“SEBI enhances LODR regulations: Introducing stricter timelines for disclosures, mandatory material event verification for top 250 companies, and clarity on market rumors. Aimed at fostering transparency and investor trust.”

CONSULTATION PAPER ON REVIEW OF DISCLOSURE REQUIREMENTS FOR MATERIAL EVENTS OR INFORMATION UNDER SEBI (LODR) REG, 2015

BACKGROUND:

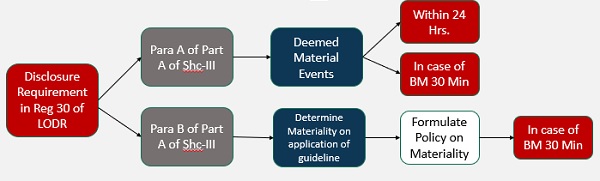

√ Reg 30: LE was required to disclose material events specified in Para A & B of Part A of Sch-III.

√ Various instances observed of inadequate / misleading / delayed disclosures at last hours.

√ No Uniformity in Policy for Disclosure on Material Events.

√ LEs were taking discretion of not disclosing material event wherever possible.

√ Policy adopted were too generic in nature.

√ Many Complaints and representation received by SEBI.

√ Some LE also represented for review and change in existing provisions.

EXISTING DISCLOSURE REQUIREMENT IN REG. 30 SEBI (LODR) REG. 2015

BELOW CRITERIA FOR DETERMINING MATERAILY REG. 30(4)(i):

√ Any act/ omission which is likely to influence the commercial & Economic Decision of the stakeholders; or

√ Any act resulting in Discontinuity/ alteration of an event or information already available publicly; or

√ Any act/ omission which if comes into limelight at a future date would result in significant market reaction.

INTRODUCTION OF CONSULTATION PAPER:

SEBI proposes to:

√ streamlining the disclosure requirements for material events.

√ remove discretion to the possible extent

√ Introduce quantitative threshold.

√ Bring uniformity in Materiality Policy for Disclosure.

√ Reduce timeline for disclosure.

√ Make it mandatory to verify the market rumours for Top 250 LE.

√ Require disclosure of communication from any regulatory, statutory, enforcement or judicial authority:

√ Add/ modify some events in Para A & B.

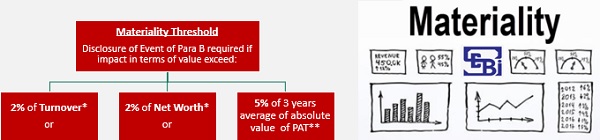

MATERIALITY THRESHOLD Reg 30(4)(i):

√ The events specified in Para B are required to be disclosed upon application of criteria of materiality as per reg 30(4).

√ LE do not disclose on ground that events are not material as per Materiality Policy for Disclosure of LE.

√ Hence, it was required to make reg 30(4) more objective & non-discretionary;

*as per the last audited standalone financial statements

** as per the last three audited standalone financial statements

MATERIALITY POLICY Reg 30(4)(ii) :

Existing Provisions Reg 30(4)(ii): The listed entity shall frame a policy for determination of materiality, based on criteria specified in this sub-regulation, duly approved by its board of directors, which shall be disclosed on its website.

LE are proposed to:

√ provide additional quantitative threshold/ criteria for determining materiality in addition to Reg 30(4);

√ Frame policy to assist its employees in easily identifying potential material event & reporting it to KMP for onward disclosure;

√ Make policy more objective and non-discretionary.

Proposed amendments to be made:

a) Include additional Quantitative Criteria, which shall not dilute existing requirements.

b) Policy to assist employees in identifying potential material event or information which shall be escalated and reported to the relevant KMP for determining materiality and disclosure to SE.

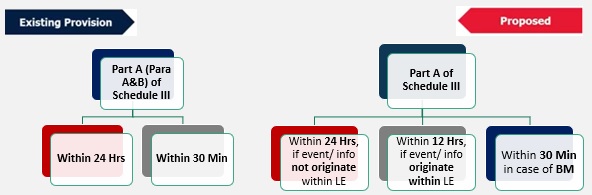

TIMELINE FOR DISCLOSURE Reg 30(6):

√ Timeline to disclose events as specified in Part A of Sch III is 24 hrs or as soon as reasonably possible.

√ Due to digital communication and social media, information permeates very fast.

√ it was observed that, disclosure of an event by the LE is made at the last hrs.

√ Hence, It is proposed to reduce the disclosure timeline from 24hrs to 12hrs.

√ Information emanates from BM outcome be disclosed in 30 min.

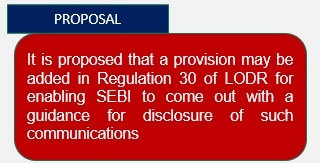

VERIFICATION OF MARKET RUMOURS Reg 30(11):

√ Existing Reg 30(11) states LE may on its own initiative, confirm or deny any reported event or information to SE;

√ At present, Influence of Print & Digital media and television is significant;

√ In order to stay contemporary, companies need to keep pace and ensure verification of such rumors.

√ Hence, a specific provision may be added thereunder mandating verification of such material events or information by top 250 listed entities to begin with.

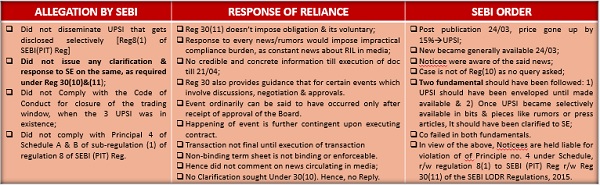

VERIFICATION OF MARKET RUMOURS (CASE LAW):

RELIANCE JIO ↔ FACEBOOK DEAL:

Fact of the case:

√ News on Facebook-Jio investment deal in Financial Times @London 24/03/20

√ circulated in Indian media same & next day

√ Concluded DD on 17/04/2020; BM: 18/04/20; Execution of transaction doc: 21/04/20

√ corporate announcement made on April 22, 2020

√ scrip price of the RIL went up by almost 15% on March 25, 2020.

Disclosure of Communication From Any Regulatory, Statutory, Enforcement Or Judicial Authority *Reg 30(13):

√ At present many LE disclosure pursuant to receipt of a communication (notice, order, direction, etc.) from any regulatory or judicial authority;

√ LE as best practice, disclose copy of such communication/ its web link;

√ Many LE use discretion to their advantage and do not disclose such info;

√ Hence, some communication may contain Material information which, if not disclose, may not be available to stakeholders at large;

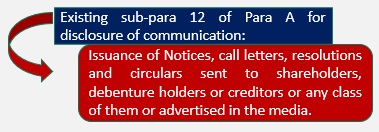

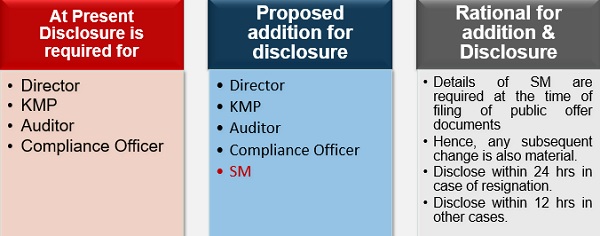

MASS ANNOUNCEMENTS & COMMUNICATION BY DIRECTORS/ PROMOTERS/ KMP/ SM:

√ Keeping track of all announcement is difficult;

√ Media announcements are considered significant from the perspective of the LE & stakeholders;

√ Hence, it is proposed to make it mandatory for LE to disclose to SE within 12 hrs;

√ This shall give impartial benefit to all stakeholders.

√ The new sub para 18 in Para A is proposed to be inserted.

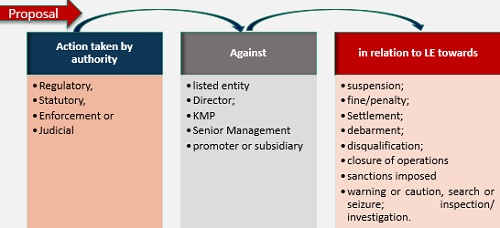

REGULATORY ACTION(s) WITH IMPACT (NEW SUB-PARA 19 IN PARA A):

√ Sub-para 8: Litigation(s) / dispute(s) / regulatory action(s) with impact;

√ Earlier disclosure for sub-para 8 of Para B was discretionary;

√ At some point the regulatory action has massive impact on LE;

√ Such disclosure shall enable investors to take informed decisions.

Disclosure to include below:

- Name of the authority;

- Nature and details of the action(s) taken or initiated;

- Date of receipt of direction or interim/ final order;

- Details of Default;

- Impact on financial, operation or other activities of LE.

| Sub-Para of Para A | Proposal for inserting new sub-para in Para-A of Part-A of Schedule III | Disclosure Timeline |

| 7C | Resignation of KMP, SM & Directors other than ID with letter having detailed reason. | within 7 days from date of resignation. |

| 7D | Non-availability of MD / CEO to perform his roles and responsibilities for a long period of more than a month. | Disclose within 12 hrs. |

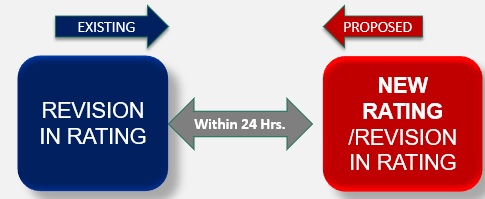

NEW RATING & REVISION THEREOF (SUB-PARA-3):

The disclosure of rating or revision in rating shall be made even if it was not requested for by the LE or the request was withdrawn by the LE.

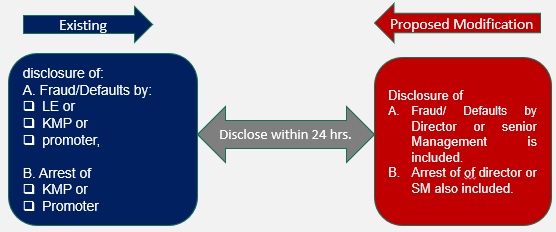

MODIFICATION IN SUB-PARA 6 OF PARA A:

Impact:

- The Fraud/ Arrest by Director or Senior Management is also material for the decision making of investor;

- These information also has impact on the price of the securities listed on stock exchange;

- Dissemination shall provide an equal/ fair opportunity to all stakeholders.

- To remove ambiguity, an explanation of the term ‘default’ may be added. It may also be clarified that fraud/ default/ arrest is required to be disclosed whether it has happened in India or abroad.

Change in KMP/Resignation (Sub-Para-7):

#Resignation Letter and detailed reason as per sub para 7C is required to be disclosed within 7 days from the date of Resignation.

DELAY OR DEFAULT IN PAYMENT OF FINES/ PENALTIES/ DUES ETC. (Sub Para 13 of Para-B):

OTHER MODIFICATION IN PARA A:

| Sub-para 11 of Para A | LE is required to disclose any Winding up petition filed by any party /creditors.

Timeline LE to disclose within 24 hours |

|

| Sub-para 15 of Para A | (a) Schedule of analysts or institutional investors meet, at least two working days in advance (excluding the date of the intimation and the date of the meet), and presentations made by the listed entity to analysts or institutional investors. | LE is required to disclose all investor meet at least 2 days prior to such meeting. |

EVENTS PROPOSED TO BE MODIFIED IN PARA B OF PART-A OF SCHEDULE-III:

|

Sub-Para of Para B |

Existing disclosure requirement/ provision | Proposed addition/ Modification in Para-B | Disclosure Timeline/ View |

| 2 | Disclosure of material tie-ups, adoption of new line(s) of business & closure of operations only if it bring change in its general character or nature of business of LE. | Requirement of change in generic character/ nature of business is removed. In event closure of operation of subsidiary is added. | within 12 hrs. |

| 3 | Capacity addition or product launch | No change. Timeline is reduced to 12hrs | within 12 hrs. |

| 5 | Agreements (viz. loan agreement(s) as a borrower or any other agreement(s) which are binding and not in normal course of business) and revision(s) or amendment(s) or termination(s) thereof. | The word as a Borrower is removed. Below & explanation is added:

“Disclosure of loan agreement for lending shall not be applicable to a listed entity which is a bank or a non-banking financial company” SEBI has also invited comment on whether loan to WOS is material & disclosure of agreement thereto is required. |

within 12 hrs.

(Lending agreement which are binding and not in normal course is also be material for the decision making) |

| 8 | Material litigations or disputes where the LE, or its KMP, or promoter, or ultimate person in control becomes a party are required to be disclosed. | Additionally, information pertaining to material litigations or disputes where the subsidiary or director of the LE becomes a party is also material information for investors. | within 12 hrs |

| 11 | Giving of guarantees or indemnity or becoming a surety, for any third party | Giving of guarantees or indemnity or becoming a surety, by whatever name called, for any third party | Within 12 hrs. Added to make this para wide and inclusive. |

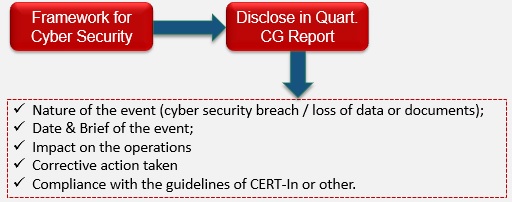

PROPOSED FRAMEWORK FOR CYBER SECURITY (IN LODR Reg.):

- Increase in Importance & use of Technology

- Incidences of cyber crime/ breaches is major concern;

- It impacts the operations and/or performance of LE;

- Hence, Disclosure is necessary for informed decision;

- Immediate disclosure may be vulnerable to further attacks;

- Hence, Disclosure with root cause & ATR is necessary;