I. Introduction

According to the Global Infrastructure Outlook Report 2017, investment in the infrastructure industry throughout the globe is estimated to reach over $94 trillion between the years 2016 and 2040.[1] Of this total investment, almost 50 percent of it comes from only four countries: China, the United States of America, India, and Japan. According to the aforementioned trend, if infrastructure expenditure keeps growing at the current rate, there would be a $14 trillion investment shortfall by 2040.

A well-developed infrastructure system is what propels the overall growth of any nation. The amount spent on infrastructure in India between 2013 and 2017 was around INR 57 lakh crores, which, when converted to current currency, comes to INR 36 lakh crores, or 5.8% of the country’s GDP. India spent around INR 10.2 lakh crores and INR 10 lakh crores on infrastructure in the fiscal years 2018 and 2019, respectively.[2] To reach its target of a $5 trillion economy by 2030, India alone would need to invest nearly $4.5 trillion in infrastructure, as this industry has a multiplier effect on the economy as a whole. Focus should be placed on accelerating infrastructure sector growth so that it can reach 7–8% growth in the future.[3]

Private sector investment in infrastructure started to decrease towards the conclusion of the Twelfth five-year plan as a result of difficulties with land acquisition, delays brought on by permissions, challenges with utility relocation, a lack of a dispute resolution procedure, and competitive private sector bidding. Government was unable to provide the funding required to finance infrastructure because of budgetary restrictions, which delayed the start of these projects. In light of this, the government has suggested investing INR 111 lakh crores in infrastructure between the fiscal years 2020 and 2025 under the National Infrastructure Pipeline (NIP) plan. About 70% of the total money that has been allotted is anticipated to come from the federal and state governments, with the remaining 30% coming from the private sector.

Additionally, SEBI approved the implementation of Infrastructure Investment Trust (InvIT) Regulations in India in 2014 after taking into account the necessity for increased capital requirements in financing infrastructure projects. InvIT’s debut has been viewed as a bold endeavour with strong expectations that it can play a significant part in helping India achieve its critical infrastructure needs.

- II. Need for InvITs in India

- III. Legal and Regulatory Framework surrounding InvITs

- Investment by InvITs

- Investment Restrictions

- Valuation of Assets

- IV. Reception of InvITs in India

- V. Parties involved in InvITs and their Eligibility Criteria in law

- A. Sponsor

- B. Trustee

- C. Investment Manager:

- D. Project Director

- VI. Tax Structure and Leverage Restrictions of InviITs

- Leverage Restrictions on InvITs

- VII. Advantages and Risks Involved in InvITs

- Advantages for the holder of the unit:

- Additional advantages for the investors:

- Potential hazards associated with investing in InvITs

- VIII. Conclusion and the way ahead

II. Need for InvITs in India

Any economy’s foundation is its infrastructure, which is vertically interconnected with other industries like iron and steel, cement, goods, etc. According to a recent estimate, India would need to invest more than US$ 1.5 trillion over the next ten years to close its infrastructure gap. However, the sector’s growth has slowed over the previous five to seven years, particularly following the global slump. Infrastructure projects are innately expensive and take a long time to complete. The sponsors’ equity and debt have become immobilised as a result of the economic slump, particularly in the infrastructure and real estate industries. This has created a vicious cycle where the sponsor’s promoters are unable to generate their equity part to start new projects and are unable to pay their debt (which the banks might have used to lend more money to). Additionally, as a result of this, banks’ asset quality has declined, and they are currently hesitant to provide additional loans in this area. Thus, a substitute for bank funding or refinancing is required. InvITs can potentially replace bank financing while also assisting sponsors in releasing equity.

As their ownership will not be concentrated in a small number of hands and will be properly managed by the Investment manager and the project manager chosen by the Trustee, InvITs can help the system achieve greater levels of governance. In addition to the aforementioned, InvITs can be a good vehicle to attract outside capital to the Indian infrastructure industry.

III. Legal and Regulatory Framework surrounding InvITs

InviTs must be registered with SEBI and follow the SEBI (Infrastructure Investment Trusts) Regulations of 2014.[4] In the Finance Act of 2014, the government included taxation rules for InvITs referred to as “Business Trusts” under the Income Tax Act of 1961. Since then, SEBI has made a number of changes to the rules in an effort to draw in prospective investors. In a notice issued in 2017, SEBI approved financing to SPVs in whom the corresponding InvlTs had invested, extended the term of “strategic investor,” and allowed InvlTs to raise capital 4 through the issuance of debt instruments. Additionally, SEBI announced revisions that permit an increase in the leverage limits for InvlTs in its decision from April 22, 2019.[5] The previously 49% maximum leverage has been raised to 70%. To improve market liquidity and fundraising flexibility, the trading lot value was also decreased from Rs. 5,00,000 to Rs. 1,00,000.[6] In order to make fundraising easier, SEBI recently made certain changes to these regulations. With consideration for the conditions brought about by the ongoing pandemic, SEBI “granted certain relaxations for raising equity capital” by listed InviTs in its circular dated September 28, 2020][7]. According to the information provided, InvlTs are permitted to obtain equity capital through institutional placement as long as there is a two-week buffer between each transaction. It is important to remember that the prior time gap was six months, as was required. Since the same pricing method must be used for all allocations resulting from the approval of the same unit holders, changes regarding the pricing of units for preferential issues have also been made, which include a lock-in period of 3 years in the case of units allocated on a preferential basis.[8] The circular further said that the units owned by the sponsors and locked-in for three years before under the IVT Regulations must be included when calculating the lock-in requirement. To increase the number of investors, the minimum subscription amount for a publicly traded InvlT was reduced from Rs. 10 lakh to Rs. 1 lakh.[9]

Investment by InvITs

Investment Trust is to allocate at least 80% of the value to finished, income-producing infrastructure projects, and no more than 10% to those that are still under construction. InvIT units that invest more than 10% on ongoing construction projects are positioned privately since doing so would provide them more investment freedom. Institutional investors and business organisations frequently join privately placed InvIT.

InvITs have two investment options: direct and indirect (via SPV, such as a holding company). Investment trusts maintain a controlling interest as well as a minimum 50% ownership stake or interest in SPVs. SPVs are only permitted to take part in activities that are related to the underlying projects. To prevent cross-holdings, an InvIT is not permitted to invest in other InvITs. A maximum of 20% of the entire amount of InvITs may invest directly in the development of current infrastructure projects, and if this is done through an SPV, a maximum of 10% of the total amount of InvITs may do so.

In India, infrastructure projects may be directly held using invITs. However, a Hold Co/SPV will make investment in the PPP Project necessary. A Hold Co investments are susceptible to the following: (A) There should be a minimum 26% InvIT stake in SPVs. Others (b) The adherence to InvIT requirements by an InvIT, Hold Co/SPV should not be restricted by partners or shareholders. In order to assure investor liquidity, SEBI mandates the listing of new InvIT units within three years of the date of registration. Its SEBI registration would be cancelled if this is not done.

Investment Restrictions

An InvIT may finance infrastructure projects directly or via SPVs. Infrastructure investment in PPP projects must be done through special purpose companies (SPVs). They are permitted to invest in both completed, financially successful projects as well as those that are still being built, according InvIT regulations. Publicly listed InvITs are expected to invest at least 80% of their assets in finished, revenue-generating infrastructure projects.[10] Privately put InvITs are exempt from this requirement. They are allowed to put up to 10% of the value of their assets into projects that are still under construction. An InvIT must follow the private placement process if it intends to invest more than 10% of its capital. A unit of one InvIT cannot be purchased by another InvIT.

Valuation of Assets

It is recommended that an annual comprehensive assessment of all assets, including a thorough examination of all infrastructure projects, be conducted. In the case of public InvITs, this valuation should be performed twice a year. Moreover, a valuation is necessary before the issuance of any additional units (excluding Bonus units) in relation to the InvIT. In the context of InvIT asset transactions, it is mandatory to conduct a thorough valuation of the respective project by an independent valuer. The transaction amount for acquisition is limited to 110 percent, whereas for sale, it is restricted to 90 percent of the assessed value.

IV. Reception of InvITs in India

There are now 5 functioning InviTs with SEBI registrations, with a combined market value of Rs. 60,000 crores.[11] The present investment restriction of 5% restricts participation, according to Harsh Shah, CEO of IndiGrid, an InvlT linked to inter-state electricity transmission assets in India.[12] Investment in InviTs carries a minimal risk, according to IndiGrid, IRB Invit, and Indinfravit.

Since its offering, IndiGrid has paid out a total of Rs. 525 crore to its unitholders. In addition, a number of private sector companies, including Reliance Infrastructure, ACME, and ReNew Power, plan to introduce own InvlTs in the construction, telecom, and other industries. A proposal by the NHAI to set its own InvlT, which permits it to impose a toll on specific designated roadways, was also accepted by the Cabinet in December 2019.[13] This would help the NHAI earn money to build roads around the country. According to the Indian Trust Act, 1882 and the associated SEBI rules, it shall be created as a Trust. It is important to note that these roadways would be included in the central government’s main highway expansion programme, the Bharatmala Pariyojana, which was introduced in October 2017.

With a total expenditure of Rs. 5,35,000 crore, this programme sought to construct 24,800 km of roads.[14] Therefore, one of the most practical possibilities for NHAI to acquire money is to monetize its operating assets and to draw in investors from the private sector.

Fund houses increased their investment in InvITs by 55 percent between January and December 2019, going from INR 611 crore to INR 948 crore. India still has a long way to go when it comes to taking into account its need for real estate/infrastructure finance and growth potential, notwithstanding recent rises in investor interest in InvIT and REIT investments.

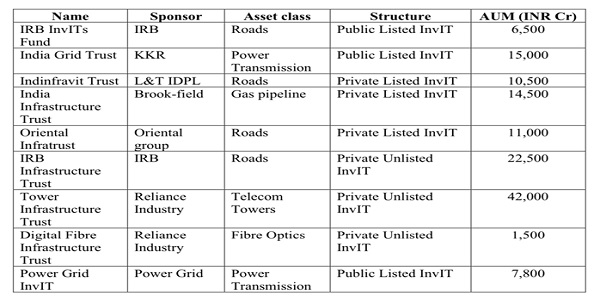

Over the previous 4-5 years, India has experienced quite a few InvIT transactions. The total assets under management (AUM) of the 8 operational InvITs is estimated to be over INR.1.4 lakh crore. Toll roads (INR. 47,500 crore) account for the majority of the assets, followed by telecom (INR. 42,000 crore), gas pipeline (INR. 16,500 crore), and electricity transmission (INR. 14,000 crore). As on date, following InvITs are prevalent in India market.[15] The details of which are listed in the table at the end of this section.

Since the passage of InvIT law, the bulk of InvITs have been sponsored by private sector infrastructure developers. The Canadian Pension Plan Investment Board and the Ontario Teachers’ Pension Plan Board, along with a variety of Domestic Institutional Investors (DIIs), invested units totaling more than INR 5,000 crore in the InvIT portfolio, which at the moment consists of five National Highways, after the National Highway Authority of India (NHAI) recently launched its first infrastructure investment trust.

V. Parties involved in InvITs and their Eligibility Criteria in law

A. Sponsor

Any company, LLP, or other legal entity that creates an InvIT and is responsible for transferring or promising to transfer the InvIT’s initial portfolio of assets as well as the formation transactions related to the creation of an InvIT. It refers to an infrastructure developer or a particular SPV in the context of PPP projects.

Eligibility requirements

There can be no more than three sponsors, and each one must have at least INR 100 crore in net worth (in the case of a business or body corporate) or INR 100 crore in net tangible assets (in the case of a limited liability company). If the sponsor is a developer, the sponsor or its associate must have at least five years of demonstrated expertise in infrastructure development or infrastructure fund management, as well as the successful completion of at least two of the sponsor’s projects.

Important Responsibilities

The Sponsor(s) shall jointly retain not less than 25% of the outstanding units of the InvIT on a post-issue basis for a period of not less than three years following the listing of the Units.[16] Any ownership share owned by the sponsor over the aforementioned 25% must be kept for at least a year following the listing of such units. In the case of PPP, the sponsor may choose to keep the PPP at the SPV level if doing so is not forbidden by any regulations. However, on a post-issue basis, aggregate ownership at the SPV level and in the InvIT should not be lower than 25% of all of the InvIT’s units for a minimum of three years from the date the units were listed.

B. Trustee

This person keeps the assets of the InvIT in the name of the InvITs for the benefit of the unit holders and also verifies that the work done by the InvITs, Investment Manager, and Project Manager complies with SEBI regulations.

Eligibility requirements

According to the Securities and Exchange Board of India (Debenture Trustees) Regulations, 1993, the trustee must be registered with the Board and cannot be connected to the management or sponsor.

Important Responsibilities

The Trustee is in charge of overseeing the assets and portfolios of the InvITs. It ensures that investment choices are in line with underlying assets. Additionally, it is in charge of appointing an investment manager and executing an investment management agreement on the InvIT’s behalf. Additionally, it receives a quarterly compliance statement and monitors the behaviour of the project manager and investors. The trustee looks at transactions between the investment management and its partners and makes sure the manager complies with all reporting and disclosure requirements.

C. Investment Manager:

An organisation, limited liability partnership, or other type of legal organisation that oversees the administration of InvIT’s investments and assets. Investment Manager performs the duties of InvIT in accordance with the rules.

Eligibility requirements

A corporation or business with a net worth of at least 10 crore Indian rupees serves as the investment manager. The investment manager’s net tangible assets must be valued at least INR 10 crore if it is a limited liability partnership (LLP).[17] The body must have at least 50% of the directors (in the case of a corporation) or members of the governing board (in the case of an LLP) who are not also the directors or members of the governing board of another InvIT, as well as at least 5 years of experience in infrastructure fund management or consulting services (exemptions are still being considered). The investment manager has committed to collaborate with the trustee on investment management (which describes the investment manager’s obligations) and maintains an office in India where the InvIT’s activities are managed.It must have a minimum of two workers with five years of work experience in infrastructure development or fund advising, as well as a minimum of one employee with five years’ expertise in a field related to invIT investment.

Key Responsibilities

Regarding the underlying assets or projects of the InvIT, including any new investments or asset divestitures, the investment manager takes investment choices. The body is in charge of keeping an eye on the project manager’s activities connected to project income streams and requesting a project manager quarterly compliance certificate. Additionally, it will be in charge of all operations connected to the unit issuance and listing of the InvIT. The investment manager must declare dividends to unitholders in accordance with the law and complete other obligations outlined in the Trustee-Investment Manager Agreement.

D. Project Director

Depending on what is required by the project agreement (which, in the case of a PPP project, could include a concession agreement), the project manager may be directly responsible for the operation and management of InvIT assets, including maintenance arrangements.

Eligibility requirements

The project’s execution is the responsibility of whoever the InvIT chooses as the project manager. In PPP projects, the organisation is in charge of project execution and milestone accomplishment in accordance with the concession agreement.

Important Responsibilities

The administration of the underlying assets falls within the purview of the project manager. It guarantees appropriate implementation and keeps track of the project’s development. The project manager must complete all requirements connected to the timely completion of infrastructure projects (where appropriate), as well as those related to their implementation, operation, maintenance, and management.

Hold Co. is an LLP or business in which InvIT wants to hold at least a 51% capital/interest portion of equity holding. It is only permitted to conduct operations related to owning underlying SPVs and infrastructure projects.[18]

An SPV (Special Purpose Vehicle) is a corporation or LLP in which an InvIT or Hold Co. owns or proposes to possess at least a 51% controlling position in the equity (however this is not taken into account for PPP Projects). An SPV’s assets should not be utilised for other operations to the tune of 90% of its holdings.

VI. Tax Structure and Leverage Restrictions of InviITs

The tax structure pertaining to dividend distribution has undergone a change, whereby the Dividend Distribution Tax (DDT) is no longer applicable to distributions made by Special Purpose Vehicles (SPVs) to Infrastructure Investment Trusts (InvIT). This change came into effect on June 01, 2016. In order to be eligible for this exemption, it is necessary for the Infrastructure Investment Trust (InvIT) to possess the complete share capital of the Special Purpose Vehicle (SPV), except for the portion that is required to be owned by other entities. The SPV’s payment of interest to the Trust on loans and advances, if applicable, is exempt from taxation and does not necessitate any deduction of TDS. The deferral of capital gains for the Sponsor resulting from the exchange of its SPV shares for InvIT units will result in taxation only upon the sale of said units. Regarding the distribution of income by InvIT, encompassing Interest, Dividends, and Capital Gains, it is noteworthy that solely the interest portion of the income obtained by the trust for unit holders will be subjected to taxation, whereas the remaining amount will be granted an exemption.[19]

The sale of listed InvIT units will incur capital gains that are subject to the security transaction tax for unit holders, which is comparable to the tax levied on listed equity shares. Long-term capital gains (LTCG) are not subject to taxation, whereas short-term capital gains (STCG) are taxed at a rate of 15%. In the case of off-exchange sales of units, the applicable rates of LTCG and STCG are imposed. The applicability of Minimum Alternate Tax (MAT) will extend to the interest income and capital gains derived from the sale of units of Infrastructure Investment Trusts (InvITs). Non-resident or offshore investors are subject to a tax rate of 5%. Incentives may be provided under the Double Tax Avoidance Agreement (DTAA), if applicable.The tax exemption for Long-term capital gains (LTCG) is applicable when the units are held for a period exceeding 36 months. Conversely, Short-term capital gains (STCG) are taxable at a rate of 15% when the units are held for a period less than 36 months

Leverage Restrictions on InvITs

The aggregate net consolidated borrowing and deferred payments of InvIT, Hold Co, and SPV(s) are restricted to 70% of the total value of assets managed by the InvIT. Provisions are established for consolidated borrowings and deferred payments that exceed 25% of the value of the InvIT’s assets.

a. The minimum required credit rating.

b. Approval by unit holders requires a greater number of affirmative votes than negative votes.

c. If there is a breach in the parameters due to price movement in the underlying assets/securities, a six-month adjustment period is permitted for the aforementioned parameters.

VII. Advantages and Risks Involved in InvITs

The InvIT structure offers several advantages, particularly to the sponsor. One such benefit is the ability to monetize real estate and infrastructure assets that generate income. By targeting the appropriate cohort of long-term investors, specifically pension funds, it presents a reduced cost of capital. The sponsor is entitled to certain tax benefits, such as exemption from dividend payment tax and relaxation of capital gains tax, and serves as a consistent source of capital for the sector upon being listed.[20]

Advantages for the holder of the unit:

Investment in real estate or infrastructure can be made without direct ownership of the asset. Infrastructure Investment Trusts (InvITs) provide tax-efficient returns to their unit holders. As the revenue generated by a project increases, there is a corresponding increase in cash flow. Additionally, the addition of new projects can enhance returns.

Additional advantages for the investors:

a. The diversification of a portfolio aids in mitigating the volatility and risk of fluctuations in portfolio value over a given duration.

b. By investing in publicly traded InvIT, investors can diversify their portfolio while circumventing the liquidity risk that is typically associated with direct infrastructure investment.

Investors who are interested in obtaining regular revenue may consider investing in InvIT, as it offers distributions on a consistent basis. The InvIT serves as a hedge against inflation as its revenue is generated from the underlying asset, which remains unaffected by inflation. The sector is characterised by a high degree of transparency owing to its robust regulatory framework and stringent control mechanisms. This is reflected in the transparent corporate structure of the sector. It is common for companies to be obligated to distribute a significant portion of their funds to shareholders, resulting in limited retained earnings for the operators.

Potential hazards associated with investing in InvITs

The premature conclusion of the concession period for the asset, coupled with the introduction of fresh projects for a duration of six months, may result in the removal of InvIT from the listing. The decrease in revenue can be attributed to the decline in traffic as well as the loss of traffic due to leakage. In addition, there exist various types of risks such as regulatory risk, default risk, and force majeure. During the initial public offering (IPO) process, there exists a potential hazard of overestimating the value of the company.

The bid-ask spread is elevated due to the limited liquidity of the InvIT unit in Indian stock exchanges, thereby exposing investors to the possibility of order execution risk. A prolonged project duration is positively correlated with an increased likelihood of project deviation in relation to actual cash flow. Therefore, effective management plays a crucial role in enhancing the performance of InvITs and increasing the value and returns for unit holders.

VIII. Conclusion and the way ahead

The clearance granted by the SEBI to GMR and IRB group to establish their own InvIT represents a significant step forward in the expansion of the InvIT sector in India. In spite of this, there are a few problems that need to be fixed by the government and the regulatory bodies in order to make the InvIT market vibrant.

1. Taxation: Obtaining clarification on the taxes issue was the single most essential stage in the process of developing InvITs in India. To take things a step further, we believe that in order to encourage more involvement, international investors should be excluded from the withholding tax. Given the track record of success that infrastructure bonds have had in the past, regular investors need to be eligible for tax breaks as well.

2. Modification to the Ownership of Assets: In order to comply with the regulations of the InvIT, the sponsor is required to either transfer or commit to transferring the whole ownership of the infrastructure assets to the InvIT. Nevertheless, there are circumstances in which the concessionaire body (such as NHAI) would not allow a change in control or ownership and might instead impose a lock-in term for the transaction. It should be possible to transfer one hundred percent of ownership to an InvIT on a case-by-case basis so that administration may be improved.

3. Tax benefit taken into account due to a change in ownership: certain SPVs may have pushed forward tax losses.It is possible for the SPV to lose the tax benefit as a result of a change in control ownership in the event that ownership is transferred to an InvIT (the InvIT must own a minimum of 51% of the SPV). If SPVs are allowed to keep receiving tax benefits after InvITs are created, this will help make InvITs more appealing to investors.

4. Stamp duties: It is possible to receive a waiver for the stamp duty that must be paid during the process of transferring an asset to an InvIT.

5. One point of contact: There should be one point of contact for all regulatory approvals that are associated with the SPV and the InvIT.

6. The number of Sponsors: At this time, the sponsor(s) jointly are required to hold not less than 10% of the total units of the InvIT after the initial offer of units, on a post-issue basis, for a period of not less than 3 years from the day that such units were listed on the market. The intention of the regulator to allow five sponsors is a step in the right direction since it would enable those sponsors to make available more funds for new investments and will also diversify the holding structure.

7. The tax treatment of capital gains: It needs to be on a same footing with that of equity investments.

8. Investment by Insurance Companies: The Insurance Regulatory and Development Authority ought to make it possible for insurance companies to invest in Infrastructure Investment Trusts (InvITs), as part of the Infrastructure Sector.

Even if the worldwide pandemic has slowed down the expansion of the Indian economy, there is still a great deal of anticipation about investments in its infrastructure sector from foreign investors. In the future years, it is anticipated that an increasing number of InvlTs will be put into operation. This is due to the urgent need for increased investment of infrastructure, as well as the relaxation of restrictions. The rules and compliance regulations have also been loosened up by the regulatory authorities in order to promote a larger involvement. In addition, Infrastructure Investment Trusts (InviTs) have the potential to serve as effective investment vehicles, which can guarantee long-term funding for infrastructure projects from retail investors as well as international institutional funds. It has been shown before that the aforementioned investment vehicles are advantageous for both investors and developers alike due to the fact that they guarantee high yielding returns over an extended period of time.

Before making any choice that is in any way connected to such investments, it is imperative that the risks that are linked with such investments, such as increased operational expenses as a result of inflation and large changes brought about in the regulatory environment, be kept in mind.

[1] Oxford Economics, ‘Global Infrastructure Outlook’ (Oxford Economics Blog, 20 June 2019) https://blog.oxfordeconomics.com/global-infrastructure-outlook accessed 10 April 2023.

[2] Axis Direct, ‘Thematic Report on Infrastructure Investment Trust (InvITs)’ (July 2019) https://simplehai.axisdirect.in/app/index.php/insights/reports/downloadReport/file/INVITs+Main+-+Thematic+Report+-+08072019_10-07-2019_13.pdf/type/fundame accessed 10 April 2023.

[3] Cyril Amarchand Mangaldas, ‘Deconstructing InvITs and REITs, 2nd Edition’ (2020) https://www.cyrilshroff.com/wp-content/uploads/2020/10/Deconstructing-InvITs-REITs-NEW-11-oct.pdf accessed 10 April 2023.

[4] Securities and Exchange Board of India, ‘Infrastructure Investment Trusts Regulations 2014 (Last Amended on May 4, 2022)’ (May 2022) https://www.sebi.gov.in/legal/regulations/may-2022/securities-and-exchange-board-of-india-infrastructure-investment-trusts-regulations-2014-last-amended-on-may-4-2022-_58818.html accessed 10 April 2023.

[5] Securities and Exchange Board of India, ‘Guidelines for Determination of Bidding, Allotment and Trading Lot Size for Real Estate Investment Trusts (REITs) and Infrastructure Investment Trusts (InvITs)’ (Circular, April 2019) https://www.sebi.gov.in/legal/circulars/apr-2019/guidelines-for-determination-of-bidding-allotment-and-trading-lot-size-for-real-estate-investment-trusts-reits-and-infrastructure-investment-trusts-invits-42772.html accessed 10 April 2023.

[6] Insolvency and Bankruptcy Board of India, ‘Securities’ (n.d.) https://www.ibbi.gov.in/uploads/resources/Securities accessed 10 April 2023.

[7] Securities and Exchange Board of India, ‘Amendments to Guidelines for Preferential Issue and Institutional Placement of Units by a Listed InvIT’ (Circular, 29 September 2020) https://www.sebi.gov.in/legal/circulars/sep-2020/amendments-to-guidelines-for-preferential-issue-and-institutional-placement-of-units-by-a-listed-invit_47587.html accessed 10 April 2023.

[8] Securities and Exchange Board of India, ‘Relaxation from Compliance to REITs and InvITs due to the COVID-19 Virus Pandemic’ (Circular, 23 March 2020) https://www.sebi.gov.in/legal/circulars/mar-2020/relaxation-from-compliance-to-reits-and-invits-due-to-the-covid-19-virus-pandemic_46323.html accessed 10 April 2023.

[9] Soubhik Das, ‘InvITs: The Next Big Infra Story’ (24 August 2020) Livemint https://www.livemint.com/industry/infrastructure/invits-the-next-big-infra-story-11597814096232.html accessed 10 April 2023.

[10] Securities and Exchange Board of India, ‘Infrastructure Investment Trusts Regulations 2014 (Last Amended on May 4, 2022)’ (May 2022) https://www.sebi.gov.in/legal/regulations/may-2022/securities-and-exchange-board-of-india-infrastructure-investment-trusts-regulations-2014-last-amended-on-may-4-2022-_58818.html accessed 10 April 2023.

[11] Sterlite Power, ‘Harsh Shah, CEO, IndiGrid, talks in detail about InvIT and how it works’ (Sterlite Power, 17 July 2020) https://www.sterlitepower.com/news/detail/harsh-shah-ceo-indigrid-talks-detail-about-invit-and-how-it-works accessed 10 April 2023

[12] Ibid.

[13] Pranav Mukul, ‘Explained: How NHAI plans to monetise its highways through InvITs’ (Indian Express, 9 September 2020) https://indianexpress.com/article/explained/explained-how-nhai-plans-to-monetise-its-highways-through-invits-6605500/ accessed 10 April 2023.

[14] Ibid.

[15] Harsh Shah, ‘InvITs: Gamechanger for Infrastructure Financing in India’ (Infraline issue, November 2018) https://www.indigrid.co.in/pdf/Infraline%20November%20Issue%20Harsh%20Shah%20Article.pdf accessed 23 April 2023.

[16] Securities and Exchange Board of India, ‘Infrastructure Investment Trusts Regulations 2014 (Last Amended on May 4, 2022)’ (May 2022) https://www.sebi.gov.in/legal/regulations/may-2022/securities-and-exchange-board-of-india-infrastructure-investment-trusts-regulations-2014-last-amended-on-may-4-2022-_58818.html accessed 10 April 2023.

[17] Securities and Exchange Board of India, ‘Infrastructure Investment Trusts Regulations 2014 (Last Amended on May 4, 2022)’ (May 2022) https://www.sebi.gov.in/legal/regulations/may-2022/securities-and-exchange-board-of-india-infrastructure-investment-trusts-regulations-2014-last-amended-on-may-4-2022-_58818.html accessed 10 April 2023.

[18] Securities and Exchange Board of India, ‘Infrastructure Investment Trusts Regulations 2014 (Last Amended on May 4, 2022)’ (May 2022) https://www.sebi.gov.in/legal/regulations/may-2022/securities-and-exchange-board-of-india-infrastructure-investment-trusts-regulations-2014-last-amended-on-may-4-2022-_58818.html accessed 10 April 2023.

[19] Ganesh Rao and Pallabi Ghosal, ‘Indian Infrastructure Investment Trusts: Key Considerations and Implications for Foreign Investors’ (AZB & Partners, Spring 2018) https://www.globalprivatecapital.org/app/uploads/2018/06/LRB_Spring_2018_AZB.pdf accessed 10 April 2023.

[20] Harsh Shah, ‘InvITs: Gamechanger for Infrastructure Financing in India’ (Infraline issue, November 2018) https://www.indigrid.co.in/pdf/Infraline%20November%20Issue%20Harsh%20Shah%20Article.pdf accessed 10 April 2023.