There are many start-ups in India who begin their journey as Limited Liability Partnership (LLP). LLP is majorly suitable for Service sectors, Professionals, Start-ups, Small Businesses, where the liability in business remains LIMITED. It is also a recommended form of business for people who want to have lesser of annual compliances and annual audit expenses and who do not want to raise funds from any Investor in the initial phase. Partners of an LLP do not face any restrictions on withdrawing capital /profit from the firm. Whereas Shareholders of a company have to follow the laws to withdraw their money. Conversely, LLP attracts a higher income tax rate of 30% as against a company which is taxed at 22%. For bigger and capital-intensive businesses Company form start up is suitable, who can easily get fundings from banks and investors. Corporatization has become the need of the current market situation. Hence there are many start-ups stepping into company form of business. One such conversion is LLP into a Private Limited Company. This article briefs on the steps involved in the same.

PRE – CONDITION FOR CONVERSION:

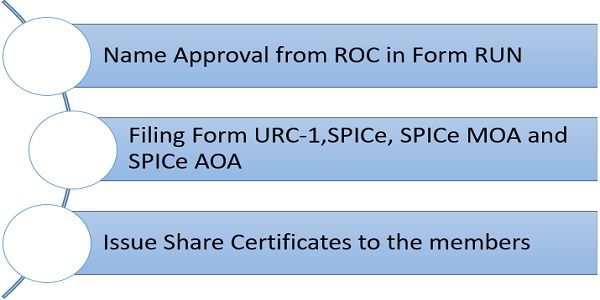

STEPS IN CONVERSION:

ATTACHMENTS TO URC – 1

1. List of the members with details viz. names, address, occupation, shares held by them appropriately, etc.

2. List of the first directors of the private company with details viz. names, address, the DIN etc.

3. An affidavit from every person proposed as first directors, that he is not banned to be a director under section-164

4. A list including the names & addresses of partners of LLP

5. A copy of LLP agreement & certificate of registration duly verified by two designated partners

6. A statement indicating the following specifications q) the nominal share capital of firm & the number of shares into which it is separated b) the number of shares taken & the amount paid for every share c) the name of the firm, with the addition of word Limited or private limited is required.

7. A written consent of all partners of LLP

8. A written consent or No objection certificate from all creditors.

9. Copy of newspaper advertisement,

10. Statement of accounts of the company which must not be 30 days preceding the date of the application and it must be duly certified by the auditor.

11. A copy of latest income tax return

12. Undertaking by proposed first directors with regard to compliance with Stamp Act

ATTACHMENTS TO SPICe Form

1. Consent & Declaration by first Directors in form DIR-2; (On Plain Paper)

2. Self-Declaration by first directors and subscribers in form INC-9; (On Plain Paper)

3. ID Proof and Address Proof of Directors; (PAN card and Aadhar card)

4. Resolution of Partners for conversion of LLP into Company;

5. Proof of regd. Office like Rent Agreement/Sale deed

6. Latest Electricity bill (Not older than 2 Months)

7. NOC of Owner of Office, If Regd office is rented

TAX IMPLICATIONS:

Following Conditions specified in Income Tax to be followed for the transaction of transfer from Firm to Pvt Ltd Co. to not attract capital gain tax:-

(a) all the assets and liabilities of the firm or of the association of persons or body of individuals relating to the business immediately before the succession become the assets and liabilities of the company;

(b) all the partners of the firm immediately before the succession become the shareholders of the company in the same proportion in which their capital accounts stood in the books of the firm on the date of the succession;

(c) the partners of the firm do not receive any consideration or benefit, directly or indirectly, in any form or manner, other than by way of allotment of shares in the company; and

(d the aggregate of the shareholding in the company of the partners of the firm is not less than fifty per cent of the total voting power in the company and their shareholding continues to be as such for a period of five years from the date of the succession;

(e) he demutualization or corporatization of a recognized stock exchange in India is carried out in accordance with a scheme for demutualization or corporatization which is approved by the Securities and Exchange Board of India established under section 3 of the Securities and Exchange Board of India Act, 1992 (15 of 1992);

STEPS AFTER CONVERSION:

1. Secured Loans

NOC from Bankers & New Sanction Letter required for the same of Pvt Ltd (Ask Banker about expenses)

2. Unsecured Loans

Loan from other than Director’s and relative cannot be transferred to company. (These loans to be routed through Individuals)

3. New PAN/TAN/GST/PT/ESIC/IEC Code and any other statutory registration and vendor registration

4. To ask labour consultant about transfer of employee to new company

5. All Assets to be transferred to New company at Book Value

6. Approx, Expenses on Formation of New company like ROC Fees & Stamp Duty on Authorized Capital

| Authorised Capital | 1 CR | 2 CR |

| MOA | 2,04,000.00 | 2,79,000.00 |

| Stamp Duty | 20,000.00 | 40,000.00 |

| Total | 2,24,000.00 | 3,19,000.00 |

Disclaimer:-

The above note is only for reference purpose, you shall consult a tax professional for advice on same. For any queries the author can be reached at vaibhav.chheda8@gmail.com

Author Bio