Recently the MCA issued notification dated 24/07/2020 wherein a number of amendments are introduced in IndAS 103, 107, 109, 116, 7, 8, 10, 34 and 37. We will be here discussing the amendments brought in IndAS 103. It is worthy to note that the changes are in line with changes introduced by IASB in IFRS 3 in October 2018 for FY 01/01/2020 and onwards in countries following IFRS.

Whenever there is acquisition of group of activities and assets it needs to be examined whether it is “Asset Acquisition” or “Business Combination” because both are broadly distant in their accounting treatments. Before amendments, IndAS 103 gave a very general guidance in this direction through Appendix B. But now amendments in IndAS 103 have exactly ‘hit the nail on the head’. These amendments have narrowed the scope of transactions falling under IndAS 103. These changes are very much specific and to-the-point.

Page Contents

- A. Gist of Amendments in IndAS 103:

- B. Applicability of Amendment

- C. What is Business as per Ind AS 103?

- D. Definition of Output

- E. Does this mean that input and substantive processes acquired need to have Output?

- F. Concept of Market Participants in determining “Business Combination”

- G. Removing assessment whether Market Participants can replace the missing inputs or processes

- H. Optional Concentration test

- I. Newly inserted Para B12B and B12C

- J. Other Guidance

A. Gist of Amendments in IndAS 103:

1. Business must include inputs and substantive processes applied to those inputs which have ability to create output contribute to ability to create output.

2. Change in definition of “Output” – It, now, focuses on goods and services provided to customers.

3. Omission of ability to substitute the missing inputs and processes by the market participants.

4. Addition of “OPTIONAL CONCENTRATION TEST”.

5. Omission of Para B10 and insertion of Para B12A to B12D in Appendix-B.

Let’s understand these amendments one-by-one.

B. Applicability of Amendment

The amendments shall be applicable on Acquisitions on or after 01/04/2020.

C. What is Business as per Ind AS 103?

“A Business consists of inputs and substantive processes applied to those inputs that have the ability to create outputs contribute to the ability to create output”.

Why these changes – The change is clarifying that the business can exist even when not all the inputs and processes are acquired.

Example 1, a business consists of 3 sets of inputs and processes, say, IP1, IP2 and IP3 out of which IP3 is substantive for producing output. If only IP3 is acquired by another entity still it may become a Business.

D. Definition of Output

As per IndAS 103, Output means “the result of inputs and processes applied to those inputs that provide or have the ability to provide a return in the form of dividends, lower costs or other economic benefits directly to investors or other owners, members or participants goods/ services to customers, generate investment income or other income from ordinary activities”

Why these changes – It is seen that an organization acquires an asset to reduce its cost, thereby the asset has ability to lower the cost or to provide other economic benefits to entity. Does it mean that asset acquired is a Business Combination? Of course “No”. Hence, the definition is changed and now, no such criteria is there in amended definition. Moreover, the new definition focuses more on “goods or services”.

E. Does this mean that input and substantive processes acquired need to have Output?

No. E.g. a Startup is under R&D phase for a vaccine. Meanwhile, another entity acquires its inputs and substantive processes. This acquisition may be a Business Combination, subject to other conditions, even though it is not presently creating output. What needs to be verified is that “inputs and substantive processes acquired should have the ability to contribute to create output (even though not presently creating output)”.

F. Concept of Market Participants in determining “Business Combination”

In determining whether an acquisition of activities and assets is “Business Combination” or not, IndAS 103 focuses on “Market Participants approach”. It asks to assess from point of view of Market Participants rather than how those activities and assets are being used by Acquirer and Acquiree because it leads to a common treatment of transaction otherwise each Acquirer will treat the same transaction differently based on his intention of use. There is no change in this approach. So what is the Change brought in by notification? The change can be understood in next Section with the help of example.

G. Removing assessment whether Market Participants can replace the missing inputs or processes

Example 2: Suppose, an output needs IP-1, 2 and 3. (IP 3 is substantive to contribute to ability to create output). Another entity acquires IP3 only. However, output needs IP-1 and 2 also to be created.

Before amendment, the IndAS 103 prescribed that if market participants, not Acquirer or Acquiree, can substitute IP-1 and IP-2 with their own inputs and processes, then IP3 used to become “Business Combination”.

However, after amendment this condition is removed. Now, the focus is only what has been acquired. If set of activities and assets acquired is substantive which have capability to significantly contribute to create output, then it may become “Business Combination”, subject to other conditions.

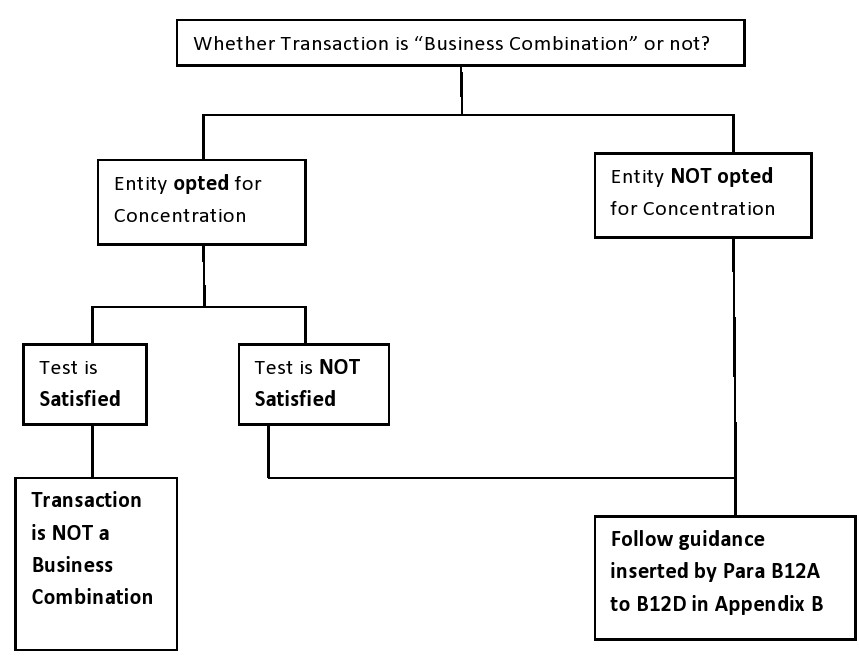

H. Optional Concentration test

(i) What is Concentration Test?It can be observed from above diagram, that the Concentration Test is optional. An entity may or may not opt for it. Further, amendments have inserted Para B12A to B12D in Appendix B of IndAS 103 and omitted Para B10.

Concentration Test is a very simple method. Simply speaking, it will be assessed whether the FMV OF GROSS ASSETS ACQUIRED is concentrated to INDIVIDUAL ASSET OR GROUP OF SIMILAR ASSET out of set of activities and assets acquired. Let’s understand this with the help of examples given in IASB documentary (slightly modified).

Example 3 : An entity acquires a legal entity which has:

| S.No. | Case A | Case B |

| 1. | Project 1 (To treat diabetes) which includes know-how, formula, protocols, designs, etc. This project 1 is at testing stage. | Project 1 (To treat diabetes) which includes know-how, formula, protocols, designs, etc. This project 1 is at testing stage. |

| 2. | Contract that provides outsourced Trials of output from Project 1 (FMV of contract is Nil) | Contract that provides outsourced Trials of output from Project 1 (FMV of contract is Nil) |

| 3. | – | Project 2 (To treat Alzheimer) which includes know-how, formula, protocols, designs, etc. This project 1 is at testing stage. |

Suppose, acquirer entity applies Concentration Test.

In Case A: Two assets are acquired. However total FMV of these assets is concentrated towards only Project 1 because Asset 2 i.e. Contract to provide outsourced trials has FMV = Nil. Hence, it can be concluded that Concentration Test is satisfied and the transaction is NOT A BUSINESS COMBINATION. It is simply an asset acquisition.

In Case B: Three assets are acquired. FMV of all the assets can be allocated to Project 1 and Project 2 (Asset 2 i.e. contract has FMV = Nil). Project 1 and Project 2 are separate identifiable intangible assets. Hence, Concentration Test is NOT met. Further guidance provided under Para B12A to B12D need to be applied to finally conclude whether this transaction is Business Combination or not.

Example 4: An entity purchases a portfolio of 10 single-family homes. The Fair value of consideration paid is equal to the aggregate of these 10 homes. It is observed that each home has a different floor area and interior design. The 10 single-family homes are located in the same area and the classes of customers (e.g. tenants) are similar. The risks associated with operating in the real estate market of the homes acquired are significantly same.

In this case, 10 homes are purchased. But these are similar assets. Hence, the Concentration Test is met even though more than 1 asset is acquired , because these assets are similar. This transaction is “Asset Acquisition” NOT BUSINESS COMBINATION.

(ii) Calculating FMV of GROSS ASSETS for Concentration Test

| Include | Exclude |

| – Goodwill calculated as per IndAS 103 other than that created on Deferred Tax liabilities acquired | – Cash and Cash equivalents acquired

– Deferred Tax Assets acquired – Goodwill related to Deferred Tax liabilities acquired |

- The FMV of Gross Assets is to be taken. It means liabilities acquired are not reduced for Concentration Test. It is because; decision of whether a transaction is asset acquisition or business combination is not effected by how the acquired activities and assets are financed.

Example 5: Entity A holds 20% interest in Entity B. It further acquired 50% interest in Entity B for Rs. 200. Entity B’s assets and liabilities on date of acquiring control:

- Building having FMV Rs. 500

- Identifiable Intangible Asset having FMV of Rs. 400

- Cash and Cash equivalents Rs. 100

- Financial liabilities having FMV of Rs. 700

- Deferred tax liabilities of Rs. 160

FMV of Non-controlling Interest is Rs. 120 and FMV of 20% stake acquired earlier is Rs. 80.

In this case, Total Goodwill in transaction can be calculated as follows:-

| Purchase Consideration for 50% stake | Rs. 200 |

| FMV of 20% stake earlier acquired | Rs. 80 |

| FMV of Non-controlling Interest | Rs. 120 |

| Total | Rs. 400 |

| Less:- Net Identifiable Asset acquired

(500 + 400 + 100 -700 – 160) |

Rs. (140) |

| Goodwill as per IndAS 103 | Rs. 260 |

In total goodwill of Rs. 260, Rs. 160 is goodwill due to Deferred Tax liabilities acquired. Now let’s apply Concentration Test.

FMV of Gross Assets acquired is = 500 (Building) + 400 (Intangible Asset) + Rs. 100 (Goodwill other than on Deferred Tax Liabilities = 260 less 160). This will come to Rs. 1000.

Rs. 1000 is not just concentrated on an individual or group of similar asset. It relates to Building and Intangible Asset which are different. Hence, concentration test is not met. Para B12A to B12D needs to be applied.

I. Newly inserted Para B12B and B12C

If acquired set of activities and assets do or do not create output then the transaction will be a business combination only when the acquired set of activities and assets include:-

- Inputs and

- Substantive processes which are CRITICAL to convert input(s) to outputs and

- Organized workforce that has necessary skills, knowledge or experience to perform that substantive process

In other words, the organized workforce is key to declare a transaction as “Business combination”, whether output is generated or not.

Exception to above: There is an exception to above enumerated point.

- Where set of activities and assets generate output, AND

- acquired substantive processes are unique/ scarce/ significant cost or effort is involved in replacing them or delay in ability to continue producing output

then there is NO requirement to assess whether organized workforce is acquired or not. It will be itself treated as “Business Combination”.

J. Other Guidance

- Para B9 suggests that a business need NOT to have liabilities.

- Para B12A suggests if the acquired set of activities and assets used to generate output which was earlier sold in market, it is considered to have generating revenue at acquisition date even if output would be integrated by the acquirer itself post-acquisition.

- Para B12D suggests that difficulties in replacing an organized workforce may indicate that the acquired organized workforce performs a process which is critical to the ability to create outputs.

We may conclude, that these amendments are going to help industry which were struggling in determining whether a transaction results in “Business Combination” or not. The Indian Accounting will become more consistent and compatible across the globe.

Bibliography: Documentary issued by the International Accounting Standards Board (IASB) in October 2018.

Author Bio

Appreciate your efforts 👍🏻👍🏻👍🏻