TYPES OF BUSINESS REGISTRATION

-Sole Proprietorship Registration

-Partnership Firm Registration

-Limited Liability Partnership Firm

-Company Registration

COMPANY DEFINITION

A company is essentially an artificial person—also known as corporate personhood—in that it is an entity separate from the individuals who own, manage, and support its operations. Companies are generally organized to earn a profit from business activities, though some may be structured as nonprofit charities

TYPES OF COMPANIES

- Companies Limited by Shares

- Companies Limited by Guarantee

- Unlimited Companies

- One Person Companies (OPC)

- Private Companies

- Public Companies

- Holding and Subsidiary Companies

- Associate Companies

- Government Companies

- Foreign Companies

- Charitable Companies (section 8 companies)

- Dormant Companies

- Nidhi Companies

WHY REGISTRATION OF COMPANY REQUIRED

- Limited liability protection:

- Any business is prone to incur a loss and one of the main advantages of registration is that it offers limited liability protection and hence the business promoters are not liable for the liabilities of the business. There is no way of losing personal property.

- Secure funding

- In order to move your business forward, seeking and securing investment cannot be missed out. Funding could be in the form of debt or equity. Company incorporation facilitates the funding process well and attracts more potential investors. Also, most banks and financial institutions prefer to fund registered entities rather than unregistered entities.

- Brand recognition

- A registered business is the biggest asset and has the prospects of being passed down as an inheritance to generations or it could be sold to new breed entrepreneurs. Registering a business is required for sustainability.

REQUIRED DOCUMENTS TO INCORPORATE COMPANY

1. Name and object of Proposed Company.

2. Self attested PAN card of all applicants

3. Self attested Aadhar card of all applicants

4. Bank statement of all applicants (NOT OLDER THAN 2 MONTHS)

5. Mobile no. and e-mail id of all applicants

6. Color passport size photograph of all applicants

7. Electricity bill For proof of registered office address (NOT OLDER THAN 2 MONTHS)

8. Rent Agreement if property rented

9. Total capital of company and sharing ratio.

10. Education of all applicants.

11. Occupation of all directors. (IF in service then which sector, please specify)

12. Bank name for account opening of company

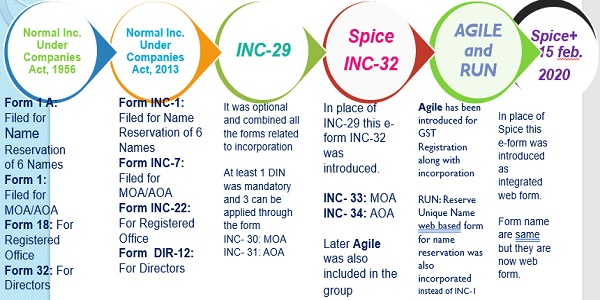

Transformation in Incorporation Process in Last Decade

Simplified Performa for Incorporating Company electronically Plus (SPICe+) is an integrated Web form offering 10 services.

Thereby saving as many procedures, time and cost for Starting a Business in India. SPICe+ is part of various initiatives and commitment of Government of India towards Ease of Doing Business (EODB).

♦ SPICe+ offers a bouquet of services viz.

(i) Incorporation

(ii) DIN allotment

(iii) Mandatory issue of PAN

(iv) Mandatory issue of TAN

(v) Mandatory issue of EPFO registration

(vi) Mandatory issue of ESIC registration

(vii) Mandatory issue of Professional Tax registration (Maharashtra)

(viii) Mandatory Opening of Bank Account for the Company and

(ix) Allotment of GSTIN (if so applied for)

♦ SPICe+ has been divided into two parts viz., SPICe+ Part A and SPICe+ Part B.

- SPICe+ Part A represents the section wherein all details with respect to name reservation for a new company has to be entered.

- SPICe+ Part B represents the section wherein all remaining details required for incorporation of a company has to be entered.

♦ SPICe+ Web form is a post-login service and existing registered applicants would need to login into their account using their credentials. New applicants are required to create a login account first before using the service.

♦ Once the SPICE+ is filled completely, it will be converted into pdf for affixing the DSC.

COMPLIANCES which must be complied by Private Companies under Companies Act, 2013

| MANDATORY COMPLIANCES | EVENT BASED COMPLIANCES |

| Filing Of Form inc-20A | Share Certificate Issuance |

| Appointment of Auditor | Any change in Company’s registered office |

| Board and Annual General Meeting | Any change in Management |

| Preparation of Annual Financial Statements | Any change in business(object)of the Company |

| Filing Annual Return | Any change in capital of the Company |

| Maintaining Statutory Records | |

| Tax Compliance | |

| Statutory Audit | |

| DIR-3 Kyc | |

| DPT-3 Return | |

| MSME Return |

FILING OF FORM INC-20A;

FORM INC – 20A Declaration for Commencement of Business

INC-20A is a mandatory form that is to be filed by a company incorporated on or after 02/11/2018 with MCA. It is also known as Declaration of Commencement of Business. It should be filed by the directors within 180 days from date of incorporation of a company which has share capital.

APPOINTMENT OF AUDITOR (Sec. 139)

According to sec. 139 of Companies Act 2013;-

√ The first auditor of the company shall be appointed by the Board within 30 days of Incorporation & otherwise within 90 days in Extra Ordinary General Meeting.

√ Auditor shall be appointed

√ In case of individual- for not more than 1 term of 5 years and in case of Audit Firm- for not more than 2 terms of 5 years (Applicable for companies prescribed u/s 2 of sec. 139 ).

√ E- Form ADT-1 shall be filed with ROC within 15 days of such appointment.

BOARD AND ANNUAL GENERAL MEETING

According to Companies Act 2013:-

√ First Board Meeting to be held within 30 days of incorporation and at least 4 Board Meeting must be held every year and the time gap between 2 Board Meetings- should not be more than 120 days. Notice of Board Meeting shall be given at least 7 days in advance through electronic mode.

√ Annual General Meeting must be held each year apart from other meetings and the first Annual General Meeting must be held within a period of 9 months from closing of its first financial year otherwise in other cases within the period of 6 months.

FILING OF ANNUAL RETURN

- FORM AOC-4:- Form AOC 4 is an annual return required to be file for filing the company’s financial statement for every financial year with the Registrar of Companies. Hence, Form AOC-4 is submitted with the MCA for each Financial Year within 30 days of a company’s ANNUAL GENERAL MEETING.

- FORM MGT-7A:- Following Companies shall file its annual return in Form MGT-7A from the financial year 2020-2021 and onwards:-

1. One Person Company

2. Small Company

- Small company means a company other than the public company of which paid up capital and turnover shall not exceed rupees two crores and rupees twenty crores respectively.”

- Provided that nothing in this clause shall apply to

(A) A holding company or a subsidiary company;

(B) A company registered under section 8; or

(C) A company or body corporate governed by any special Act.

Now MGT-7 is specifically for companies other than small and OPC. That means the same is required to be certified by CS, unlike MGT-7A (applicable from F.Y. 2020-21)

MAINTAINING STATUTORY RECORDS

♦ Register of the Company

♦ Register of Members (MGT-1)

♦ Register of Debenture-holders (MGT-2)

♦ Register of Directors and Key Managerial Personnel. (no particular format)

♦ Register of Charges. (CHG-7)

♦ Register of Renewed and Duplicate Share Certificates. (SH-2)

♦ Register of Shareholders

♦ Register of Shares/Other Securities Bought Back (SH-10)

DIR-3 KYC (TO KEEP DIRECTOR DIN ACTIVE)’

Every Director who has been allotted DIN on or before the end of the financial year, and whose DIN status is ‘Approved’, would be mandatorily required to file form DIR-3 KYC before 30th September of the immediately next financial year.

After expiry of the respective due dates, system will mark all non-compliant DINs against which DIR-3 KYC form has not been filed as ‘Deactivated due to non-filing of DIR-3 KYC’ and to make DIN active there is requirement to pay fine of Rs. 5000.

DPT-3 RETURN

DPT-3 is annual return which is required to be filed every year by Companies having any amount of loan or advances, not considered as deposits as on 31st March within 90 days of closure of financial year i.e. upto 30th June. Every company except a government company must file this return. Additionally, as per Rule 1(3) of the Companies (Acceptance of Deposits) Rules 2014, the following companies are also exempt:

- Banking company

- Non-Banking Financial Company

- A housing finance company registered with National Housing Bank

MSME RETURN

MSME RETURN:- Every company, who get supplies of goods or services from Micro And Small Enterprises and whose payments to micro and small enterprise suppliers Exceed Forty Five Days from the date of acceptance or the date of deemed acceptance of the goods or services ,shall submit a9 half yearly return to the Ministry of Corporate Affairs stating the following: (b) the reasons of the delay of payment;