at end point, this is also logical as NO GST applicable on sale of immovable property, therefore no ITC allowed.

Conclusion:

By treating work contract as service provide the complete solution of continues dispute arise in past between goods or service. Once it is clear that work contract will be tax in GST as service, the distinction between goods and service is relevant only for Place of supply and Point of Taxation.

Author Bio

hello sir, supplying and drilling of sheet pile in a bridge construction for railway project. kindly advise whether it will be triggered as composite supply under SAC 9954 with 18% or 12% tax rate.

DEAR SIR

WE ARE DOING STATUTORY TESTING OF L P G CYLINDERS FOR OIL COMPANY LIKE INDIAN OIL CORPORATION. THE WORK INCLUDES CLEANING , TESTING, PAINTING ETC…., WE ARE USING OUR OWN TRUCKS FOR TRANSPORTATION OF THE EMPTY CYLINDERS. WE ARE NOT USING ANY CONSIGNMENT NOT. OUR QUESTIONS ARE UNDER

1. WHETHER THE CONTRACT WILL COME UNDER COMPOSIT CONTRACT ?

2, WHAT IS THE S AC CODE ?

3,WHAT IS THE % OF TAX OF THE TRANSPORTATION

HOPE YOU WILL REPLAY MY QUESTIONS

THANKING YOU

BINU

सर,

पावर कार्पोरेशन मे जहां वर्क्स अनुबंध सेवाएं, जहां यह काम संविदा सेवा की और आपूर्ति के लिए इस मद पर जीएसटी कैसे चार्ज किया जाए क्या संसोधित गजट मे पावर कार्पोरेशन के संविदा सेवा भी सामिल हो सकता हैं।

[TO BE PUBLISHED IN THE GAZZETE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)] Government of India Ministry of Finance (Department of Revenue) Notification No. 20/2017-Central Tax (Rate) New Delhi, the 22nd August, 2017 G.S.R……(E).- In exercise of the powers conferred by sub-section (1) of section 9, sub-section (1) of section 11, sub-section (5) of section 15 and sub-section (1) of section 16 of the Central Goods and Services Tax Act, 2017 (12 of 2017), the Central Government, on the recommendations of the Council, and on being satisfied that it is necessary in the public interest so to do, hereby makes the following amendments in the notification of the Government of India, in the Ministry of Finance (Department of Revenue), No. 11/2017- Central Tax (Rate), dated the 28th June, 2017, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i), vide number G.S.R. 690(E), dated the 28th June, 2017, namely:-

We are golf course makers.we supply earth and other materials like pvc pipes,grass and other materials.we do earth work like leveling etc also.This is total contract of 11 crores.At what rate should we charge GST ?

We have a work order for supply & installation of electrical wiring & cabling, panel supply, earthing. Now in work order we have line item for supply of material with rate & next line item above material installation rate. In above case how to charge GST on supply & GST on installation ?

In line item of supply of material we have electrical point wiring which consist of wire, PVC pipe, switch, switch plate & GI Box. Now How to charge GST on this item. Please not that in this case GST on above material is 18% & 28%.

Can anybody reply GST rate is @18% OR principal supply i.e, Electrical Goods @28%

We have a work order for supply & installation of electrical wiring & cabling, panel supply, earthing. Now in work order we have line item for supply of material with rate & next line item above material installation rate. In above case how to charge GST on supply & GST on installation ?

In line item of supply of material we have electrical point wiring which consist of wire, PVC pipe, switch, switch plate & GI Box. Now How to charge GST on this item. Please not that in this case GST on above material is 18% & 28%.

Can Anybody reply rate of GST is 18% or Principal Supply i.e, Electrical Goods @28%

We have a work order for supply & installation of electrical wiring & cabling, panel supply, earthing. Now in work order we have line item for supply of material with rate & next line item above material installation rate. In above case how to charge GST on supply & GST on installation ?

In line item of supply of material we have electrical point wiring which consist of wire, PVC pipe, switch, switch plate & GI Box. Now How to charge GST on this item. Please not that in this case GST on above material is 18% & 28%.

my work is aluminium section doors window in new building or in renovation work ? can i migrate to work contract composite tax for manufaturare ? plz reply

I am contractor providing Composite Supply of Modular Kitchen, Door for Underconstruction Properties. Can this be regarded as “Works Contract” as per Sec 2(119) defn of CGST or “Supply of Furniture” being principle nature ? Kindly clarify. thanks

printing job work where paper supply by parties

Very very useful article for Real states

Very very useful article