The Modi Government is coming up with the various new changes in the GST Regime including the New GST Returns and the concept of E-Invoicing. Both the E-invoicing and the new GST returns have direct linked with each other. Successful of both depend on each other how they perform after there final roll out in the market and their acceptance and the Industry.

After analyzing the various GST Models of countries like Canada, UAE the Indian Government comes to a question that why India cannot also adopt the Concept of E-invoice to mitigate the Frauds relating to Input Tax Credit, Fake Invoices, etc. To mitigate all these factors and to Simplify the GST Return filing process in more user-friendly and n simple manner issues which cause a loss of revenue the need and the utility of the implementation of modified GST Return or the NEW GST Returns comes in the mind of the Government.

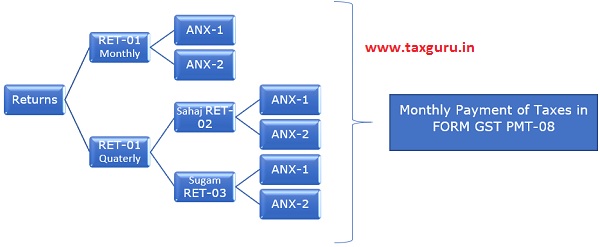

In the 31st GST Council Meet, it was decided that a New Return System under GST would be introduced for taxpayers. This return system will contain simplified return forms, for ease of filing across taxpayers registered under GST. Under this New Return System, there will be one main return GST RET-1 and 2 annexures GST ANX-1 and GST ANX-2. This return will need to be filed monthly, except for small taxpayers who can opt to file the same quarterly. Small taxpayers are taxpayers with a turnover of up to Rs 5 crore in the preceding financial year. The same can be understood easily with the help of the relevant chart as follows: –

In order to check the system quality and the Trial run of the New GST Return a pilot project has been started in October 2019 in which the taxpayers have been allowed to Manage their online Profile by using the NEW Trial Return in a Beta Mode. So that all types of Issues and Errors are corrected before the Live implementation of the NEW returns in the Industry. The Large Taxpayers whose aggregate turnover was more than Rs. 5 Crore in the preceding financial year will upload their details of Outward Supply in FORM GST ANX-1 from October 2019 onwards. However, the small Taxpayers whose turnover does not increase Rs. 5 Crore or more during the previous financial year will be allowed to upload their First Quarterly FORM GST ANX-1 only in January 2020 for the quarter ending on 31st December 2019.

For October and November 2019, large taxpayers will continue to file FORM GSTR-3B on monthly basis. They will File their first FORM GST RET-1 for December 2019 by 20th January 2020. For October and November 2019, large taxpayers will continue to file FORM GSTR-3B on monthly basis. They will File their First FORM GST RET-1 for December 2019 by 20th January 2020.

Benefits of NEW Returns Prototype: –

1. One single simplified main return form GST RET-1 containing 2 annexures GST ANX-1 and GST ANX-2 to be filed by all categories of taxpayers. No Different returns like GSTR-1,4,5,6,7 etc.

2. A mechanism for the continuous upload of revenue invoices on a real-time basis so that the Supplies and the vendor can claim the Input Tax Credit and do the following actions like Locking, Unlocking Rejections, Providing Details of Missing Invoices on Either of the Supplier Party to claim the Input Tax Credit.

3. Missing invoices and amendments, if any, can be made by filing an Amendment Return like GST RET-01A.

4. Cases where a taxpayer has applied for cancellation of registration, the taxpayer does not need to be filed the returns for this period.

5. Taxpayers considered small if turnover is up to Rs 5 crore in the preceding financial year, otherwise considered large taxpayers. Earlier the limit was 1.5 crore.

NEW GST Returns

1. FORM GST RET-01 (Normal Monthly Return): – Taxpayers whose aggregate turnover in the preceding Financial year was above Rs.5 Crore will have to file monthly return. is return needs to be filed monthly by 20th of the month succeeding the month to which the tax liability pertains. Monthly return in FORM GST RET-1 needs to be ‑led based on FORM GST ANX – 1 and FORM GST ANX – 2.

2. FORM GST RET-01 (Normal Quarterly Return): –

Taxpayers whose aggregate turnover in the preceding financial year was up to Rs.5 Crore can file this return. This return needs to be filed quarterly by 20th of the month succeeding the quarter to which the tax liability pertains. The tax must be paid monthly through FORM GST PMT-08.

3. FORM GST RET-02 (Sahaj Quarterly): –

Taxpayers whose aggregate turnover in the preceding financial year was up to Rs.5 Crore and have supplied only to consumers and unregistered persons (B2C supplies) can file this return based on FORM GST ANX – 1 and FORM GST ANX – 2 quarterly, but pay tax monthly through FORM GST PMT-08. Taxpayers opting to file Sahaj can declare outward supply under the B2C category and inward supplies attracting reverse charge only. E-commerce operators are ineligible to file Sahaj.

4. FORM GST RET-03 (Sugam Quarterly): –

Taxpayers whose aggregate turnover in the preceding financial year was up to Rs.5 Crore and have made supplies to consumers and un-registered persons (B2C) and registered persons (B2B) can file this return based on FORM GST ANX – 1 and FORM GST ANX – 2 on quarterly basis, but pay tax on monthly basis through FORM GST PMT-08. Taxpayers opting to file Sugam can declare outward supply under B2C and B2B category and inward supplies attracting reverse charge only. E-commerce operators are ineligible to file Sugam.

Availment of Input Tax Credit Mechanism under NEW GST Returns: –

1. Missing invoices: Whenever a supplier has not uploaded an invoice or a debit note, and a recipient claims ITC, it will be termed as “missing invoices”. The ITC which is availed on the missing invoices by a recipient, and these missing invoices do not get uploaded by the supplier within the time frame, then the ITC availed concerning such debit notes/invoices will be recovered from the recipient.

2. Locking of invoices: A recipient will have the option to lock in an invoice if he agrees with the details reported in that invoice. If there is a huge volume of invoices, it may not be practical to lock in individual invoices, and in such cases, deemed locking of invoices will be done on those invoices uploaded which are neither rejected nor have been kept as pending by recipient. Once it is locked then the vendor can’t amend such details only after the unlocking by the buyer party. He will be allowed to make any kind of changes in the GST Returns.

3. Unlocking of the invoices: An invoice on which ITC has already been availed by a recipient will be considered a locked invoice and will not be open for amendments. In case an amendment needs to be made to an invoice, the supplier will have to issue a debit or a credit note. An incorrectly locked invoice can be unlocked by the recipient online, subject to a reversal of ITC claim made, and an online confirmation thereafter.

4. Rejected invoices: When the recipient’s GSTIN is filled incorrectly by the supplier, the invoice will be visible for a taxpayer who is not the receiver of such supplies. As ITC will not be eligible to be taken on these invoices, the recipient will need to reject these invoices. To make the task of rejecting invoices hassle-free, the matching IT tool will have the option to create a recipient/seller master list via which the correct GSTIN can be identified.

Availing of ITC will depend on uploading of invoices or debit notes by the supplier, within the stipulated time frame. An invoice uploaded by the supplier within the 10th of the following month will be visible continuously for the recipient. The taxes payable thereafter which can be claimed as ITC will be posted in the ITC table of the recipient’s return before the 11th of the following month. These invoices will be available for availing ITC in the return which is filed by the recipient. Invoices that are uploaded by the supplier after the 10th of the following month will get posted in the concerned field of the recipient’s return of the subsequent month, however, the viewing facility will be continuous.

Author Bio

I want hindi version so please provide me.