Government of India

National Financial Reporting Authority

7th Floor, Hindustan Times House,

Kasturba Gandhi Marg, New Delhi

Order No. NF-23/30/2021 |Date: 19.09.2022

Order under Section 132(4) of the Companies Act 2013 in respect of CA Rajiv Bengali (ICAI Membership No. 043998)

1. Information was received from the Registrar of Companies Mumbai vide letter dated 17.11.2020 relating to possible non-compliance with the auditing standards by the Statutory Auditor of Trilogic Digital Media Limited (TDML hereafter). The matter was taken up for investigation under section 132 (4) of the Companies Act 2013 (the Act hereafter) for investigating into Professional Misconduct, if any, by the Statutory Auditor.

2. TDML, a company listed on Bombay Stock Exchange (BSE hereafter), was in the business of media and content syndication. TDML was required to prepare its Financial Statements for the Financial Year (FY hereafter) 201617 in accordance with the schedule III and other applicable provisions of the Companies Act 2013 and Accounting Standards (AS hereafter) notified under the Companies (Accounting Standards) Rules, 2006.

3. M/s Subramaniam Bengali & Associates was the statutory auditor of TDML for FY 2016-17 and CA Rajiv Bengali was the Engagement Partner (EP hereafter) for this audit.

4. On a preliminary examination of Financial Statements downloaded from BSE website (TDML did not have a working website), it was found that the TDML had not complied with the Accounting Standards and provisions of the Act in the preparation and presentation of its Financial Statements for FY 2016-17, resulting in material misstatements of various figures and disclosures. Vide letter dated 22.03.2022, the Audit File along with other information were called from M/s Subramaniam Bengali & Associates and the EP, giving 30 days’ time for submission of required documents. CA Rajiv Bengali, the EP of the Audit Firm, submitted the Audit File in respect of audit of TDML for FY 2016-17 on 03.05.2022.

5. On examination of the Audit File, it is observed that the audit had been conducted in disregard of most of the Standards on Auditing (SA hereafter) and the Act. Despite this, on 30.05.2017 the EP had issued an unmodified audit opinion in the Independent Auditor’s Report on behalf of the Audit Firm giving TDML a clean chit and stating that “…. financial statements give the information required by the Act in the manner so required and give a true and fair view in conformity with the accounting principles generally accepted in India: a) in the case of the Balance Sheet, of the state of affairs of the Company as at 31st March, 2017, b) in the case of the Statement of Profit and Loss for the period ended on that date, c) in the case of the Statement of Cash Flow for the year ended on that date”.

6. On satisfaction that a sufficient cause existed to take action under subsection (4) of section 132 of the Companies Act, a Show Cause Notice (SCN hereafter) was issued to CA Rajiv Bengali on 06.07.2022 in terms of Rule 11 of the NFRA Rules 2018, asking him to show cause as to why action should not be taken against him for professional misconduct in respect of his performance as the Engagement Partner on behalf of M/s Subramaniam Bengali & Associates, the Statutory Auditor of TDML for the FY 2016-17. The EP was charged with professional misconduct of:

a. failure to disclose a material fact known to him, which is not disclosed in a financial statement, but disclosure of which is necessary in making such financial statement, where he is concerned with that financial statement in a professional capacity;

b. failure to report a material misstatement known to him to appear in a financial statement with which the EP is concerned in a professional capacity;

c. failure to exercise due diligence, and being grossly negligent in the conduct of professional duties;

d. failure to obtain sufficient information which is necessary for expression of an opinion, or its exceptions are sufficiently material to negate the expression of an opinion; and

e. failure to invite attention to any material departure from the generally accepted procedures of audit applicable to the circumstances.

7. As the EP did not submit any reply within the stipulated period, a mail dated 10.08.2022 was again sent advising him to submit the reply by 17.08.2022, failing which it would be construed that he had nothing to say in the matter and the issue would be decided based on materials on record. Thereafter, the EP submitted his reply on 16.08.2022.

8. The EP has been evasive in his replies and has not specifically responded to the allegations of non-compliance with statutory requirements. He has mentioned that non communication with the management and breakdown of Computer Systems were the reasons for non-availability of Audit Evidence in Audit File. The EP has accepted his lapses in respect of some of the charges in the SCN, adding that the audit was completed when he was under stress because of his health and was completed in a hurried manner. He also submitted that his Systems were damaged, and he had to change almost the entire Systems; and that all the data could not be recovered, especially the mails which were very much part of the documentation.

9. The SCN gave the EP an opportunity of personal hearing but the EP has chosen not to avail of the same. Thus, this order is based on the written replies of the EP and other materials available on record.

10. We have perused all the materials on record including the written response of the EP. Some of the major violations relate to False reporting in the Independent Auditor’s Report about truthfulness & fairness of Cash Flow Statement (CFS hereafter) despite non preparation of CFS by TDML, False reporting that TDML was registered under Reserve Bank of India Act, which was factually not correct, Failure to evaluate ‘Going Concern’ assumption despite availability of adverse indicators, Failure to recognize the possibility of risk of material misstatements due to fraud despite recognition of unusual expenditures by TDML, Failure to identify Related Party Transactions, Violation of large number of Standards on Auditing and Failure to report non-compliance with Accounting Standards & provisions of the Companies Act 2013 etc. Each of these charges are analysed and discussed under three broad categories:

A. False reporting by Auditor in Independent Auditor’s Report.

B. Failure to comply with Standards on Auditing.

C. Failure to report non compliances with Accounting Standards and provisions of the Companies Act 2013.

A. False reporting by Auditor in Independent Auditor’s Report

11. The EP was charged’ with false reporting in the Independent Auditor’s Report as he reported that he had audited the Cash Flow Statement (CFS) and it gave a true & fair view, whereas the Financial Statements submitted by the EP and the Annual Report downloaded from the Bombay Stock Exchange website did not contain the CFS. One of the integral components of Financial Statements, as per section 2(40) of the Act, is the CFS which is to be prepared as per Accounting Standards-3 ‘Cash Flow Statements’. The Auditor was required, under section 143(2) of the Act, to report whether the CFS gives a true and fair view of the cash flow for the year.

11.1 Responding to the charge, the EP has replied that, “The cash flow was prepared and was ready but was not attached to the Financial Statements inadvertently because it was made in a separate file and was not in the same file as of Financial Statements. I am attaching herewith the Cash Flow Statement”.

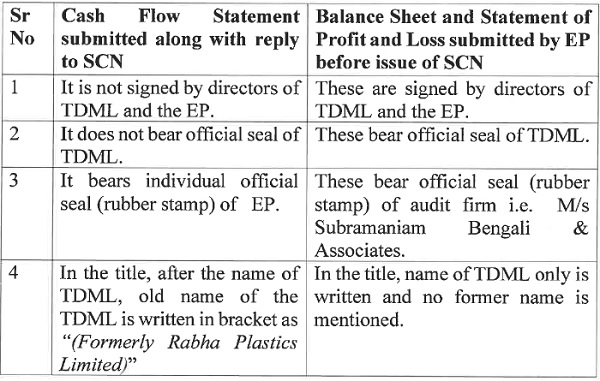

11.2 We observe that the Audit File submitted by the EP did not have the CFS and the EP had averred through an Affidavit dated 03.05.2022 that the information submitted was true and complete in all respects and nothing had been concealed. The CFS was not available in the Audit File or the BSE website but was later submitted along with the reply to the SCN, raising a strong suspicion that this CFS is an after- thought and has been prepared or obtained subsequently. This is further corroborated by the fact that the manner of preparation & signing of the CFS submitted by the EP along with reply to SCN is totally different from that of the Balance Sheet and the Statement of Profit and Loss submitted along with the Audit File. The differences are tabulated as under:

11.3 From the above, it can be reasonably inferred that the EP has prepared the Cash Flow Statement after receipt of SCN and attached the same with his reply to SCN with the intention to mislead us. This act of the EP amounts to falsification of the Financial Statements.

12. The EP was charged2 with false reporting in the Independent Auditor’s Report which shows that TDML was registered under section 45 IA of the Reserve Bank of India Act 1934 (applicable for Non-Banking Finance Companies-NBFCs) and was holding a registration certificate for the same. In fact, as seen from Annual Report, TDML was in the business of media and content syndication and not an NBFC. TDML was not registered under RBI Act and was not holding such registration certificate.

12.1 Responding to this charge the EP stated that, “Reporting company as NFBC is purely a Typographical Error and which should not have been done”.

12.2 We find that the Auditor was required as per para (xvi) of the Companies (Auditor’s Report) Order, 2016 (CARO) to report “whether the company is required to be registered under section 45-IA of the Reserve Bank of India Act, 1934 and if so, whether the registration has been obtained”. Such reporting is to be done only after performing audit procedures to examine applicability of the RBI provisions to the auditee company. There is no evidence in the Audit File that the EP exercised due diligence by evaluating whether the company was NBFC or not. But the audit report disclosed it to be an NBFC. The EP has accepted his mistake but casually calls it a ‘typographical error’. This establishes the lack of due diligence in professional reporting.

13. The EP was charged’ with false reporting in the Independent Auditor’s Report that TDML had provided in its Financial Statements requisite disclosure about the holdings as well as dealings in Specified Bank Notes (SBN hereafter) for the period 08-11-2016 to 30-12-2016, as required under the Act’. This was a disclosure mandated for the specific period post demonetization. In fact, we observe that TDML did not provide such disclosure in the Financial Statements.

13.1 Responding to this charge the EP stated that, “The details as per the requirement of Companies Act 2013 regarding disclosure of SBN was kept ready but it was not signed and was sent to the Company after verification but was not made part of the Financial Statements”.

13.2 This reply makes it clear that the EP has accepted that the disclosure about SBN was not part of Financial Statements. In fact, once the company has not made a disclosure on SBN, the Auditor was dutybound to question the same and make a mention of the same in the audit report. On the contrary the EP has tried to mislead us by stating that he sent an unsigned disclosure to the company which was ultimately not placed in the Financial Statements. This reply is an attempt to cover up and mislead thereby reflecting a reckless and unprofessional behavior on the part of the EP.

B. Failure to comply with Standards on Auditing (SAs):

14. The SCN charged the EP5 with false reporting that the audit was conducted in accordance with SAs despite non-compliance with a large number of SAs discussed in succeeding paras.

14.1 Responding to these charges the EP stated, “I had carried out the audit in accordance with the SAs but as I have said earlier the query sheet and points raised during the audit were replied by the Company based on which the Financial Statements and Report was made. However due to mainly non communication with the Company I could not complete the Audit File along with necessary documents and secondly my systems were also damaged, and I had to almost change the entire system and all the data could not be recovered especially the mails which were very much part of the documentation”.

14.2 We note that the EP had a statutory duty6 to retain the audit documentation for seven years from the date of the Auditor’s Report. The Audit report in this case was signed on date 30-05-2017. Accordingly, the EP had a statutory duty to preserve the Audit File at least till 29-05-2024. Due diligence would require the EP to proper upkeep of Systems including back up of Audit File to ensure compliance with his statutory obligations. That he failed to do so points to gross negligence and unprofessionalism on his part. In any event, accepting such irresponsible replies would create a moral hazard making it easy for an Auditor to cite such lame excuses to shirk responsibility, defeating the very purpose of the statutory requirement of preserving audit documentation for seven years.

14.3 Further, there is no link between Systems failure and recovery of e-mails. Emails can be accessed from any System anywhere any time, be it old or new, be it a desktop or laptop or mobile etc. We find EP’s reply in this regard to be frivolous.

14.4 Para 41 of SA 700 (pre revised)7 provides that “The auditor’s report shall be dated no earlier than the date on which the auditor has obtained sufficient appropriate audit evidence on which to base the auditor ‘s opinion on the financial statements”. Accordingly, the EP was required to obtain sufficient appropriate audit evidence during the course of audit of Financial Statements and on or before signing of Audit Report. Therefore, the reply of the EP about non-communication with the company after signing of Audit Report, is not relevant for the purpose of keeping the Audit File and audit evidence obtained during the course of audit. It can reasonably be inferred from the reply of the EP that sufficient audit evidence was not obtained during the course of audit of Financial Statements, which is noncompliance with SA 700 (pre revised). This is a crystal-clear evidence that the audit was performed in a very perfunctory and casual manner.

14.5 The reply and explanation of the EP are therefore not accepted.

15. The EP was charged8 with non-compliance to SA 240. This SA deals with `The Auditor’s responsibilities relating to fraud in an Audit of Financial Statements’. It was found that the EP failed to recognise the possibility of risk of material misstatements due to fraud in respect of recognition of abnormal expenses of Sundry Balance Written off worth Rs 14.87 crores and Other Miscellaneous Expenses worth Rs 24.06 crores. He was also charged with failure to report non-disclosure of these extraordinary expenses in the Statement of Profit and Loss as per requirements of Accounting Standard-59 and Division I of Schedule III of the Act. Each extraordinary item along with its nature and amount was required to be separately disclosed in the Statement of Profit and Loss in a manner that its impact on current profit or loss could be perceived. However, TDML had not given such a disclosure in the Statement of Profit and Loss and wrongly aggregated these extraordinary items under the head ‘Other Expenses’.

15.1 The EP was also charged’ with non-compliance to SA 450 relating to `Evaluation of misstatements identified during the audit’ as he failed to document evidence of corrections of misstatement regarding bad debts from Rs 23.11 crores to Rs 14.87 crores. The EP was required to document the corrections of misstatements in the Financial Statements”. We observe that the EP had enquired with the management regarding details of Bad Debts amounting to Rs 23.11 crores shown in the Trial Balance. The Audit File do not reflect any work paper showing how the EP’s query was resolved. In the audited Financial Statements, however, Sundry Balance Written off (net) of Rs 14.87 crores was disclosed. No audit procedures were performed to verify the correctness of Sundry Balance Written off (net) for Rs 14.87 crores and genuineness of this transaction.

15.2 Responding to the charge relating to non-compliance to SA 240 the EP stated that – “There was no such circumstances and situation which would draw the attention to risk related to Material Misstatement due to Fraud.”

15.3 Responding to the charge of misstatement identified during audit the EP has stated that – “The reply is already given in response to query 4.1. I had done the audit with all the possibilities only problem arose was not able to complete the audit file because of non-communication with the Company and System Breakdown in my office.”

15.4 We note that the Sundry Balance Written off (Rs.14.87 crore) and Other Miscellaneous Expenditure (Rs.24.06 crore) constituted 54.50% of total expenses of Rs 71.43 crores in FY 2016-17 and were 3041% higher than the previous year’s expenses under both these account heads (Rs 1.28 crores). These expenses were unusual keeping in view the size and nature of business of TDML and the previous year’s expenses under these heads. The EP was required’ to evaluate whether the business rationale (or the lack thereof) of these transactions suggested fraudulent financial reporting or attempt to conceal misappropriation of assets. The EP was required to exercise Professional Skepticism 13 and enquire about the basis of such extraordinary expenditure. However, there is no evidence in Audit File that the EP has done such evaluation and exercised Professional Skepticism. Further, the EP has not given any explanation regarding his failure to report non-compliance with AS 5 and schedule III of the Act.

15.5 It is evident that the EP’s enquiry during the audit about the bad debts of Rs 23.11 crores resulted in TDML transferring the same to Other Miscellaneous Expenses. This further resulted in one more misstatement in the Financial Statements. The EP was aware of this misstatement but he neither documented this in the Audit File nor reported the same in his audit report, thus failing to comply with SA-450. His plea regarding non-communication with the TDML and Systems breakdown cannot be accepted for the reasons already mentioned before.

16. The EP was charged’ with non-compliance to SA 570 which deals with auditor’s responsibilities in the audit of Financial Statements relating to a `Going Concern’. The Financial Statements are prepared on the assumption that the entity is a ‘Going Concern’ and will continue its operations for the foreseeable future. The EP failed to obtain sufficient appropriate audit evidence regarding management’s use of the ‘Going Concern’ assumption in preparation of Financial Statements despite several adverse indicators in the Financial Statements that could raise significant doubt about the ‘Going Concern’ assumption and management’s intentions to continue operations. Such indicators included:

(i) Reduction in ‘Revenue from Operations’ from Rs 51 crores in FY 2015-16 to Rs 17.06 crores in FY 2016-17,

(ii) Reduction in Inventory from Rs 12.71 crores in FY 2015-16 to NIL in FY 2016-17,

(iii) Sundry Balances worth Rs 14.87 crores had been written off during the year,

(iv) Recognition of abnormal Miscellaneous Expenses of Rs 24.06 crores during the year and

(v) The company had incurred loss of Rs 54.37 crore, which resulted in

substantial reduction in Net Worth from Rs 58.89 crores as on 31.03.2016 to Rs 4.52 crores as on 31.03.2017.

16.1 Responding to the charge as to why the appropriate audit evidence about ‘Going Concern’ assumption was not obtained by the auditor, the EP stated that – “Revenue from operations had decreased due to some of the clients cancelled their orders and other business reasons. The stock of Rights of File Shoukeen was nil because it turned out to be super flop and it was not realizable. It can be verified now also because the said film is not shown on any TV channel. The Sundry Balance written off were the advances given which was not recoverable and other miscellaneous Expenses included Rs. 23.11 crores of Bad debts written off. These queries were raised during the field audit and was replied by them through mail but as I said I am unable to recover that data and at present I do not have any documents for the same.”

16.2 The indicators mentioned above would attract skepticism in any prudent person. There was no evidence in the Audit File to indicate that the EP had questioned the management and had done any audit procedure on the ‘Going Concern’ issue and as discussed above, the plea of the EP regarding non recovery of emails is not acceptable.

17. The EP was charged15 with non-compliance with SA 55016 as he failed to perform audit procedures to identify, assess and respond to the risk of material misstatements arising from Related Party Transactions (RPT hereafter). TDML was required to disclose the name, transaction and outstanding balance in respect of all Related Parties in accordance with AS 1817. TDML had not disclosed names of all Related Parties except that of Shri Vishal Shyam Gurnani, Managing Director, despite evidence in the Annual Report that TDML had other Executive Directors and there were frequent changes in the directorship of the TDML. Further, TDML has also not disclosed any transaction with Related Parties despite the fact that there were evidence in Audit File regarding RPTs such as loan transaction of Rs.1.40 crore & salary expenditure of Rs 25.76 lacs with Ms. Aparna Shah (Director of TDML and wife of Shri Vishal Shyam Gurnani Managing Director). Further, the audit work papers indicate question being raised about the related party status of trade payables of Rs 6.25 Lacs to Filidian Impex (India) Pvt Ltd, Rs 17.36 Lacs to Tri Digital Medium Pvt Ltd and Rs 23 Lacs to Vishal Gurnani Enterprises. There was no evidence that these were resolved.

17.1 Responding to the charge on Related Party Transactions the EP stated that – “The queries were raised during the field audit report which you have also mentioned. The respective response was also received through mails but as I said earlier due to breakdown of systems, I am unable to recover the data and give any proof on the issue. The same could not be recovered from the Company because we have no communication since last more than five years. Further you must have also observed that the Note No. 27 to the Financial Statement seems not complete. This is the reason the names of other related party which were there. Generally, the Full table is made but unfortunately not able to recover that data. As far as the change of Directors are concerned, I have no idea on that issue at present.”

17.2 As discussed earlier, the reply of the EP that he is not able to retrieve e-mails is unacceptable. The EP having failed to evaluate RPT and make appropriate disclosures regarding the same has thus not complied with SA 550.

18. The EP was charged’ with non- compliance with SA 230 relating to ‘Audit Documentation’ in that he had failed to document the nature, timing and extent of audit procedure performed and results thereof; failed to document audit evidence obtained, conclusions reached, communication with management & Those Charged With Governance (TCWG) etc.; he did not assemble the Audit File within 60 days of signing of audit report which is evident from the fact that he did not send the Audit Report and Financial Statements to NFRA along with the Audit File on 03.05.2022 but submitted them only on 10.05.2022 after NFRA advised him on 05.05.2022 to do so.

18.1 Responding to these charges the EP stated that – “The audit file was made with the name of the concerned persons and audit plan. My staff visited the Company Office and raised the query. However, as I said the response to query was through mail which unfortunately on my part not able to recover and present to yourself As far as not sending the Financial Statement to NFRA it was• purely unintentional and immediately sent you the Financial Statement and Audit Report on 5th of May 2022″.

18.2 On inadequate documentation, the reply of the EP regarding system breakdown has already been discussed at para 14 above and found not acceptable. The EP has not given any satisfactory reply for not submitting the Financial Statements and Audit Report along with Audit File.

19. The EP was charged’ with non-compliance to SA 200, SA 210, SA 220, SA 260, SA 265, SA 300, SA 315, SA 320, SA 330, SA 500, SA 505, SA 520, SA 580, SA 700, SA 710 and SA 720.

19.1 The EP further responded that “All the paragraphs and Paras of SAs mentioned in this clause is regarding the Documentation and/or that I have already said and again stating that there was no communication with the Company after the audit report was issued and unfortunately for us the mails received for confirming our stand on various issues were lost in system breakdown.”

19.2 We have already examined the reply of the EP regarding non communication with the company and Systems breakdown in the foregoing paragraphs and found them not acceptable. Therefore, we hold that the EP has not complied with the aforementioned SAs.

C. Non compliances with Accounting Standards (AS) and Provisions of the Companies Act 2013.

20. Financial Statements are to be prepared and certified as per the provisions of the Act and the rules made thereunder20. It is the primary responsibility of the EP to ensure that these are adhered to. The EP was charged’ with not obtaining audit evidence to support that Financial Statements were approved by the Board of Directors of TDML; and that the EP failed to report that Financial Statements were not signed as per requirement of the Act. The Financial Statements were required to be approved by the Board of Directors before these were signed by the EP on 30.05.2017 as per the provisions of the Act. However, there was no evidence in the Audit File that Financial Statements were approved by Board of Directors of TDML. Further, the Financial Statements were not signed by the Chief Finance Officer and Company Secretary, in violation of the provisions of the Act. The names of other signatories were not mentioned in the Financial Statements.

20.1 Responding to the charges the EP stated that “The Financial Statements were signed by the directors. The Audit report was signed and was given in good faith after getting the signature on the Balance Sheet but it was a mistake on my part to trust them for the same”.

20.2 Thus, the EP has accepted his lapse in not ascertaining that the persons as prescribed in the Act had signed the Financial Statements, and absent these, placing disclaimers about the same in his audit report. This is extreme lack of diligence on the part of a qualified professional to not insist to write the names of persons who signed on the Financial Statements as Directors of the TDML. The EP has not responded to the non-availability of audit evidence regarding approval of Financial Statements by the Board of Directors of TDML. Absent these the Financial Statements remain unverified thus making a mockery of the auditing responsibilities when this basic requirement is not adhered to.

21. The EP was charged’ with not ensuring compliance with AS 22 relating to ‘Accounting for Taxes on Income’ as TDML had recognised Deferred Tax Assets (DTA) of Rs 11.96 crores despite the fact that there was no reasonable certainty that sufficient future taxable income will be available against which such DTA can be realised. It was further charged that the EP had failed to report non-compliance with AS 22 in his Audit Report that resulted in violation of section 143(3)(e) of the Act and Rule 4(1) of the Companies (Accounting Standards) rules, 2006.

21.1 Responding to the charge regarding DTA, the EP stated that “As I have already stated earlier that there was no circumstances existed which will lead to the stage where company is not going concern. The Company was running business though one year of loss does not stop company from performing. This reason lead us to report the Deferred Tax Asset.”

21.2 The Audit File does not evidence that the EP had performed any audit procedure to evaluate whether there was reasonable certainty of future taxable income which could justify recognition of DTA, as required in AS-22. Despite clear indications in the Financial Statements (also discussed in Para 16 above) that raised questions about management’s intensions to carry on its operations, the EP did not question the recognition of DTA. This clearly evidences the EP’s non-compliance with the said Accounting Standard.

22. The EP was charged’ with failure to report non-compliance with Division

I of Schedule III of the Act; the shortcomings in this regard are as follows:

(i) Short Term Borrowings which were required to be presented on the face of Balance Sheet are shown in Note no-8 to FS,

(ii) Deferred Tax Assets (DTA) which were required to be classified as Non-Current Assets are classified as Current Assets,

(iii) Cost of materials consumed/Purchase of stock in trade/ Changes in Inventories of finished products/Work in progress and Stock in Trade were to be presented on the face of the Statement of Profit and Loss, but have been shown in Note no-19 to FS,

(iv) Wrong figure of Earning per Share has been reported,

(v) Disclosure about Loans as in Note no-6 to FS is incomplete, as the bifurcation of loan amounts was not mentioned.

(vi) Classification of Short-Term Borrowings at Note 8 to FS has not been given.

(vii) Classification of Short Terms Loans & Advances at Note 15 to FS, has not been given.

22.1 Responding to the charges the EP stated that “(i) Short Term Borrowing of Rs. 1.40 crores was from Aparna Shah as explained to us and what I recollect which was given to Company for payment of Taxes, (ii)Deferred Tax Asset shown under Current Asset. It is a mistake and should have been stated under Non Current Assets, (iii) The nature of business of the Company is of Media content and not manufacturing or Trading in Goods• and hence instead of Material Consumed it has been shown as Operating Cost. However, the details has been given, in the Schedule, (iv) Diluted Earnings per share shown at Rs. 0.53 for 31st March 2016 on the face of Profit & Loss account, However, in the Schedule Note No 25 it has been correctly shown at Rs. 0.45, (v) Terms of Repayment of Loans. Both are car loans as mentioned in the notes and further bifurcation is not given for each of the loan, (vi) Classification of Short Term Borrowings, as already stated earlier the loan was given by Aparna Shah for payment of taxes and (vii) Classification of Short Term loans and Advances Given, were business advances in a day to day business.”

22.2 We find that the EP has accepted his lapse relating to the issues raised in point no (ii), (iv) & (v) above. In respect of point no. (iii), the reply of the EP is accepted. In respect of point no (i), (vi) & (vii), Schedule III of the Act requires a particular presentation of line items of the Balance Sheet and notes to accounts need to indicate the further classifications of such line items. None of these was done and the EP has given evasive replies without addressing the issue of presentation of FS as per the Act.

23. The EP was charged24 with failure to report that Significant Accounting Policies (SAP) of TDML were not as per statutory requirements25; for example, the method of depreciation (Straight Line Method or Written Down Method) was not disclosed. Further, TDML’s SAP on valuation of inventories states ‘Inventories related to films and songs copy rights which is cost production plus relevant overhead cost’, whereas the inventories are required to be valued at lower of cost and net realisable value as per AS 2 and so TDML’s SAP was not as per the AS 2.

23.1 The EP was also charged’ with failure to report that TDML did not comply with its own SAP regarding adopting useful life of assets as prescribed in Schedule II of the Act in respect of Motor Car. The Act prescribed useful life of 8 years for Motor Car, but TDML had considered useful life of Motor Car as 6 years.

23.2 Responding to the charge relating to method of depreciation & valuation of inventories the EP stated that, “The Company had not disclosed the method of depreciation whether on WDV or SLM but in the FA Schedule it has mentioned with the rates clearly indicating it as per the WDV method and the Accounting Policy on Inventory does not show the Net Realizable Value for valuation but in the notes to Accounts for Inventory it is clearly mentioned (lower of cost or net realizable value)”.

23.3 Responding to the charge relating to useful life of assets the EP stated that, “The accounting policy for depreciation for Motor Car provided at 6 years of useful life instead of 8. Which is an error of judgement.”

23.4 The EP has admitted that the company did not disclose the method of depreciation in the SAP and that while accounting for depreciation of the car the useful life taken as 6 years instead of 8 years was an error. As an Auditor the EP should have pointed out these discrepancies, but failed to do so. His explanation that the working in the FA schedule implied that WDV method was used and therefore the company had not disclosed the depreciation method in the SAP is not acceptable. The method of depreciation is required to be specifically disclosed. Further, TDML’s SAP for valuation of inventories gives the impression that inventory is valued at cost of production plus relevant overhead cost whereas, as per AS 2, Inventories are required to be valued at lower of cost and net realisable value. Therefore, it is clear that the EP failed to report non-compliance with SAP of the company and Schedule II of Companies Act, 2013.

24. The EP was charged27 with incorrect reporting as the audit work papers show payment of salary of Rs 25.76 lakhs to Aparna Shah, Director of TDML, while the EP had reported that the company had not paid any managerial remunerations. In Note no-7 to FS relating to Trade Payables there is a reference to ‘Note 2.25’, while in Note no – 22 to the FS relating to Other Expenses, there is a reference to ‘Note 2.28’. However, on perusal, it is seen that there are no notes from 2.14 to 2.28 in the FS. Further, no work paper is available in the Audit File in support of Audit Report issued as per the Companies (Auditor’s Report) Order, 2016 (CARO) for important items like fixed assets, inventories, loans & advances etc.

24.1 Responding to the charges the EP stated that, “The salary was paid to Aparna Shah the Director of the Company and it has been part of our working paper, there is an error in the audit report the “not” has been inadvertently added in the report. Incomplete reporting: (i) The numbers have been wrongly mentioned, Trade Payable refers to note no 2.25 actually refers to note no. 28 regarding Micro and small enterprises. Similarly, the note 2.28 regarding Auditors remuneration actually refers to note no 31. (ii) Paperwork regarding all other matters as already states were non recoverable from my system due the break up. “

24.2 As per para (xi) of CARO, an Auditor is required to report, “whether managerial remuneration has been paid or provided in accordance with the requisite approvals mandated by the provisions of section 197 read with Schedule V to the Companies Act………” There is no work paper in Audit File that Auditor has performed any audit procedure to comply with the above requirement. The Reply of the EP is not acceptable as resorting to inadvertence further magnifies the negligent attitude of the EP in performing his statutory obligations. The reply of the EP regarding wrong numbering again reflects negligence both on the part of the preparer of the accounts and the auditor. Reliance of the EP regarding System breakdown is not acceptable as already discussed earlier.

25. The EP was charged’ with failure to report TDML’s non-compliance with Accounting Standards AS 15 ‘Employee Benefits’ in respect of recognition of expense for retirement benefits. TDML disclosed the fact of nonrecognition of retirement benefits but did not disclose the reason for this deviation from AS 15 and its financial effect as required under section 129(5) of the Act.

25.1 Responding to the charges the EP stated that, “(a) As far as the AS 15 regarding the retirement benefits, the Company had not given any details and hence it has been qualified to that extent. It was explained to us that since none of employees had completed more than 5 year the retirement benefits were not applicable to them. Since it was oral discussion the same has not been put in the audit report.”

25.2 The reply of the EP does not justify non-disclosure of the reason for non-compliance with AS 15 and its financial effect. Besides, verbal explanations or oral discussions cannot be the reason for non disclosure in the Independent Auditor’s Report.

26. As discussed, the EP has made a series of serious departures from the Standards and the Law, in conduct of the audit of TDML for FY 2016-17. Based on above discussion, it is proved that EP had issued unmodified opinion on the Financial Statements without any basis. The poor quality of Audit followed by the cover up in terms of Cash Flow Statement that did not exist at the time of Audit, incomplete documentation and attempt to mislead through evasive replies further compounds the professional misconduct on the part of the EP. Based on the discussion and analysis, we conclude that the EP has committed Professional Misconduct as defined in the Act, as below:

i. CA Rajiv Bengali committed professional misconduct as defined by Section 132 (4) of the Companies Act, read with section 22 and clause 5 of Part I of the Second Schedule of the Chartered Accountants Act 1949 (no. 38 of 1949) as amended from time to time, which states that an EP is guilty of professional misconduct when he “fails to disclose a material fact known to him which is not disclosed in a financial statement, but disclosure of which is necessary in making such financial statement where he is concerned with that financial statement in a professional capacity”.

This charge is proved as the EP failed to disclose in his report the material non-compliances the Company made as explained in para no. 11, 13, 15, 16, 17, 20, 21, 22 (except point no. iii), 23, 24 and 25 above.

ii. CA Rajiv Bengali committed professional misconduct as defined by Section 132 (4) of the Companies Act, read with section 22 and clause 6 of Part I of the Second Schedule of the Chartered Accountants Act 1949 (no. 38 of 1949) as amended from time to time, which states that an EP is guilty of professional misconduct when he “fails to report a material misstatement known to him to appear in a financial statement with which he is concerned in a professional capacity”.

This charge is proved as the EP failed to disclose in his report the material misstatements made by the Company as explained in para no. 15, 16, 17, 20, 21, 22 (except point no. iii), 23, 24 and 25 above.

iii. CA Rajiv Bengali committed professional misconduct as defined by Section 132 (4) of the Companies Act, read with section 22 and clause 7 of Part I of the Second Schedule of the Chartered Accountants Act 1949 (no. 38 of 1949) as amended from time to time, which states that an EP is guilty of professional misconduct when he “does not exercise due diligence or is grossly negligent in the conduct of his professional duties”.

This charge is proved as the EP failed to conduct the audit in accordance with the SAs and applicable regulations, failed to report the material misstatements in the financial statements and failed to report non-compliances made by the Company, as explained in para no. 11 to 25 (except point no. iii of para 22) above.

iv. CA Rajiv Bengali committed professional misconduct as defined by Section 132 (4) of the Companies Act, read with section 22 and clause 8 of Part I of the Second Schedule of the Chartered Accountants Act 1949 (no. 38 of 1949) as amended from time to time, which states that an EP is guilty of professional misconduct when he “fails to obtain sufficient information which is necessary for expression of an opinion or its exceptions are sufficiently material to negate the expression of an opinion”.

This charge is proved as the EP failed to conduct the audit in accordance with the SAs and applicable regulations as well as due to his total failure to report the material misstatements and non-compliances made by the Company in the financial statements, as explained in the para no. 11, 13 to 17, 19, 20, 21, 24 and 25 above.

v. CA Rajiv Bengali committed professional misconduct as defined by Section 132 (4) of the Companies Act, read with section 22 and clause 9 of Part I of the Second Schedule of the Chartered Accountants Act 1949 (no. 38 of 1949) as amended from time to time, which states that an EP is guilty of professional misconduct when he “fails to invite attention to any material departure from the generally accepted procedure of audit applicable to the circumstances”.

This charge is proved since the EP failed to conduct the audit in accordance with the SAs (as explained in para no. 11 to 25 (except point no. iii of para 22) above but falsely reported in his audit report that the audit was conducted as per SAs.

Therefore, we conclude that all the charges (except point no. iii of para 22) of professional misconduct in the SCN stand proved based on the evidence in the Audit File, the Audit Report dated 30th May 2017 issued by the EP, the submissions made by the CA, and the Annual Report of TDML for the FY 2016-17.

D. PENALTY

27. Section 132(4) of the Companies Act, 2013 provides for penalties in a case where professional misconduct is proved. The seriousness with which proved cases of professional misconduct are viewed, is evident from the fact that a minimum punishment is laid down by the law.

28. Independent Auditors of Public Listed Companies serve a critical public function of enabling the users of Audited Financial Statements to take informed decisions.

29. Absent a robust System of Auditing, Investors, Creditors and Other Users of Financial Statements would be handicapped and their work compromised. The best of systems fails, if the professionals implementing the system do not perform their job. This could lead to a serious failure of the financial system which could ultimately result in a breakdown in trust and confidence of investors and the public at large.

30. Thus, the auditor is duty bound to examine and ascertain the integrity of Financial Statements of such entities29 in larger public interest.

31. The EP in the present case was required to ensure compliance with SAs to achieve the necessary audit quality and lend credibility to Financial Statements to facilitate its users. As detailed in this order, substantial deficiencies in Audit, abdication of responsibility and inappropriate conclusions on the part of CA Rajiv Bengali establish his professional misconduct. Despite being a qualified professional, CA Rajiv Bengali has not adhered to the Standards and has thus not discharged the duty cast upon him. Under the circumstances, we proceed to order the following sanctions keeping in mind deterrence, proportionality, and the signalling value of sanctions.

SANCTIONS

32. Considering the fact that professional misconducts have been proved and considering the nature of violations and principles of proportionality, we, in exercise of powers under Section 132(4)(c) of the Companies Act, 2013, order:

(i) Imposition of a monetary penalty of Rs Five Lakhs upon CA Rajiv Bengali.

(ii) In addition, CA Rajiv Bengali is debarred for Five years from being appointed as an auditor or internal auditor or from undertaking any audit in respect of financial statements or internal audit of the functions and activities of any company or body corporate.

33. This order will become effective after 30 days from the date of issue of this order.

Signed

(Dr Ajay Bhushan Prasad Pandey)

Chairperson

Signed

(Praveen Kumar Tiwari)

Full-Time Member

Signed

(Smita Jhingran)

Full-Time Member

Authorised for issue by the National Financial Reporting Authority,

(Vidhu Sood)

Secretary

Date: 19.09.2022

Place: New Delhi

To,

CA Rajiv Bengali,

ICAI Membership No-043998,

M/s Subramaniam Bengali and Associates, Chartered Accountants,

Firm registration no-127499W,

404, The Summit Business Park, M. V. Road,

Adj. to WEH Metro Station. Andheri (East),

Mumbai-400093. (Maharashtra)

Email: rajiv@bengali-ca.com

Copy To: –

(i) Secretary, Ministry of Corporate Affairs, Government of India, New Delhi.

(ii) Securities and Exchange Board of India, Mumbai.

(iii) Registrar of Companies, Mumbai.

(iv) Secretary, Institute of Chartered Accountants of India, New Delhi.

(v) Trilogic Digital Media Limited, Mumbai.

(vi) IT-Team, NFRA for uploading the order on the website of NFRA.

Notes:-

1 At para no 3.1 of SCN

2 At para no 3.2 of SCN

3 At para no 3.3 of SCN

4 Consequent upon demonetization, GSR-308-E dated 30.03.2017, inserted a new clause for disclosure of Specified Bank Notes in division I of schedule III of the Act.

5 At para no 3.4 of SCN

6 As per para 82 of Standard on Quality Control-1 and para A23 of SA 230-Audit Documentation.

7 SA 700 – Forming An Opinion And Reporting On Financial Statements

8At para 4.2 of SCN

9 Para 4.2, 8 and 12 of AS 5- “Net Profit or Loss for the period, Prior period items and changes in accounting policies”

10 At para 4.4 of SCN

11 Para 5 & 7 of SA 450- Evaluation of misstatements identified during the audit.

12 As per para 32 (c) of SA 240.

13 As per para 15 of SA 200- ‘Overall objectives of the Independent Auditor and the conduct of an audit in accordance with Standards on Auditing’, EP was required to plan and perform an audit with professional skepticism recognising that circumstances may exist that cause the financial statements to be materially misstated.

14 At para 4.1 of SCN

15 At para 4.3 of SCN

16 SA 550-Related Parties

17 Para 21 & 23 of AS 18 — Related Party Disclosures

18 At para 4.5 of SCN

19At para 4.7 of SCN

20Section 134(1) and 203 of the Act read with Rule 8 of Companies (appointment and remuneration of Managerial Personnel), Rules 2014.

21 At para 5.2 of the SCN.

22 At para 5.1 of SCN

23 At para 5.3 of the SCN

24 At para 5.4 of the SCN

25 Please refer schedule II of the Act, para 29 of AS-6 ‘Depreciation Accounting’ and para 2 of AS-2 ‘Valuation of Inventories’.

26 At para 5.5 of the SCN

27 At para 5.6 of the SCN

28 At para 5.7 of the SCN

29 As defined in Rule 3 of NFRA Rules 2018

Author Bio