Now a day there is a craze in the market for IPO among startups, companies of scale, medium-sized enterprises. In most of the cases entrepreneur not even know how much their company is prepared for an IPO , how much cost and preparations required for going in Public , they just assume that IPO is an easy way to raise funds for their company and after raising funds they can uses funds as per own and not answerable to banks or any financial institutions just like Debts. Company management not even considers whether is it feasible, how much their organization is ready to go for public issue.

When planning to take your company public, it is important to understand investor sentiments for the brand/ company and create the right pitch that is attractive and valuable for all proposed stakeholders. Then comes conducting due diligence and drafting of a proper road map on handling all the incremental compliance requirements that come post the IPO. One should remember that there will be new responsibilities and restrictions that may come for the management post IPO, and this need a proper assessment before going for Public issue.There is significant difference in handling public and private companies.

Share price of a public company is exposed to the stock market fluctuations

After a company listed in stock exchanges there are many external market factors which can plunge share price regardless of how well the company is managed, In order to minimize the influence of such unfavorable events on a public company’s share price, the management should make constant touch with the market and investors, keeping them informed about the company’s current developments and prospects.

Loss of Autonomous Control over the Company

In a private company, the shareholders have autonomous control over the business and its operations. However, once the company goes public, this control is lost. After Public issue, owners of a formerly private business are no longer allowed the same autonomy in making strategic decisions. All influence up to a certain extent gets transferred to New Public shareholders.

Wide-ranging disclosure requirements and financial reporting

After an IPO, A company compulsorily has to disclose all financial information and provides periodic financial reporting while it is not required for a Pvt ltd company. For example, a public company must have to disclose the names of its ultimate beneficiaries, provide detailed information about the financial position and development plans, disclose remuneration of the directors, and other relevant information.

Substantial investment in the IPO process

Aggregate investment in the IPO process on a leading stock exchange may be quite costly. Though most of these expenses will be reimbursed from the funds raised during the IPO and does not impact the operating results of the company but most of the cost incurred for preparation an IPO will have to be funded by the company’s own resources before the IPO takes place. Thus it is necessary to plan the investments into the IPO process carefully.

New responsibilities and restrictions for the management

After a company going public, activities of the directors and top management of public companies are more regulated and require additional attention. The directors and executives of a public company face certain restrictions related to dealings with the company shares and disclosures of the market-sensitive information etc.

Extensive Regulations

There are many laws that regulate the running of public company. The company will be required to follow extensive internal compliance procedures, file financial reports, accept financial performance audits by independent third parties and comply with operating rules that did not exist when the company was a private or closely owned enterprise. Companies planning to issue securities in India have to comply with provisions of following acts:-

a. Securities Contracts (Regulation) Act, 1956;

b. Securities Contracts (Regulation) Rules, 1957;

c. Companies Act, 2013;

d. The Companies (Prospectus and Allotment of Securities) Rules, 2014;

e. Securities and Exchange Board of India Act, 1992; and

f. Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009

Detailed Planning for IPO

When the company decides to go for IPO, it must build the right team to go public; selection of competent lead managers and merchant bankers for its issue is very important steps of IPO. The most important steps while going public are the internal restructuring of the business entity. Companies often do not plan their efficient internal restructuring before their IPOs. It is necessary to restructure to enhance company/ brand/ share valuations, paving the way for easier compliance management in the future, organizing the existing capital structure, and better presentation and transparency in the financial statements.

A company should make SWOT analysis first and assess how much it is prepared for Public Issue. Company should review its Strategic objective, Business Threats. Market size for its product and Services, competitive advantage, growth potential etc. A Company should also check what more preparations are required what will be the cost of Public Issue.

SWOT ANALYSIS

|

Strength |

Weakness |

|

|

| Opportunities | Threats |

|

|

List is illustrative not exhaustive

Strategic objectives of IPO

There are two major reasons for going public: Being able to access capital markets to raise funds and to expedite growth and build up the resources needed to develop a business plan. A company should check whether it is clear on valid strategic Business objectives it wants to achieve upon choosing the IPO route? Is the company ready to take up required steps to present favorable image to prospective investors?

Predictable Business Model

Business predictability and a 10-year-long vision towards developing the company are some of the essential steps a company should have going for an IPO. Once company goes in public, market investors are interested to predictable earnings. So company management should check whether company business model is predictable.

Risk Analysis of Threats from Market Forces

Company should make Risk Analysis and appropriate risk mitigation strategies to ensure minimal impact form any Business threats. In addition to business risk on the operational and financial front, there is risk around compliance like regulatory risk, legal risk, and code of conduct risk, risk around communication and investor relationship and climate and reputational risk. The management must consider transferring the financial impact of this risk and its future ramifications onto risk transfer mechanisms such as IPO Insurance to safeguard their people, profits, and public image. To ensure that companies have the right insurance coverage before launch of IPO, A company should develop its risk profile and present its preparedness before going public.

Big Market of company Product & Services

Company should also consider how big the market it has for its product or service. Bigger the marekt, there will big room to grow and more likely company will make money. The more money company can make the faster company can grow.

Competitive advantage

Consider how much competitive advantage a company have in form of Cost leadership, Product differentiation, Customer relationship management (CRM),Cost focus, Commitment to customers strategy. Similarly what asset one company controls that will afford it more leverage over rivals

Underlying growth potential

Your business needs to be aware of its underlying growth potential. You should have game plan for growth after the IPO, else the markets will respond negatively.

Costs of IPO Issue

The costs of going public can vary widely. Very firstly there are so many processes to make private company into a public one. Company has to develop systems, controls and processes to support the requirements of being a public company. Cost of going public is affected by a number of factors, such as the complexity of the IPO structure, company size and offering proceeds, as well as a company’s readiness to operate as a public company. The costs of public issue can be categorizes in four part : Pre-IPO direct costs, Pre-IPO indirect costs, Post-IPO one-time costs and Post-IPO recurring costs:

|

Pre-IPO direct costs |

Pre-IPO indirect costs |

|

|

| Post-IPO one-time costs | Post-IPO recurring costs |

|

|

While the underwriting fee typically constitutes the largest direct cost that a company incurs as it goes through an IPO, the legal, registration with Stock Exchange filing exchange listing and other miscellaneous costs accounting and tax costs are also consequential and can increase significantly for companies facing additional complexities in preparing for an IPO.

Pre IPO Finance consultancy Fees

Prior to an IPO, a company has to hire a Finance consultant to guide the company what it need to do to be a public company. Most companies currently use two accounting firms: an auditor and an advisory firm. Advisor Firm advises the company on aspects of the going-public process such as taxes, structuring, HR and compensation, requirement to report financial information As required for IPO, Implementing systems and new processes that are going to make you effective as a public company.

Underwriting fee

Underwriting fees are the largest single direct cost associated with an IPO. Fees charged by bankers typically range from 2 to 3 per cent of an issue’s size. Food delivery firm Zomato’s Rs 9,375-crore IPO fetched record fees of Rs 229 cr for I-bankers, which is a sizeable amount for a large-sized offering. Issuers typically have two or three structures for distributing fees, according to experts. A fixed fee is distributed among all bankers handling the IPO mandate. Then there are variable fees, which could vary from transaction to transaction, and is dependent on parameters such as the procurement done by the banks on the institutional and retail/HNI side. Some issuers also keep a discretionary fee, which they pay if they are satisfied by the work put in by bankers.

Legal Fees

Companies working with external counsel and underwriter counsel incur costs for Due diligence on the company’s operations, management and business, Drafting of the Forms and providing other advice related to the offering ,Interactions with the underwriter, their counsel and other matters directly related to the offering ,Advice on other matters related to going public

Accounting

Companies incur accounting costs in working with the auditor and accounting advisor. Such costs are directly attributable to the offering like technical accounting and financial reporting issues, Interactions with underwriter counsel and external company counsel on matters directly related to the offering.

Registrar and transfer agents (RTA) Fees, Joining Fees of Central Depository Services (India) Limited (CDSL) and National Securities Depository Limited (NSDL)

Stock Exchange Listing and Filing Fees

Once the IPO bidding is closed, the company has to submit the final prospectus to both ROC and SEBI. This should contain both the quantum of shares being allotted and the final issue price on which the sale is closed. SEBI verifies the facts disclosed by the company and check for errors, omissions, and discrepancies. Only after SEBI approves the application the company files an application with the stock exchange to offer its securities to the public in the primary market. There are 7 recognized stock exchange listed with SEBI as on Aug 22

BSE Ltd , Calcutta Stock Exchange Ltd, Metropolitan Stock Exchange of India Ltd ,Multi Commodity Exchange of India Ltd, National Commodity & Derivatives Exchange Ltd, Indian Commodity Exchange Limited, National Stock Exchange of India Ltd. Following is the Fee structure with effect from April 01, 2022

|

Listing Fee Structure based on Paid up Capital: |

NSE | BSE |

| Initial Listing Fees | 50,000 | 20,000 |

| annual listing fees upto 100 Cr | 3,00,000 | 3,00,000 |

| 100 to 200 Cr | 3,80,000 | 3,40,000 |

| 200 to 300 cr | 4,90,000 | 4,40,000 |

| 300 to 400 Cr | 5,95,000 | 5,35,000 |

| 400 to 500 Cr | 7,30,000 | 6,55,000 |

| Above 500 Cr to 1000 Cr | Minimum 7,35,000/- and ₹4,800/- for every increase of ₹5 | Minimum 6,60,000/- and 4,320/- for every increase of Rs.5 Cr |

| Above 1000 Cr | Minimum 12,20,000/- and ₹5,125/- for every increase of ₹5 crore | Minimum 10,95,000 Rs. 4,600/- for every increase of Rs. 5 Cr |

Allotment- Expenses:

Application Collection from Banks and Reporting / ASBA Fees

(b) Stationery and Out-of-Pocket Expenses, Mailing and Handling Expenses and NSDL / CDSL Uploading Fees

(c) Listing, Allotment, Dispatch & Basis of Allotment Fees

Statutory Advertising

Before an IPO opens to the public, the company endeavors to create a buzz in the market by roadshows. Over a period of two weeks, the executives and staff of the company will advertise the impending IPO across the country. This is basically a marketing and advertising tactic to attract potential investors.

Printing Charges

It includes cost of printing of Prospectus and Application Forms, filing, printing, and distribution ,Digital and XBRL support

BSE/NSE Software Expenses

Miscellaneous Expenses

Incremental costs

Generally while going public company Management consider the cost of going public but there are so many Indict cost or say incremental/ Additional cost a company has to incur as a Public company. Private companies in general do not invest in systems, people, processes and broader infrastructure , like enterprise resource planning systems, human resources information systems, tax software solutions, cyber security , contract management systems but after IPO Company has to invest or incur such cost being a public company. Besides this there are so many additional regulatory compliance, a company has to do after being pubic. Following are some approximate incremental cost which a company has to incur after going public

- Incremental Audit – 32%

- Public investor relation HR/IT- 22%

- Financial Reporting – 18%

- Legal – 16%

- Regulatory Compliance – 12%

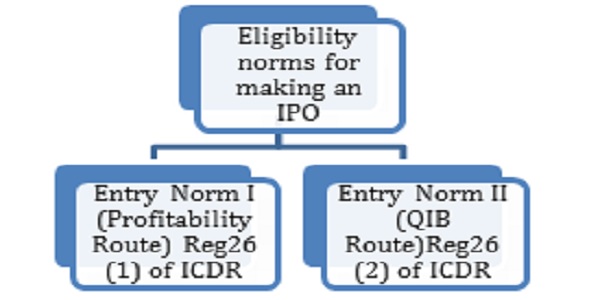

Eligibility norms for making an IPO

As per ICDR Regulations, the companies planning to raise funds through the IPO route have to fulfill the criteria laid down by Securities and Exchange Board of India, the Regulator

Entry norm I (known as Profitability Route)

- Net Tangible assets of > or equal to Rs 3 crores in each of the preceding three years of which not more than 50% are held in monetary assets. This limit is not applicable to 100% for OFS.

- Average EBIT >=Rs 15 crore in three of the preceding five years.

- Net Worth >= 1 crore for the preceding 3 years.

- In case there is a change in the name of the company within the last year, revenue >= 50% from the activity under the new name for the preceding 1 year.

Under this norm, the quota for investors is QIB: 50%, NII: 15%, Retail: 35%.

Entry Norm II (known as QIB route)

To ensure that the genuine companies could raise funds and pave their way for growth, SEBI has provided an alternative route to those who do not satisfy the above criteria. The issue shall be through the book building route, where QIB: 75%, NII: 15%, Retail: 10%. The company shall refund the subscription money if the minimum subscription of QIBs is not attained.

Lock in norms for the Promoter

- Promoter’s 20% of the post-issue capital locked in for 3 years.

- Promoter’s remaining pre-issue capital locked in for 1 year from the listing date.

- Entire non – promoter holding pre-issue capital locked in for 1 year except

- Pre-issue shares allotted to employees under ESOPs or ESPS.

- Venture capital fund, foreign venture capital investor, or alternative investment fund of category I holding shares for at least 1 year from date of purchase.

Restatement / Adjustment of Financial Statement

As per SEBI (ICDR) Regulations, 2018, the financial information should be restated to ensure consistency in the presentation, disclosures, and the accounting policies for all the periods presented in line with that of the latest financial year/Interim period. Such restated financial statements are to be prepared based on the Schedule III of the Companies Act, 2013 for the period of three years including interim period. Where the company has been in existence for a period less than three years, the financial statements are to be given for the actual period of existence

The restated consolidated financial information in the offer document shall not be more than six months old from the date of filing of offer document. If the financial statements for latest full financial year included in the offer document are older than six months from the date of filing of the draft offer document, then issuer company will be required to present a restated consolidated financial information for the interim period. For example, a Company with a March year-end going for an IPO, if the company is filing offer document after 30 September, the company will be required to present financial information for the stub period i.e., period ending 30 September. The restated financial information shall be audited and certified by the statutory auditors

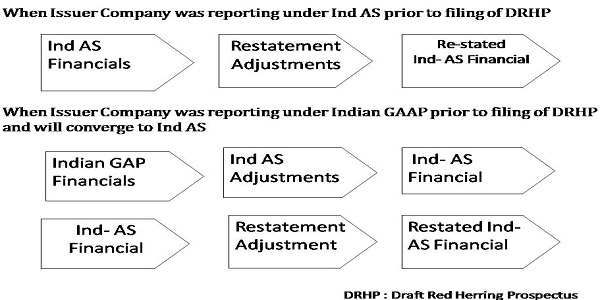

Restatement process.

There are two types of situations that may arise while restating the financials for IPO.

a) Issuer Company was reporting under Ind AS prior to filing of DRHP i.e. Draft Red Hearing Prospectus. In such case company is required to make only restatement adjustments as per ICDR regulations.

b) Issuer Company was reporting under Indian GAAP prior to filing of DRHP and will converge to Ind AS.

Ind AS Adjustments – Impact on Profitability

Certain Ind AS adjustments has an impact on the profitability as well as net worth (equity) of the company. This may have an impact on company valuation which is vital for IPO.

- Certain Ind AS adjustments has an impact on the profitability as well as net worth (equity) of the company. This may have an impact on company valuation which is vital for IPO.

- Promoters and other stakeholders are aware well in advance of the impacts arising due to adoption of Ind AS before an IPO.

- Ind AS financials enhances credibility of the Company from the perspective of the future investors.

- It facilitates comparison of company’s performance with its peers/competitors

Transition to an IPO is not a cheap one. Lawyers, investment bankers, accountants and often outside consultants must be hired. Many cannot even afford the expenses of listing on dedicated and low-cost platforms for SMEs on the Bombay Stock Exchange and the National Stock Exchange. So analysis of cost of IPO is very important steps before going public. Companies that decide to go public are not only faced with enormous opportunities to grow their organization, they also have to deal with so many challenges associated with the transition. As much as a year or more may be required to prepare for an IPO. A poorly timed and poorly planned IPO can end up being extremely detrimental to the company’s financial growth and stability. Private company owners should carefully consider all significant challenges. Lot of planned hard work has to be put in to win the crown when planning to take your company public

Author Bio

Good educative article

please send me a copy vgnath@gmail.com

dr vedula gopinath camping USA