Updated Return – Section 139(8A):

Rationale behind Introduction:

→ Section 139(4) facilitates filing of Belated Return & Section 139(5) facilitates filing of Revised Return before 3 months prior to the end of the relevant Asst. Year or before completion of Assessment, whichever is earlier.

→ This existing provision provides an additional time of approx. 5 months to an individual assessee, 2 months to a company/auditable case and 1 month to an assessee who enters into an international transaction or specified domestic transaction respectively, to file belated or revised return.

> This additional timeline for filing a revised/belated return may not be adequate when we factor in utilization of huge information and data available coupled with the “nudge approach” that motivates the taxpayer towards the desired objective of voluntary tax compliance, starting with filing of correct tax returns.

> The proposal for updated return over a period longer than that is provided in the existing provisions of the Income-tax Act would on one hand bring use of huge data with the IT Department to a logical conclusion resulting in additional revenue realization and on the other hand, it will facilitate ease of compliance to the taxpayer in a litigation free environment.

Who can file Updated Return and When can it be filed?

→ Any Person, whether or not a Return has been filed u/s 139(1), 139(4) or 139(5)

→ Within 24 months from the end of the relevant Asst. Year

Conditions for filing an Updated Return:

This Section shall not apply if the Updated Return:

→ Is a return of a loss.

→ Has the effect of decreasing the total tax liability determined in the Return furnished under Section 139(1) or Section 139(4) or Section 139(5).

→ Results in Refund due on the basis of Return furnished under Section 139(1) or Section 139(4) or Section 139(5).

→ Increases the Refund due on the basis of Return furnished under Section 139(1) or Section 139(4) or Section 139(5).

Restrictions on filing an Updated Return:

Updated Return cannot be filed in the following cases:

→ Search (S.132) / Survey (S.133A):

> Search initiated u/s 132 or Survey conducted u/s 133A.

> Notice has been issued that any money, bullion, jewellery, books, documents, etc. seized or requisitioned u/s 132 or u/s 132A in the case of any other person belongs to or relates to such person.

→ Updated Return:

> An Updated Return has already been furnished by him under this Sub-section.

→ Proceedings (Pending or Completed):

> Any Proceeding for Assessment or Reassessment or Recomputation or Revision of Income under this Act is pending or is been completed.

→ Information under other Acts:

> The AO has information in his possession under the PMLA Act, Black Money Act, Benami Property Act or Smugglers & Foreign Exchange Manipulators (Forfeiture of Property) Act & the same has been communicated to the Assessee.

→ Information u/s 90 and 90A:

> The AO has information in his possession under Section 90 and Section 90A & the same has been communicated to the Assessee.

→ Prosecution Proceedings:

> Any Prosecution Proceedings under the Chapter XXII have been initiated for the relevant assessment year in respect of such person.

Loss Return:

→ If any person has sustained a loss in any previous year and has furnished a return of loss within the time allowed under sub-section (1), he shall be allowed to furnish an updated return where such updated return is a return of income.

→ Also that if the loss or any part thereof c/f under Chapter VI or unabsorbed depreciation c/f u/s section 32(2) or tax credit c/f under section 115JAA/JD is to be reduced for any subsequent previous year as a result of furnishing of return of income under this sub-section for a previous year, an updated return shall be furnished for each such subsequent previous year.

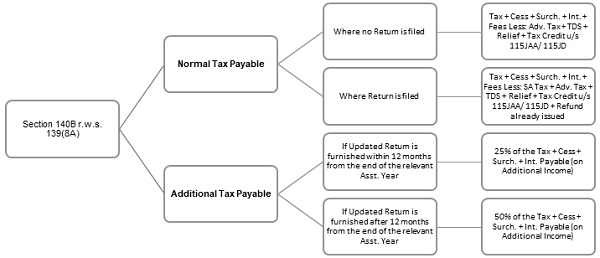

Tax Payable on Updated Return (Section 140B r.w.s. 139(8A):

Practical Example:

| Particulars

(Individual, A.Y. 2021-22) |

Original Return u/s 139(1) | Updated Return u/s 139(8A) |

| Net Total Income | 6,00,000 | 9,00,000 |

| Tax incl. Cess | 33,800 | 96,200 |

| Less: Advance Tax | 10,000 | 10,000 |

| Add: Interest u/s 234B / 234C | 2,555 | 22,133 |

| Normal Tax Payable | 26,360 | 1,08,333 |

| Less: Tax already paid | 26,360 | 26,360 |

| Balance Tax Payable | NIL | 81,973 |

| Add: Additional Tax @ 25% of the above | N.A. | 20,493 |

| Final Tax Payable | NIL | 1,02,466 |

Defective Return – Section 139(8A) r.w.s. 139(9) and 140B:

→ An Updated Return shall be regarded as Defective Return u/s 139(9) if the Return is not accompanied by the proof of Payment of Tax required u/s 140B.

→ Currently, the Income Tax Portal is not accepting the Updated Return if the details of Tax Paid u/s 140B is not entered in the Return.

Time Limit for Various Years to file an Updated Return:

| Asst. Year | Updated Return Time Limit | |

| With 25% Additional Tax | With 50% Additional Tax | |

| A.Y. 2019-2020 |

* |

* |

| A.Y. 2020-2021 |

* |

31/03/2023 |

| A.Y. 2021-2022 | 31/03/2023 | 31/03/2024 |

| A.Y. 2022-2023 | 31/03/2024 | 31/03/2025 |

* – Since New Provisions are applicable from 01/04/2022, hence updated return can never be filed

Contemplating Various Scenarios:

? Can Updated Returns replace Past Returns?

Updated Return is an opportunity provided to the Assessee to declare any Income not offered by him while filing the Original/ Belated Return. Accordingly, any Updated Return filed by the Assessee would replace the Past Returns filed by the Assessee.

? Can Updated Return be filed Multiple Times?

Clause (a) under Third Proviso to Sub-Section 8A of Section 139 clearly specifies that no Updated Return can be filed by the Assessee where an Updated Return has been furnished by him under this Sub-Section.

Accordingly, one can file a Revised Updated Return after the Return already filed u/s 139(1), 139(4) or 139(5) ONLY ONCE.

? When to opt for Updated Return over Belated / Revised Return?

Belated Return can be filed u/s 139(4) when one misses the due date specified u/s 139(1) and can be filed before 3 months prior to the end of the relevant Asst. Year or before completion of Assessment, whichever is earlier.

Revised Return can be filed u/s 139(5) when one discovers any omission or any wrong statement filed in the Return filed u/s 139(1) or 139(4) and can be filed before 3 months prior to the end of the relevant Asst. Year or before completion of Assessment, whichever is earlier.

Updated Return can be filed u/s 139(8A) when:

-

-

- One misses the due date for filing Belated Return u/s 139(4) and there is Taxable Income on which Tax is Liable to be paid.

-

OR

- One discovers any omission or any wrong statement filed in the Return filed u/s 139(1) or 139(4) and time limit for Revising the Return u/s 139(5) has lapsed and there is Tax Payable on the Additional Income.

? Can Audit Report be filed along with Updated Returns?

Currently, there is no provision to file Audit Report along with Updated Return. However, at the time of filing Updated Return, the Income Tax Portal asks whether the Assessee is liable to Tax Audit or not.

? As per the latest update of the Income Tax Portal, we are able to file Updated Return for A.Y. 2022-23 with 25% Additional Tax from 02/01/2023, thereby giving extended period of 15 months i.e. from Jan.’23 to Mar.’24?

The Provisions for Section 139(8A) allows filing of Updated Return with 25% Additional Tax within 12 months from the end of the relevant Asst. Year.

However, currently the Income Tax Portal seems to be accepting the Updated Return for A.Y. 2022-23 with 25% Additional Tax from Jan.’23 which will be available till Mar.’24 i.e. 15 months.

? Can NIL Return be filed or Nominal Taxes be paid in Updated Return?

A NIL Return or a Return claiming c/f of Losses cannot be filed via Updated Return.

An Updated Return with Additional Nominal Taxes can be filed. Even an Updated Return with only Additional Fees u/s 234F of Rs.1,000/- can be filed.

? Can Refund be claimed by filing Updated Return?

Refund cannot be claimed by filing Updated Return.

In order to claim Refund, recourse may be taken under Section 119 by filing an Application for Condonation of Delay before the Hon’ble Principal Commission of Income Tax.

Author Bio

If updated return become invalid then shall we again file an updated return for the same AY?

can i upload itr under efile 139(8a) after receiving defective notice for incomplete itr submission

I Filed My ITR-III on 24th Nov,2022, But e-Verification Time Passed. Can i file U/s. 139(8A) Without 25% Additional Tax. as already paid 2.28 Lacs Tax in original Return.

if company files return under 115BAA opting for 22% but could not file form 10-IE. can company file updated return now by opting for 25% or it will be liable to pay at 30% ?

Option to opt u/s 115BAA is available online when return is filed within the time allowed under Section 139(1) by filing Form 10IC.

For opting 25% u/s 115BA, Form 10IB needs to be filed before the due date u/s 139(1) for furnishing the *first* of the returns of income which the company is required to furnish. Further, the option once exercised cannot be withdrawn.

25% tax rate can be opted by the Domestic Company if the total turnover or gross receipts of previous year does not exceed Rs.400 crores irrespective of the date of filing the return.