Meaning and significance of EBITDA:

EBITDA means Earnings Before Interest, Taxes, Depreciation and Amortization and is a useful measure of operating performance by allowing evaluation of productivity, efficiency and return on capital, without considering the impacts of interest expenses, asset base, tax expenses, and other operating costs. EBITDA is used by analysts and other professionals to compare companies across and within the same industry.

The most widely used and comparable measure of cash flow is EBITDA as it represents a business’s cash-generating ability before the impact of burden by capital assets, debt and taxes. Therefore, businesses with varying levels of debt, capital assets or even subject to different tax rates may be compared with each other since there are no such impacts on EBITDA.

Meaning and significance of Normalisation of EBITDA:

Normalization of EBITDA is the process of eliminating non-recurring, extraordinary, and irregular or non-core expenses or income which after adjustments represent the future earning capacity which may be expected from the business by the buyer.

Normalized or Adjusted EBITDA is an effective valuation tool which may prove to be useful during acquisition of a business since it eliminates deviations and irregularities and regularizes historical streams of cash flows.

It is suggested to calculate the EBITDA from the most recent trailing 12 months financial statements. Thereafter, the buyer and seller shall apply several normalizing adjustments and “add-backs” to EBITDA to calculate the Adjusted EBITDA. The adjusted EBITDA represents the earning stream moving forward for the buyer and may reflect certain non-recurring expense items which may be debited in the Income Statement and which may cease after the transaction is closed and may require to be added back to the EBITDA.

It is imperative to determine the underlying earning capability of the business and it is advisable to the buyer to estimate the negative adjustments to historical EBITDA as well, which may be in the nature of new expense items, post acquisition that may reduce the going-forward EBITDA.

Amongst other popular valuation methods to value a business, multiple of the company’s normalized EBITDA is an easy and effective method for valuing a company (i.e. 6x TTM EBITDA). Usually, normalizing EBITDA leads to a higher post acquisition EBITDA by adding back non-recurring and extraordinary expenses and therefore, the sellers and their engaged investment bankers are motivated to obtain such a higher EBITDA which would lead to a higher valuation of business by the EBITDA Multiple method.

On the contrary, the buyers are alert to ensure that such normalization adjustments do not lead to an overstated EBITDA and they do not pay for such value of business which may not be realized in the future. A significant amount of time is invested by the buyer in verifying and scrutinising the normalisation adjustments made by the seller as well, as sifting through books of accounts and forecasted financials to unearth non-recurring income that may reduce the EBITDA and therefore the transaction price.

Formula for EBITDA and Normalised/Adjusted EBITDA:

Standard EBITDA= net income + income tax + interest expense + depreciation and amortization

Normalized EBITDA= Standard EBITDA +/- Adjustments

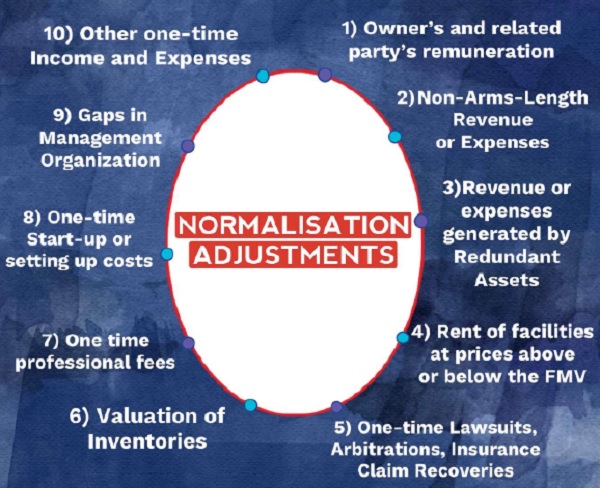

There are few scenarios in which Normalisation of EBITDA becomes imperative and which are as follows:

1) Non-recurring, irregular or one-time income, revenue or expense which is not expected to recur each year.

2) Amounts of income, expense, capital assets, revenue which are not recorded at the fair market value in the financial statements.

3) Overly aggressive or conservative application of an accounting policy or accounting estimate.Below are some of the most common adjustments found in small to mid-size companies grouped under non-recurring and non-core revenues and expenses. These adjustments that are made to EBITDA can vary widely by industry, company, time, and case by case:-

Source: Self

Page Contents

- Detailed analysis of Normalizing Adjustments:

- 1) Owner’s and related party’s remuneration and Compensation:

- 2) Non-Arms-Length Revenue or Expenses:

- 3) Revenue or expenses generated by Redundant Assets:

- 4) Rent of facilities at prices above or below the Fair Market Value:

- 5) Lawsuits, Arbitrations, Insurance Claim Recoveries and One-time disputes:

- 6) Valuation of Inventories:

- 7) One time professional fees:

- 8) One-time Start-up or setting up costs:

- 9) Gaps in Management Organization:

- 10) Other one-time Income and Expenses:

Detailed analysis of Normalizing Adjustments:

A. Business owners, usually of private limited companies, having control over the amount of remuneration to be paid to self, often may remunerate themselves with a higher or a lower salary than as compared to that of an independent third-party manager.

B. Therefore, their remuneration may not be marked-to-market and may reek of owner’s bias since they may provide for a higher remuneration as a tax mitigation strategy in a certain financial year or may provide for a lower salary than fair market value in order to record a higher net income for a certain financial year.

C. Also, the owner may declare extraordinary bonuses at the end of the year to the managerial personnel in order to save income tax for the business entity.

D. Therefore, in order to remove the owner’s bias, the valuer may add back such superfluous or understated remuneration and subtract the remuneration paid to a third-party manager for similar services towards either operational management, intellectual engagement or business development paid in similar organisations in alike circumstances, to the recurring EBITDA to obtain a normalized EBITDA.

E. Specific owner-related business and personal expenses debited to the income statement which may not continue to incur after the business acquisition transaction may be added back to the historical EBITDA. Example of such expenses may be expenses related to personal vehicles, health or life or auto insurance, Keyman Insurance, inordinately high travelling and accommodation expenses, entertainment expenses and club and association memberships.

F. Higher salaries and other remuneration paid to certain family members who may not be actively involved in the operations of the business may be added back and salary of third-party manager at fair market value or at a market-based salary may be subtracted to obtain the recurring EBITDA.

G. Such owner-related expenses may not be eliminated in such circumstances when the potential buyer is anticipating a replacement of the owner who may require similar services, perquisites or other benefits valued similarly.

2) Non-Arms-Length Revenue or Expenses:

A. Such revenue or expenses are a result of related party transactions of the business entity with its related parties at a price which is higher or lower than the market rates and requires modification in the historical EBITDA by eliminating such revenue or expenses and taking into consideration such revenues or expenses which are at Arms-Length pricing and are between two unrelated and independent parties.

B. Few examples of sales or expenses that are not at an arm’s-length transaction are (a) Related entities selling products or services to each other at marked-up rates and/or (b) Cross use of employees at no or inadequate remuneration which is not in tandem with the market rates of similar labour input.

C. In case the company under valuation is a subsidiary company of a holding company and majority of its sales are made to its holding company at non-arm’s length pricing which may for instance be at a higher rate than the market rate, then the valuer is required to normalize the EBITDA by eliminating the effect of such inflated profit due to such inflated sales to a related party and instead ensure that EBITDA reflects the fair market value of these supplies, when the subsidiary company goes up for sale.

D. In case the company under valuation, purchases supplies from a supplier company in which a director of the former company is interested or a major shareholder and the purchases are made at a price higher than the market value, then the valuer is required to normalize the EBITDA by eliminating the effect of such understated profit due to such inflated purchases from a related party and instead ensure that EBITDA reflects the fair market value of these supplies, when the said company goes up for sale.

E. There may be certain rebates or discounts of which the benefits may not pass on to a new owner and such transactions may also be categorised as at being at non-arm’s-length and the valuer should consider reducing such amounts from the historical EBITDA.

F. In case there is synergistic value by virtue of the nature of the transaction itself, then the transaction may not be considered marked-to market, for example say, there may be synergistic value created in certain purchase transactions between a research-based pharmaceuticals company and a retail-based pharmaceuticals company and the same may not be considered to be at market price, then the valuer may have to consider normalizing the EBITDA in case one of the companies goes up for sale but not with the other company.

3) Revenue or expenses generated by Redundant Assets:

A. Expenses incurred on redundant assets or non-productive assets i.e. assets owned by the company that don’t contribute to revenue-generating activities or towards the operation of the business, may be added back to the historical EBITDA to normalize the recurring EBITDA.

B. Income from redundant assets or non-productive assets i.e. assets owned by the company that don’t contribute to revenue-generating activities or towards the operation of the business, are subtracted from the historical EBITDA to normalize the recurring EBITDA.

C. Say for example, a guest house is maintained for the use and welfare of the employees of the company and such use was provided as an incentive for good performance of such employees or such a guest house was excessively used during COVID times. Since, the guest house is not directly related to the operation of the business and therefore, expenses incurred on its maintenance may be added back to the EBITDA to normalize it.

D. Say for example, a company has 4 manufacturing units and one of it becomes redundant or non-operational due to any reason, then expenses incurred on maintaining the redundant unit may be added back to the EBITDA to normalize it since no corresponding revenue from such a unit may be estimated in the future.

4) Rent of facilities at prices above or below the Fair Market Value:

A. The seller may own real estate properties in a separate legal entity and may have an existing lease/rental contract with the company under valuation, wherein the latter company may be paying rent above or below the market rent and necessary adjustments are required to be carried out in the historical EBITDA to reflect the fair market rent level.

B. Say for example, in case the office property is given out on rent by the owner-director of a company or the shareholder-director of its holding company and such rent amount is higher than the market rates of rent of similar properties in similar location, then upward adjustments may be required in EBITDA by adding back the arbitrary and non-arm’s length rent and reducing the true market rent.

C. Say for example, usually Public Sector Undertakings (PSUs) maintain offices occupied on rent which may be much lower than the market value of rent of similar commercial properties in the same location. Therefore, the EBITDA may be normalized by subtracting the market rent and adding back the actual lower rent. Additionally, the valuer may have to review such rental/lease contracts for the expiry period and other clauses too.

D. In case a real estate property is owned by the business entity and is redundant or does not contribute to the core-operations of the business or is not critical to the operations and the buyer doesn’t intend to avail the property, then related expenses such as insurance, maintenance and property tax and any rental income are required to be removed from the historical EBITDA.

5) Lawsuits, Arbitrations, Insurance Claim Recoveries and One-time disputes:

A) In case the entity is undergoing any one-time or inordinately high and unusual lawsuit which shall not recur in the future, then, it would be appropriate to add back such expenses to the historical EBITDA. It is pertinent to note that regular ongoing legal expenses for which provisioning has been made shall not be considered to be added back to EBITDA.

B) Say for example, making provisions for the expected credit loss on trade receivables is a regular exercise and may not be considered as a one-time event. However, in regard to any extraordinary income or expense in the nature of lawsuits, arbitrations, Insurance Claim recoveries and one-time disputes that may have been settled during the review period and may not recur may require either adding back or subtracting, as the case may be, from EBITDA to normalize it.

C) In case of an insurance recovery on the death of the managing director by virtue of a Keyman Insurance policy undertaken by the company or insurance claim recovery on loss of stocks due to cyclone or insurance recovery on demolition of immovable property due to any natural calamity, such extraordinary incomes would be deducted from EBITDA to normalize it.

6) Valuation of Inventories:

A. During Covid-19 times, the demand for certain FMCG goods had spiked and the suppliers maintained multiple times of the volume of stock to meet the increase in demand, however as soon as the lockdowns were lifted, the demand regularized and the fast movement of stock that lasted for a brief period regularized and resulted in piling up of high volume of closing stock for such suppliers. Therefore, normalization in stock may be required in case of non-recurrent spells of such unexpected stock movement due to unavoidable factors.

B. In certain cases, due to the innate nature of the inventory, the value of the inventory may rise or fall substantially, which may affect the valuation of the business as is in the case of jewellery, gold and other precious metals and stones inventory for jewellers and in computing the normalized EBITDA, the valuer may have to take into consideration the future forecasted prices of such precious metals during the forecasted period and may consider the same to ensure relevant valuation of business.

C. In case the business requires equipments to provide services which shall further require the purchase of parts and components throughout the year. Usually, an estimated general allowance is provided to meet the expenditure of such parts and components and in case the value of such parts exceeds such an allowance provided, then it may be advisable to value this inventory close to the date of selling of business. Also, any excess amount of value of such parts over and above the general allowance may be added back to EBITDA to normalize it.

D. The management should identify the value of slow-moving inventory or obsolete inventory which is required to be written off or sold as scrap. The valuer should ensure normalization in inventory by eliminating such type of stock from the closing balance of inventory so that the valuation of business is not affected.

7) One time professional fees:

A. There may be one-time professional fees paid in regard to setting up a new service vertical or a business unit or a branch and additionally other related costs may be incurred such as research and development costs, marketing costs, training costs and other setting up costs, which are non-recurring in nature and are specific to the new service vertical. Such non-recurring expenses should be added back to the EBITDA to normalize it.

B. In case the business is currently subject to the exposure of a one-time or inordinately and unusually high amount of payout due to a lawsuit which further involves the payout of a non-recurring third-party professional legal fees, consulting fees, accounting fees and/or engineering fees, then such amounts of professional fees should be considered to be added back to the historical EBITDA.

C. However, regular legal expenses which is a part and parcel of the operation of the business and for which a provision may also have been created, would not be considered to be added back to EBITDA since such expenses are due to the innate nature of the business and shall be expected to be continued in the future as well.

D. Once the buyout transaction goes through, the buyer’s existing support infrastructure including the accounting department, engineering staff, legal staff, Human Resource department or other professional departments would continue and such professional third-party expenses for similar services would no longer be required to be incurred, therefore, such expenses are to be added back to the Historical EBITDA.

E. One-time professional fees may be required for the set-up of family trusts, HUFs, entity restructuring or insurance claims and since such expenses are non-recurring in nature are to be considered to be added back or subtracted, as the case may be, to the Historical EBITDA.

8) One-time Start-up or setting up costs:

A. Such start-up costs and related setting up costs are non-recurring and considered sunk costs that will not be incurred going forward and in case the same has been incurred in relation to the launch of a new business vertical in the same period, then it should be added back to the historical EBITDA.

B. Say for Example, in case of valuation of Swiggy wherein the core business model is that of food delivery but recently Swiggy has started a new service vertical of grocery delivery named Swiggy Instamart. While considering the historical results of Swiggy, the set-up costs and other associated costs in regard to the new vertical being a one-time expenditure which shall not recur, may be added back to the historical EBITDA for its normalization, unless the incidence of introduction of new service verticals is frequent.

9) Gaps in Management Organization:

A. In case the organisation is primarily owner-driven or post acquisition by the buyer, existing key managerial personnel may exit the organisation and the buyer may require to hire new talent to fill the gaps in the top line and the functional level of the management. There would likely be a negative adjustment to EBITDA for remuneration, benefits and other items related to the new hires.

B. Also, a simple bookkeeper may be required to be replaced with a more experienced financial executive or a virtual CFO, financial controller or a Chartered Accountant as per the growing requirement of the organisation by the buyer and such additional remuneration may have a negative impact on the historical EBITDA.

10) Other one-time Income and Expenses:

A. Discretionary extraordinary nature of income or expenses which are non-recurring may be classified in this category such as record one-time employee bonuses or special donation expenses which should be considered to be added back to EBITDA to normalize it.

B. In case of excessive amount or a meagre amount of repair and maintenance expenses have been incurred in certain years, then forecasting of adequate amount of repair and maintenance costs should be made with regard to the age and condition of the fixed assets which shall be incurred in the future.

C. In certain cases, business owners may have aggressively expensed the purchase price of capital assets instead of capitalizing the same and to claim depreciation expense over time on the balance sheet. The valuer should ensure that the historical EBITDA has not been negatively impacted by such accounting practice of the seller.

D. The valuer should evaluate and be aware of other extraordinary items such as changes in amount of upcoming insurance (positive or negative), upcoming wage rates increases (negative), fire, cyclone or other natural disasters that have caused one-time expenses for repair or reconstruction (positive), a one-time major building renovation or repair cost (positive), non-IND-AS or non-Indian GAAP or unusual accounting practices adopted by the seller (positive or negative), and deferred capital expenditures/maintenance on equipment (negative).

E. Additionally the valuer should be alert and sift out other non-recurring and one-time expenses such as loss due to fraud, misfeasance, theft or siphoning off funds, loss caused due to labour strike or lockouts, unusual amount of gain or losses on disposal of assets, one-time movement and relocation of office expenses, extraordinary human resource related expenses such as CEO recruitment fees or severance package costs of other KMPs, goodwill impairment, and unusual gain or loss due to Foreign Exchange fluctuations and carry out necessary normalization adjustments to the historical EBITDA.

The process of Normalization of historical EBITDA may be illustrated using the following example:

| S.No | Particulars | Effect on EBITDA | Amount (in Rs.) |

| Historical EBITDA | 10,50,75,250 | ||

| a) | Incremental remuneration paid to owner versus marked-to-market remuneration of third-party manager i.e. adjustment for owner’s bias | (+) | 15,75,000 |

| b) | Incremental remuneration paid to inactive owner’s relatives versus marked-to-market remuneration of similar third-party manager i.e. adjustment for owner’s bias | (+) | 6,45,000 |

| c) | Inordinately high owner-specific expenses including health, auto and life insurance, club memberships and travelling expenses not to be incurred post acquisition transaction by the buyer. | (+) | 7,15,000 |

| d) | Incremental income due to related party transactions at Non-Arms-Length prices. | (-) | 25,75,000 |

| e) | Remuneration not charged to group entities on cross-use of manpower services | (+) | 5,85,000 |

| f) | Expenses incurred on Redundant Assets | (+) | 5,25,000 |

| g) | Incremental rental expenditure due to Rent of facilities at prices above the Fair Market Value | (+) | 8,85,000 |

| h) | Lawsuits, Arbitrations and One-time disputes | (+) | 12,45,250 |

| i) | One-time professional fees | (+) | 3,50,000 |

| j) | One-time Start-up or setting up costs | (+) | 17,89,000 |

| k) | Remuneration of new key managerial personnel hired to fill the role of the owner | (-) | 25,85,000 |

| l) | One-time extraordinary bonus to KMPs | (+) | 7,75,000 |

| m) | Loss on damage to P&M due to Amphan cyclone | (+) | 4,25,000 |

| n) | Non-recurring Insurance claim received on loss of inventory due to fire- breakout | (-) | 2,50,000 |

| o) | One-time Special donation expense | (+) | 1,50,000 |

| p) | Expensing of acquisition of fixed asset instead of capitalization

(Adjustment net of depreciation) |

(+) | 12,75,000 |

| q) | Loss due to non-recurring fraud and misfeasance by company staff | (+) | 3,50,000 |

| r) | Unusual gain on disposal of fixed asset | (-) | 4,50,000 |

| s) | EBITDA overstated due to adoption of inappropriate accounting policies and practices now adjusted | (-) | 3,65,000 |

| t) | One-time expenses on relocation of registered office | (+) | 4,25,000 |

| u) | Unusual gain due to foreign exchange fluctuations. | (-) | 6,45,000 |

| v) | No requirement of expenses of third-party professional services due to presence of buyer’s support infrastructure. | (+) | 9,65,000 |

| Normalized EBITDA | 11,08,84,500 |

Source: Self

In case the Registered Valuer adopts EBITDA multiple of 8x as the valuation methodology, then it is notable that the Valuation of the business, considering Standard EBITDA before normalization adjustments, is Rs. 84,06,02,000 and the Valuation of the business, considering Adjusted/Normalized EBITDA after normalization adjustments, is Rs. 88,70,76,000. The incremental EBITDA due to normalization adjustments is Rs. 58,09,250 and therefore, an amount of Rs. 4,64,74,000 (i.e. Rs. 58,09,250 x 8) is to be paid more by the buyer since the valuer while adopting any valuation methodology including the EBITDA multiple method of relative valuation of business, would consider the parameter of Normalized EBITDA instead of Standard EBITDA being more reflective of the true value of the business.

Disclaimer: The contents of this article are for information purposes only and does not form an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc. before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

Author Bio