Understand the linkage between Sections 44AA, 44AD, 44ADA, and 44AB in the Income Tax Act. Explore the distinctions, turnover criteria, and compliance requirements for businesses and professionals. Stay informed to ensure proper compliance with tax regulations.

Section 44AA – Compulsory maintenance of Books of account

Distinction between 44AD and 44ADA

|

44AD |

V/s | 44ADA |

| Resident – Individual, HUF, Firm (excluding LLP) | Eligible Assessee | Resident – Individual and Firm (excluding LLP) |

| Any business except – Sec 44AE Business

– Agency Business – Commission and Brokerage And Turnover is upto Rs. 2 Crore |

Eligible Business | Professionals covered under section 44AA |

| Turnover x 8%

*If Turnover/Gross Receipt realized by account payee cheque/DD/Electronic payment through bank account or any electronic mode as may be prescribed upto due date of return filling then PGBP = Turnover x 6% |

Presumptive Income | Gross Receipt x 50% |

| If Assessee declares income for any PY as per sec 44AD & he doesn’t declare income as per sec 44AD in any of the 5 consecutive P.Y.’s, then he shall not be eligible to claim benefit of sec. 44AD for 5 years subsequent to the year in which assessee did not declare income as per sec 44AD. If this point is applicable & NTI of assessee is more than basic exemption then assessee is required to maintain BOA and get them audited | Linkage with 44AB | If Assessee declares income lower than 50% & his NTI is more than basic exemption he is required to maintain BOA and get it audited |

Section 44AB – Compulsory audit of Books of account

Person not opted for Section 44AD AND If opted then continuously complied with 44AD for further 5 years

Applicability of section 44AD and 44AB can be better understood with

the help of below turnover criteria

Our Comments

♦ Assessee having turnover more than Rs. 10 crore shall have to maintain BOA and get it audited on compulsory basis irrespective of condition of cash receipt and payment

♦ An Assessee opting for Section 44AD shall be exempted from maintenance of BOA related to such business as required under section 44AA and shall pay advance tax on or before 15th March of respective financial year.

Person opted for Section 44AD AND declared profit not in accordance with the provision of section 44AD in any of the 5 subsequent years

Applicability of section 44AD and 44AB can be better understood with

the help of below turnover criteria

Our Comments

♦ Where the Assessee having turnover between 1 cr and 2 cr and his net taxable income exceeds Rs. 2,50,000 and his aggregate cash receipt and payment does not exceed 5% of total payment and receipt, he shall not be liable to audit under 1st proviso to clause (a) of section 44AB but he will be liable to audit u/s 44AB(e).

♦ Where the Assessee having turnover between 2 cr and 10 cr and his aggregate cash receipt and payment does not exceed 5% of total payment and receipt, he shall be not be liable to audit under 1st proviso to clause (a) of section 44AB as well as u/s 44AB(e). Section 44AB(e) states that person shall be liable to audit to whom provision of section 44AD(4) applies and 44AD apply to the person having turnover upto 2 cr. Therefore, person having turnover more than 2 cr will not be liable to audit u/s 44AB(e).

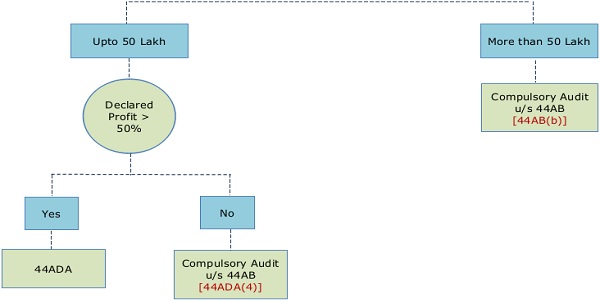

Professionals covered under section 44AA(1)

Applicability of section 44ADA and 44AB can be better understood with

the help of below turnover criteria

Our Comments

♦ Condition of cash receipt and payment upto 5% is not applicable to professionals.

♦ An Assessee opting for Section 44ADA shall be exempted from maintenance of BOA related to such business as required under section 44AA and shall pay advance tax on or before 15th March of respective financial year.

*****

Disclaimer : This material and the information contained herein prepared by us is intended to provide general information on a particular subject or subjects and is not an exhaustive treatment of such subject(s). I am not, by means of this material, providing any professional advice or services. The information is not intended to be relied upon as the sole basis for any decision which may affect you or your business. Before making any decision or taking any action that might affect your personal finances or business, you should consult a qualified professional adviser.

I shall not be responsible for any loss whatsoever sustained by any person who relies on this material.

Author Bio