With recent amendment to IBBI regulations for voluntary liquidation dated 31.1.2024, the process for voluntary liquidation has become more transparent, efficient and faster. These amendments have also brought some additional safeguards to protect interest of stakeholders. Now, it is mandatory to hold contributories meeting, if the voluntary liquidation is not completed within the specified period of 90 or 270 days as the case may be. This article provides an in-depth overview of the process, including its background, conditions, and steps involved. From reasons for voluntary liquidation to the detailed process timeline, this guide offers valuable insights for stakeholders navigating the voluntary liquidation process.

Background

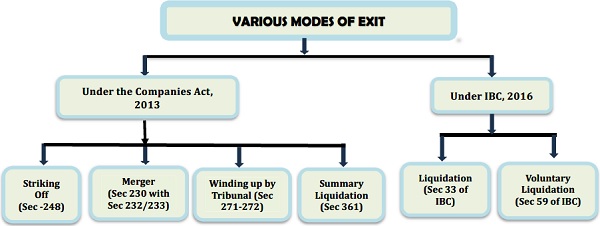

Companies are incorporated as per the provisions of Companies Act, 2013. A Company after incorporation will become an artificial person. The termination of its existence will conclude with dissolution as per the provisions of Insolvency and Bankruptcy Code, 2016 (IBC). Various ways of termination of its existence (dissolution) are as follows:

I. Striking off – FTE (Fast Track Exit) U/S 248 of Companies Act, 2013

Company’s name can be struck off pursuant to section 248(1) by the Registrar of Companies or the Company can apply voluntarily for strike-off under section 248(2) of the Companies Act,

2013 when it has not carried out its business operations for a period two years or more.

II. Merger or Amalgamation under section 230-232/233

Transferor Company gets dissolved when it merges with transferee company pursuant to section 230-232 or section 233 of the Companies Act, 2013.

III. Winding-up by Tribunal – Section 271-272

Section 271 of the Companies Act provides for winding up of a company when members passes special resolution; on application by Registrar for non-filing of financials for 5 consecutive years; Tribunal on just and equitable grounds. The winding under this section requires order of Tribunal.

IV. Summary Liquidation under Section 361

Pursuant to Section 361 of the Companies Act, 2013, Regional Director may order for winding up of a Company under summary procedure

i. When a Company has assets of book value not exceeding one crore rupees; and

ii. belongs to such class or classes of companies as may be prescribed.

V. Liquidation of a Company under Section 33 of IBC, 2016

When a Company fails to get a Resolution Plan under CIRP (Corporate Insolvency Resolution Process) or does not comply with the terms of approved Resolution Plan or for certain other reasons, Tribunal may order for dissolution of the Company.

VI. Voluntary Liquidation pursuant to section 59(7) of IBC, 2016 – Solvent Company

Voluntary liquidation is a process of winding up voluntarily without the court/NCLT intervention. Members of the Company and creditors, if any, will appoint a liquidator to liquidate all assets and pay to all its creditors. Surplus amount, if any, after meeting all costs and expenses shall be distributed to the members as per the mechanism provided in Section 53 of IBC, 2016. Voluntary liquidation process has to be completed as per Insolvency and Bankruptcy Board of India (Voluntary Liquidation Process) Regulations, 2017. Only a solvent Company is eligible for voluntary liquidation.

Voluntary liquidation of LLP’s and other Body corporates are also covered under these regulations and hence the same procedure is applicable with suitable changes.

However, voluntary liquidation of financial service providers is regulated separately and procedure specified in IBBI (Voluntary Liquidation Process) Regulations, 2017 are not applicable to such companies.

Voluntary liquidation pursuant to Section 59(7) of IBC, 2016

Introduction: As per Section 59(7) of IBC, a Company which intends to liquidate itself voluntarily and has not committed any default may initiate voluntary liquidation process subject to fulfilment of certain conditions.

A. Reasons for voluntary liquidation are as follows:

a. Special purpose Vehicle (SPV): A company can be liquidated voluntarily when the object for which the Company has been incorporated is fulfilled. For example, creation of a special purpose vehicle (SPV) in real estate projects, or toll projects etc., formed with sole purpose.

b. No potential opportunities (Unfeasible operations or poor operating conditions): If any Company does not have potential business opportunities or it is not feasible to run its operations economically due to technical obsolescence or due to un-favorable environment conditions or due to change in legal framework, it may decide to wind-up its operations voluntarily.

c. As tax planning measure: Companies may also plan for voluntary liquidation to avail certain tax benefits. Further, companies can plan for voluntary liquidation to offset its capital losses. Ex. If a holding company has capital gain on sale of its shares in one transaction, then it may plan for liquidation of loss making subsidiary(ies) or associate companies to book capital losses which can be set off against capital gains thereby holding company can save capital gain tax.

B. Conditions for Voluntary Liquidation:

a) Company must be solvent.

b) Company must have resolved to wind up voluntarily through a special resolution passed by its shareholders and creditors, if any.

C. Process of Voluntary Liquidation:

1) Solvency Declaration: The Board of directors must file a Declaration of Solvency (DoS) in the form of an affidavit stating that:

a. They have made a full inquiry into affairs of the Company and they have formed an opinion that either the Company has no debt or that it will be able to pay its debts in full from the proceeds of assets to be sold in the liquidation;

b. The company is not being liquidated to defraud any person; and

c. The company has made sufficient provision to meet the obligations arising on account of pending matters. #

The declaration must be accompanied with:

i. audited financial statements and record of business operations of the company for latest previous two years or for the period since its incorporation, whichever is later;

ii. a report on valuation of assets of the company, if any. (Valuation report is not required, if the Company has only cash and cash equivalents)

Within four weeks of such declaration under sub-clause (a), shareholders must pass special resolution approving winding up of the Company and appoint an Insolvency Professional (IP) to act as liquidator to complete the process.

If a Company has any debt, creditors representing two-thirds in value of the debt must confirm the resolution passed for voluntary winding-up within seven days of such resolution.

2) Intimation to ROC and IBBI: The Company shall intimate to ROC and IBBI about the commencement of voluntary liquidation within seven days of approval of resolution by shareholders or creditors as the case may be. The declaration of solvency shall be filed with the Registrar of Companies in Form GNL-2.

Effect of liquidation: The company shall from the liquidation commencement date cease to carry on its business. However, the company shall continue to exist until it is dissolved.

3) Liquidator to take over the Management control: Liquidator shall take over the Management control of the company and proceed with liquidation process. He is responsible for management of affairs of the Company from the liquidation commencement date and to ensure timely legal compliances.

4) Public Announcement: Within five days of his appointment, the liquidator must cause public announcement in Form A requesting claims from the stakeholders. Claims must be filed within 30 days and publication is to be made in English and regional language newspaper having wide circulation in the area where the company’s registered office is located and if the Company has website, the copy of publication also to be uploaded on its website.

5) Submission and verification of claims: Creditors either financial or operational including employees are required to submit their claims in the prescribed form attaching proof of claim. The liquidator shall verify the claims within thirty days from the last date for receipt of claims and may either admit or reject the claim, in whole or in part.

If the liquidator rejects the claim, then the creditor may file an appeal before Adjudicating Authority within 14 days.

6) Preliminary Report: The liquidator shall submit a preliminary report to the Company within 45 days from liquidation commencement date and preliminary report to include capital structure, estimate of its assets and liabilities and other relevant information.

7) Separate Bank Account: The liquidator must open a separate bank account in the company’s name, with the words ‘in voluntary liquidation’ to receive all money owed. All transactions above Rs 5000 must be made by way of cheque or through internet banking channel.

8) NOC from Tax Authorities: The liquidator shall inform to assessing officer about the commencement of liquidation. If the claims are not received or no NOC is received from the tax authorities, it is presumed that they do not have any outstanding claims.

9) Assets Realization: The liquidator shall liquidate all assets and realize the money on timely basis in order to maximize the stakeholders’ value. The money realized is required to be deposited in a separate bank account opened for this purpose.

10) Distribution: Before distribution of money to stakeholders, the liquidation cost must be paid in full and balance amount shall be distributed to stakeholders as per mechanism provided under Section 53 of IBC. The distribution must be made within 30 days from the date of receipt. If a particular asset cannot be realized due to its nature or other conditions, the liquidator may distribute such assets to its stakeholders with due approval.

11) Preservation of records: The liquidator shall maintain records and registers as per the formats prescribed in Schedule II of the Voluntary Liquidation Regulations. In case the books of accounts are not complete as on the liquidation commencement date, then the liquidator shall have them completed and brought-up-to date. The records shall be preserved:

a) electronic copy of all records for a minimum period of 8 years; and

b) physical copy of records for a minimum period of 3 years;

12) Completion of liquidation: The liquidator shall endeavour to complete the liquidation process and submit the Final Report

a) Within 90 days – if the Company does not have creditors.

b) Within 270 days – if the Company has creditors.

If the liquidation process does not complete within stipulated period mentioned above, (i.e. 90 days or 270 days as the case may be), the liquidator shall hold a meeting of the contributories within fifteen days from the end of stipulated period and submit status report. Thereafter, the liquidator shall conduct contributors meeting at the end of every succeeding two hundred and seventy days or ninety days, as the case may be, till submission of application for dissolution. The status report shall contain:

Settlement of the list of stakeholders; details of any assets that remain unsold; distribution to the stakeholders; distribution of unsold assets to the stakeholders; developments in any material litigation, by or against the company; filing of and developments in applications for the avoidance of transactions.

13) Corporate Voluntary Liquidation Account: Unclaimed dividends and undistributed proceeds, if any, shall be deposited into ‘Corporate Voluntary Liquidation Account’ and shall intimate ROC and IBBI attaching a statement in Form-G with names and last known addresses of the stakeholders entitled to receive the unclaimed dividends or undistributed proceeds.

14) Final Report: After the liquidation process is concluded, the liquidator shall prepare and file Final Report containing the following information:

a. Audited statement of accounts;

b. A declaration stating that all assets have been sold, all debts have been paid off, and no legal action is underway;

c. A statement of an asset sale that shows the assets realized value, cost, manner and mode of sale, any shortfall, and to whom it is sold.

Liquidator shall file the final report with the registrar and the IBBI, and also submit copy to NCLT attaching compliance certificate in form H.

15) Petition to NCLT for dissolution order: The liquidator shall make an petition to NCLT seeking dissolution order. After receiving the order from the hon’ble NCLT, the liquidator shall file form INC 28 with ROC. With approval of form INC 28, the company gets dissolved and master data with ROC will show Company status as “Dissolved under section 59(8).”

D. Income tax implications for voluntary liquidation: The following are compliances under Income Tax, 1961:

(i) Section 2 (22) (c) – Dividend

(ii) Section 46 – Capital Gains

(iii)Section 178 – Company in Liquidation

Section 2 (22) (c) – Dividend: Any distribution made to the shareholders of a company on its liquidation, to the extent to which the distribution is attributable to accumulated profits of the company is treated as deemed dividend and accordingly TDS @ 10% is required to be deducted (As per section 194 of Income Tax Act,1961).

Section 46 – Capital Gain: Distribution of assets of the company to its shareholders on its liquidation shall not be regarded as a transfer by the company.

Any money or other assets received by a shareholder from company during liquidation shall be chargeable to income-tax under the head “Capital gains”, as reduced by deemed dividend u/s 2(22) (c).

Section 178 – Company in Liquidation: The liquidator of a Company shall give intimation to income tax officer within 30 days from the date of his appointment. If the liquidator fails to give such intimation, he shall be personally liable for payment of income tax dues and other compliances.

However, obtaining NOC is not mandatory as per circular issued by IBBI Circular No. IBBI/LIQ/45/2021 Dated 15-11-2021.

Liquidator occupies the position of principal officer as per section 2(35) of Income Tax Act, 1961 for ensuring required compliances.

Stamp duty impact: If a company distributes immovable property to its shareholders, then liquidator is required to execute sale deed and the transaction attracts stamp duty as per respective state stamp act.

COMPLETE PROCESS TIMELINE FOR VOLUNTARY LIQUIDATION

It is important to note that while voluntary liquidation may seem straightforward but legal complexities and procedural nuances can arise. Companies considering this option should seek legal counsel to ensure compliance with all regulatory requirements and to navigate potential challenges.

Note: # Effective from 31.1.2024.

References: IBC and regulations and IBBI newsletters.

Author Bio

Thanks for Mr. Krishnan V.C

Excellent article. Lucid and clear