Valuation Standards Board

The Institute of Chartered Accountants of India

18th January, 2022

ANNOUNCEMENT

Request to give comments on the Exposure Draft of ICAI Valuation Standard-304 “Valuation of Assets in the Extractive Industries” by 27th January, 2022

The Valuation Standards Board of the Institute of Chartered Accountants of India has been assigned with the task of formulation of Valuation Standards, in relation to the Asset Class – “Securities or Financial Assets”, and also to conceive and suggest areas in which Valuation Standards need to be further developed.

In the year 2018, the Institute of Chartered Accountants of India through its Valuation Standards Board had issued ICAI Valuation Standards 2018, to standardise the various principles, practices and procedures followed by the Valuation Professionals in India.

Taking forward this journey it has been decided to issue Valuation Standards for Valuation in other areas. Accordingly, ICAI Valuation Standard-304 “Valuation of Assets in the Extractive Industries” has been formulated. The Standard prescribes specific guidelines and principles which are applicable to the valuation of assets (including rights or interests) in Extractive Industries and that are not dealt with specifically in any other Valuation Standard.

For wider participation it has been decided to issue an Exposure Draft of the said Standard. Comments are invited on any aspect of this Exposure Draft. Comments are most helpful if they indicate the specific paragraph or group of paragraphs to which they relate, contain a clear rationale and where applicable provide a suggestion for alternative change.

The downloadable version is available at: https://resource.cdn.icai.org/68852vsb-vs304.pdf

Further, comments on the abovementioned Exposure Drafts may be submitted through any of the following modes:

1. Electronically: To submit comments online click on https://forms.gle/rhyFhjwSQpnr12xm9 (Preferred method)

2. Email: Comments can be sent to: commentsvsb@icai.in

3. Postal: Secretary, Valuation Standards Board, The Institute of Chartered Accountants of India, ICAI Bhawan, A-29, Sector–62, 4th Floor, Admin Block Noida – 201309

You are requested to give your suggestions/ inputs on the Exposure Draft latest by 27th January 2022.

Sincerely Yours,

Chairman and Vice Chairman

Valuation Standards Board

The Institute of Chartered Accountants of India

ED/ICAI VS- 304/2021-2022/21

Exposure Draft

of

ICAI Valuation Standard 304

Valuation of Assets in the Extractive Industries

(Last date for Comments: January 27, 2022)

Exposure Draft

ICAI Valuation Standard 304 Valuation of Assets in the Extractive Industries

Following is the Exposure Draft of the ICAI Valuation Standard (ICAI VS) 304 Valuation of Assets in the Extractive Industries issued by the Valuation Standards Board of the Institute of Chartered Accountants of India, for comments.

The Board invites comments on any aspect of this Exposure Draft. Comments are most helpful if they indicate the specific paragraph or group of paragraphs to which they relate, contain a clear rationale and, where applicable, provide a suggestion for alternative wording.

Comments can be submitted using one of the following methods, so as to be received not later than January 27, 2022.

1. Electronically: Click on: https://forms.gle/rhyFhjwSQpnr12xm9 to submit comments online. (Preferred method)

2. Email: Comments can be sent to commentsvsb@icai.in

3. Postal: Secretary, Valuation Standards Board, The Institute of Chartered Accountants of India, ICAI Bhawan, A- 29, Sector- 62, Noida – 203209.

Further clarifications on any aspect of this Exposure Draft may be sought by e-mail to valuationstandards@icai.in.

Exposure Draft

ICAI Valuation Standard [304]

Valuation of Assets in the Extractive Industries

Exposure Draft

ICAI Valuation Standard 304, Valuation of Assets in the Extractive

Industries

The Exposure Draft of the ICAI Valuation Standard includes paragraphs set in bold type and plain type, which have equal authority. Paragraphs in bold type indicate the main principles. (This Exposure Draft of the ICAI Valuation Standard should be read in the context of its Introduction and Framework for the preparation of Valuation Report in accordance with ICAI Valuation Standards)

Objective

1. The objective of this Standard is to prescribe specific guidelines and principles which are applicable to the valuation of assets (including rights or interests) in the Extractive Industries that are not dealt specifically in another Standard.

2. The Standard is not applicable and does not cover the assets downstream (or assets involved in the distribution of products to retailers or fabricators) from the metal refineries or mineral processing plants or petroleum refineries and natural gas processing plants.

3. The importance of valuing assets of Extractive Industries arises from the fact that the reported and intangible form of the said assets may not reflect the true value of the said assets. Unlike valuation of many other industries, valuation of assets in extractive industry is based on depleting mineral assets, the knowledge of which is imperfect prior to the commencement of extraction. It is therefore essential that the valuation incorporates the risks associated with each stage of mining. Certain areas where valuation of assets of Extractive Industries are required are as below:

a. Accounting and financial reporting

b. Transaction purposes

c. Financing

d. Bankruptcy / restructuring

e. Litigation

f. Impairment testing analysis

g. Mergers and Acquisitions

h. Initial Public Offerings

i. Grant or acquisition of Rights

j. Tax computations

4. The principles enunciated in this Standard shall be applied in conjunction with the principles prescribed and contained in the Framework for the Preparation of Valuation Report in accordance with ICAI Valuation Standards.

Scope

5. This Standard shall be applied for valuation of Extractive Industries assets including interests / rights held by entities involved in the Extractive Industries / in natural resource properties including mining industry and petroleum industry but not including activities focused on the extraction of water from earth.

6. Valuation of Extractive Industry assets (including interests / rights) is necessary to assess the availability of capital for supporting the continuity of the said Industry as well as to help in the effective use of Mineral and Petroleum natural resources. Some exploration and evaluation assets are treated as intangibles (e.g. drilling rights), whereas others are considered as tangible (e.g. vehicle and drilling rigs).

7. Valuers and users of valuation are required to make a distinction among real property, personal property, and business interests involved in the stages of ownership, processing and measurement.

8. Valuation of Extractive Industries assets may require placing of reliance on a Technical Expert or accredited specialists specific to the industry.

Definitions and Important Terms

9. Exploration Area or Property: A Mineral or Petroleum real property interest for which the economic viability has not been established but which is being actively explored for Mineral deposits or Petroleum accumulations.

10. Exploration for and evaluation of mineral resources: It is defined as the search for mineral resources, including minerals, oil, natural gas and similar non-regenerative resources after the entity has obtained legal rights to explore in a specific area, as well as the determination of the technical feasibility and commercial viability of extracting the mineral resource. 1

11. Extraction: Deposits of Extractive Industries are generally located in remote locations and are majorly or completely buried below the surface of the land and below the floor of water bodies. The means of production would necessarily be in the form of extraction of natural resources from the earth. Examples of depleting / wasting natural resources are: metallic mineral deposits containing metals such as gold, silver, copper, platinum, iron, etc., non-metallic minerals such as coal, diamonds, gemstones, limestone, salt, etc., construction material like sand, crushed stone, dimension stone, etc. and petroleum deposits such as oil, natural gas and its variants, other gases, etc. Valuable minerals are extracted by mining in a surface mine (Surface mine also includes a quarry used to produce construction material) (open pit, open cut, open cast or strip mine) or an underground mine. Extraction can also be undertaken through wells (in situ leaching of salts and uranium minerals) or dredging the floors of water bodies for resources such as diamonds, alluvial gold, gravel, etc.

12. Extractive Industries: The term “Extractive Industries” refers to the industry engaged in mining operations and the extraction of oil and gas; however, excludes industry engaged in extraction of water from the earth. Extractive Industries engage in processes that involve different activities that lead to the extraction of raw materials from the earth such as oil, metal, minerals and other aggregates. These processes take place within host and home countries of operating companies as well as consuming markets. There is no distinction between the extraction methods employed, with some metals being recovered by fluid dynamics and in situ recovery techniques that are identical to those used in secondary oil recovery. Geothermal energy production is also an extractive industry, and again the technology of hot water or steam production is similar to that developed with fluids like natural gas. One characteristic that differentiates the Extractive Industries from the other industries is the wasting / depletion of natural resources.

13. Highest and Best Use: Valuation of the property should be based on the Highest and Best Use of the resources. Therefore, due consideration should be given to non-Petroleum and non-Mineral uses of the property. Additionally, the impact of any changes to the exploration or other strategies should be considered for any economic impact. Thus, the Valuer needs to assess the best probable use which is legally permissible, financially feasible and physically possible, thus resulting in the highest value of the subject property.

14. Mineral: A mineral is a naturally occurring material on the earth’s crust and includes metallic minerals, fuel minerals, industrial minerals, precious stones, aggregates, etc. Definition of Minerals does not include Petroleum.

15. Mineral Reserve: Combined [Mineral] Reserves International Reporting Standard Committee (CRIRSCO) defines Mineral Reserve to be the economically mineable part (adjusted for diluting materials and allowances for losses) of a measured or indicated mineral resource demonstrated by at least a preliminary feasibility study (which considers mining, metallurgical, economic, marketing, social, governmental and legal factors). Reserves are further subdivided into Probable Mineral Reserves and Proved Mineral Reserves in the order of increasing confidence.

16. Mineral Resource: CRIRSCO defines a Mineral Resource as a concentration or occurrence of material of intrinsic economic interest in or on the earth’s crust (a deposit) in such form or quantity that there are reasonable prospects for subsequent extraction that can be useful economically.

17. Petroleum: As per the ‘Petroleum and Natural Gas Regulatory Board (PNGRB) defines petroleum as “any liquid hydrocarbon or mixture of hydrocarbons, and any inflammable mixture (liquid, viscous or solid) containing any liquid hydrocarbon, including crude oil and liquefied petroleum gas, and the expression ‘petroleum product’ shall mean any product manufactured from petroleum”. Crude oil and natural gas are the products of petroleum.

18. Petroleum Industry: The industry comprises of companies engaged in the business of exploration of petroleum and the extraction, processing, refining and marketing of crude oil and natural gas.

19. Petroleum Reserves: As defined by the Society of Petroleum Engineers, “Reserves are those quantities of petroleum which are anticipated to be commercially recovered from known accumulations from a given date forward. All reserve estimates involve some degree of uncertainty. The uncertainty depends mainly on the amount of reliable geological and engineering data available at the time of the estimate and the interpretation of these data. The relative degree of uncertainty may be conveyed by placing reserves into one of two principal classifications, either proved or unproved. Unproved reserves are less certain to be recovered than proved reserves and may be further sub-classified as probable and possible reserves to denote progressively increasing uncertainty in their recoverability.” Possible reserve implies one of the possibilities of existence of reserves of a particular quality out of many other possibilities. Out of many possibilities, in one of the possibilities of existence of reserves, probable reserve implies higher probability of existence of reserves. Any reserve is first inferred as a possible reserve. Upon reasonable delineation, a reserve may further be classified as probable reserve. Upon precise delineation, a reserve may finally be classified as proven reserve.

20. Petroleum Resources: Petroleum Resources are those quantities of petroleum, which are estimated, on a given date, to be potentially recoverable from known accumulations, but which are not currently considered to be commercially recoverable.”

21. Prefeasibility study in the extractive industry: An analysis of the Mineral or Petroleum deposit which contains details including geological, economic, environmental and other applicable factors which help in proceeding with a feasibility study.

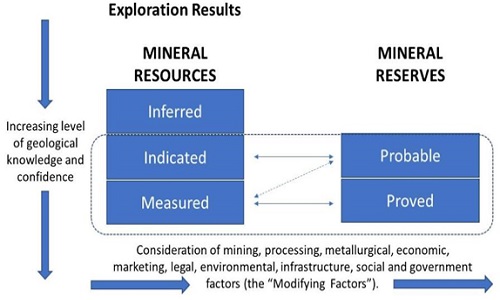

22. Relationship between Exploration Results, Mineral Resources and Mineral Reserves: Mineral Resources can be estimated on the basis of geoscientific information with input from other disciplines to establish reasonable prospects for eventual economic extraction. Mineral Reserves, which are a modified sub-set of the Indicated and Measured Mineral Resources, require consideration of those factors affecting extraction, including mining, metallurgical, economic, marketing, legal, environmental, infrastructure, social and governmental factors, and should in most cases be estimated with input from a range of disciplines. In certain situations, Measured Mineral Resources could convert to Probable Mineral Reserves rather than to Proved Mineral Reserves because of uncertainties associated with Modifying Factors which are taken into account in the conversion from Mineral Resources to Mineral Reserves.

23. Structure of oil and gas industry: The oil and gas industry is grouped into 3 main segments upstream, midstream and downstream. Upstream comprises of exploration, development and production; midstream covers transportation and storage; and downstream covers manufacturing of products through oil refining, gas processing and petrochemical processes as well as selling of these products to various consumers markets.

Significant Considerations

24. It is understood that valuation for the Mining and Petroleum sector could be more challenging as compared to other asset classes due to the following:

- ambiguity over the quantities that will actually be available for the purpose of extraction

- uncertainty of prices for extracted commodity after production and at the time of marketing and selling

- the various costs involved in exploration and recovery considering the timelines involved

- economic, physical and contractual considerations generally restrict the life of the resources

- the impact of government regulation

- impact of taxation on the sector;

- the costs of decommissioning, rehabilitation and restoration at the time of closure

25. The appropriateness of each valuation method or approach in the Extractive Industry will depend on the following:

- Stage of project (exploration, development, and production)

- Identification and classification of extent of reserves or resources

- rate of production over the LOM

- capital expenditure and operating expenditure over the LOM

- determination of expected future prices for minerals/petroleum products

- availability of reliable and adequate public information regarding comparable projects

- various stages of regulatory approval and the stage in which the subject resource is at the time of valuation

- ability to understand and forecasting the risk towards progressing to extraction (existence of environmental impact statements, etc),

- certainty regarding title, and other legal considerations (non-regulatory)

- sources of and availability of financing of the various stages

- availability of infrastructure and its financing

- marketing.

26. Mineral resources and Petroleum are subject to significant government control. Extractive Activities are subject to specific fiscal policies, that are likely to be revised depending on the political and economic situation.

27. There can be some intangible assets related with exploration and extractive activities. Examples include drill hole databases, computer software, procedure manuals, employee handbooks, operating manuals, engineering drawings, patents, environmental approvals, licences and materials and services supplier contracts. Valuers can refer to ICAI Valuation Standard 302 Intangible Assets for valuation of such intangibles, as applicable.

Valuation Bases

28. A valuer must consider the relevant valuation bases for valuation of assets in the Extractive Industries in accordance with ICAI Valuation Standard 102 Valuation Bases. However, a valuer should follow the bases prescribed by a prescribed law or regulation, if it is applicable.

Valuation Approaches and Methods

Overview

29. The valuation of Extractive Industries assets involves an understanding of the differences between the production and transportation phases of the minerals and petroleum industries. The value of the assets is a function of the surface and subsurface geological information. The sector generally has a planned phase of extraction and once the extraction is completed, there are no economically recoverable assets that can be considered for extraction at that point in time. However, the petroleum industry generally has more than one economical phase of extraction for crude oil. Exploration Assets derive their value from the existence of economically viable deposits of Mineral or Petroleum in it. The main source of value of an Extractive Industry natural resource is the projected net earnings derived from such resource. The net earnings may vary from year to year depending on the type of asset / commodity extracted, pricing considering the cyclical nature of the commodity markets, production costs, etc. Assets pertaining to Mineral and Petroleum natural resources are valued primarily based on the presence of Mineral and Petroleum Reserves and Resources including the potential for discovering such reserves and resources. The quality and quantity of the reserves and resources depends on the effectiveness of the exploration undertaken and any technical advancements. The extraction and processing of raw materials normally requires certain fixed assets and specialized plant and equipment, which generally have negligible or nil value when such assets are separated from production at the site. Rights or Interests of exploration assets are bought and sold in transactions which could be farm-in, option or joint venture arrangements (also known as partial interest arrangements). Other determinants of valuation include residual value of real property interest, plant and equipment, liabilities pertaining to environment reclamation and property improvements, etc.

30. The property type being considered for the purpose of valuation should be identified along with any in situ Minerals and Petroleum, which form a part of the property (real estate / physical land). Real property would include the following for the purpose of valuation (except otherwise stated in applicable statutes):

1) Ownership of in situ Minerals and Petroleum

2) Interest in such Minerals and Petroleum

3) Right to explore and extract such Minerals and Petroleum

31. The business activity comprises of operation of petroleum well, quarry or mine as well as processing and transportation of Minerals and Petroleum. It is thus important to identify the property interests and related rights to be valued. The Valuer should consider the Highest and Best Use of the property while undertaking the valuation.

32. Generally, the following three main valuation approaches are adopted to measure value of Extractive Industries assets in correlation with the valuation approaches and methodologies prescribed under ICAI Valuation Standard 103 Valuation Approaches and Methods.

(a) Market approach;

(b) Income approach; and

(c) Cost approach.

33. The appropriate valuation methods employed should be decided based on the exploration and development phase / stage of the property. Mineral and Petroleum properties are generally classified in the following categories with the different stages of exploration and development carrying different levels of risk (risk of ultimate Mineral and Petroleum production).

- Exploration properties: A Mineral or Petroleum real property interest that is under active exploration for Mineral deposits or Petroleum accumulations. However, economic viability for the same has not been demonstrated.

- Resource properties: A Mineral or a Petroleum Resource which has however not been established through a Pre-feasibility Study or Feasibility Study to be economically beneficial or viable.

- Development properties: Properties which are established as economically viable through a Feasibility Study, however, there is no production.

- Production properties: An operation with active production of Mineral and Petroleum as of the valuation date is understood to be a Production property.

34. The requirements of this Standard shall be followed consistently in addition to the requirements as contained in ICAI Valuation Standard 103, while selecting and applying the valuation approach. Reasons for using one or more methodologies should be stated along with explanation towards using a particular methodology/ies. The concluding value should be based on the appropriate weights, where more than one methodology is considered. A valuer should provide justification for applying weightages to a particular methodology.

35. As a practice, properties with mineral reserves are valued using the Income Approach while properties without mineral reserves are valued using Market or Cost Approach.

36. Considering the nature of the asset, the Valuer needs to place reliance on technical experts who have estimated the quantitative information and other technical information which then forms the basis of the valuation with a significant manner.

37. The valuer must specifically disclose in his report the reliance placed on the technical experts with details of the experts and the type of report from such experts which has been relied upon in the valuation engagement.

38. The valuer when using more than one methodology, should assess and complement the findings of the methods used. It should be noted that the three approaches draw inferences from the same set of data and this should be viewed in combination when recommending the valuation conclusion.

Market Approach

39. Market approach is a valuation approach that uses prices and other relevant information generated by market transactions involving identical or comparable (i.e., similar) assets, liabilities or a group of assets and liabilities and is based on the principle of substitution of value.

40. In accordance with the requirements contained in ICAI Valuation Standard 103, the market approach shall be adopted only if adequate information is available about the comparable assets from a recent transaction and there are instances of orderly transactions that can be compared with the subject asset to be valued.

41. The Market Approach provides an indication of value by comparing the subject asset with identical or similar assets for which price information is available. The price information could be for individual assets or a collection of assets that are considered together in an extractive activity. Adjustments could be required to incorporate any differences between the comparable asset and the subject asset and differences in timing. Price information is often analysed based on units of comparison, eg prices per tonne or multiples of earnings. There could be certain constraints in applying the Market Approach in the Extractive Industries because extraction activities are heterogeneous in nature, and it is often necessary to make significant adjustments to such price information that is available in relation to transactions involving similar assets. Examples of some differences that may require transaction data to be adjusted include cost of extraction, location, accessibility, quality and status of reserve and the quality of the equipment used in the activity.

42. Methods involving Comparable multiples help in determining the value of the mining projects in comparison to the comparable mining projects. Under the Comparable Transactions method, the transaction price of comparable properties is used to determine the value of the subject property. Valuers need to take cognizance of the fact that exploration is cyclical, due to which there will be relatively lesser transactions in periods of low metal prices (due to the subdued state of the industry). Comparable Transactions are required for valuing speculative and exploration properties as there is relatively less adequate data available to undertake a fundamental DCF analysis.

43. Given the nature of the asset and the diversity involved, each Exploration Property, Mineral deposit and Petroleum accumulation can be unique with specialized characteristics. Considering the inimitability of the property involved, direct comparison of Mineral and Petroleum resources could be difficult or irrelevant. Nevertheless, sales analysis is considered to be an important tool to undertake an indirect sales comparison (with the use of sales adjustment or ratio analysis). If the valuer is able to obtain reliable and adequate information to assemble a reasonable database of values, inputs such as value per unit area of the property or value per unit of contained metal in Mineral Resources or Mineral Reserves can be applied. The important metrics to obtain the value are as below:

- Price to Net Asset Value (P/NAV): P/NAV is an important mining valuation metric. “Net asset value” is the net present value (NPV) or discounted cash flow (DCF) value of all the future cash flow of the mining asset less any debt plus any cash. The model can be forecast to the end of the mine life and discounted back today because the technical reports have a very detailed Life of Mine plan (LOM). NAV is computed as the sum-of-the-parts approach to valuation, in that each individual mining asset is independently valued and then added together. Corporate adjustments are made at the end, such as head office overhead or debt. The formula is as below:

| P/NAV = Market Capitalization / [NPV of all mining assets – net debt] |

- Price to Cash Flow (P/CF): The price to cash flow ratio, or “P-cash flow” is also common but only used for producing mines, as it takes the current cash flow in that year, relative to the price of the share. The ratio takes the adjusted cash flow of the business in a given year, and compares that to the share price. Operating cash flow is after interest (and thus an equity metric) and also after taxes, but it does not include capital expenditures. The formula is as below:

| P/CF = Price per Share / Cash from Operations per Share |

- EV/Resource: This ratio takes the total resources contained in the ground and divides it by the enterprise value of the business. This metric is typically used for early-stage development projects, where there is not a lot of detailed information (not enough to do a DCF analysis). The ratio is very basic and does not take into account the capital cost to build the mine, nor the operating cost to extract the metal. The formula is as below:

| EV/Resource = Enterprise Value / Total weight in units of Metal Resource2 |

- Total Acquisition Cost (TAC): Another commonly used metric in the mining industry for early-stage projects is Total Acquisition Cost or TAC. This represents the cost to acquire the asset, build the mine and operate the mine, all on a per unit basis. The formula is as below:

| TAC = [Cost to Acquire + Cost to Build + Cost to Operate] / Total weight in units |

Additionally, the value obtained as sum of the parts or component value is usually representative of the value of the Extractive Industries’ assets and businesses.

Income Approach

44. Income approach is the valuation approach that converts maintainable or future amounts (e.g., cash flows or income and expenses) to a single current (i.e. discounted) amount. The fair value measurement is determined on the basis of the value indicated by current market expectations about those future amounts and is based on the principle of anticipation of value.

45. The Income approach considers the “value-in-use” principle and requires determination of the present value of future cash flows over the useful life of the property. The value using the Income Approach considers the expected benefits from the property, usually in the form of discounted cash flows or using real option analysis in conjunction with the income approach.

46. The Discounted Cash Flows (DCF) method is one of the methods to value a mining asset as it takes into account a mining plan obtained from a feasibility study report (one of the most bankable technical assessment of the asset) or other relevant inputs that can be obtained. DCF method is one of the primary valuation methodologies for development properties and producing mines. The underlying valuation premise is that the value is reflective of the current net economic benefit of cash flows that are expected to be generated over the life of the asset / property / resource. This involves determination of the present value of the net after-tax cash flows of the property. The present value of cash flows is computed using a discount rate and discounting factor which is representative of the rate of return on investment that accounts for the time value of money and risk factors involved. The valuer will be required to assess the amount, timing and certainty of future cash flows from any exploration and evaluation assets recognized.

47. The Income Approach is widely used for production and development properties while holding lesser relevance for exploration properties. Certain important considerations are required to be placed while using the DCF model to determine the value of the property:

- It has been observed that the standard DCF models incorporate a single net cash flow stream which captures the most expected value from the property using a particular variable such as the grade of metal. Valuers need to take cognizance of the fact that the grade and quality differences are likely to be present and this uncertainty of expected quality differences may impact the value of the property. A sensitivity analysis in this case would exhibit differences in values where the metal prices vary based on the quality. To overcome this limitation, valuers can consider the Monte Carlo simulation for analysis of more uncertainty in which a set probability distribution describes possible changes in a specific variable during the project. The model can be enhanced with lognormal stochastic processes for model reversion or tendency of a variable (metal price) to revert over time to a long-term equilibrium level, which may then restrain long term cash flow uncertainty. These models can be extended to reflect other characteristics such as uncertainties in long term equilibrium price levels and structures of forward curves.

- While a static DCF model relies on a standard production policy, predetermined financing and taxation payouts, etc., consideration must be given to the fact that the operating policies could change and payoffs relating to taxation and financing could be altered with the changing business environment. This limitation of static DCF is particularly challenging for estimating the value of sub economic resources at a gold or copper-gold mine, the economic impact of windfall taxes, or the true cost of a financing arrangement with embedded commodity derivatives. As a standard industry practice, a series of models are developed considering different designs and project environments.

48. The key steps to develop a DCF model for a property are as below:

1) Understanding the Life of Mine (LOM) for the resource

2) Analysing the quantity of the resource to be produced every year / time period

3) Understanding of the commodity price to be considered for the forecast period or LOM

4) Computation of total revenue (Step 3 x Step 4)

5) Estimation of operating costs / margins and capital expenditures and other contingencies

6) Computation of free cash flows and discount rate (depending on the stage of production)

7) Calculation of net present value (NPV)

49. A valuer shall refer to the section on Discount Rate which is explained in detail in ICAI Valuation Standard 103, Valuation Approaches and Methods. The Discount Rate to compute the present value of cash flows can be computed using one of the following methods.

1) Capital Asset Pricing Model (CAPM)

2) Weighted Average Cost of Capital (WACC)

3) Rate build-up method

50. The valuer needs to consider certain factors for building the discount rate, which are as below:

1. Development and Production stages;

2. Weighted Average Cost of Capital for the sector

3. Asset specific Risk

4. Inflation

5. Other applicable factors

6. Aggressiveness of the pricing assumptions in the cash flow, i.e. higher discount rate for more aggressive pricing assumptions as compared to conservative assumptions.

Real Option Analysis3

51. Real Option Analysis is a valuation approach that reflects the benefit of the flexibility in decision making and is useful in cases where there are significant uncertainties.

52. Option pricing methods are not very widely used in all types of valuations. They are generally reserved for valuations where information is scarce, as in the case of exploration properties.

53. In the case of operating mines, real option pricing, despite the understanding that it values future flexibility more adequately than DCF, is not often used in view of the complexity and the inter-linkages with the projections which are prepared for many purposes and thus, giving preference to the DCF method.

54. However, this approach may be of use and relevance in cases where there are significant uncertainties or future flexibilities are of importance.

Cost Approach

55. Cost approach is a valuation approach that reflects the amount that would be required currently to replace the service capacity of an asset (often referred to as current replacement cost) and is based on the principle of contribution to value.

56. Cost approach considers the possibility that, as a substitute for the purchase of a given property, the entity could construct another property that is either same as the original property or similar to the original property capable of furnishing equal utility.

57. Generally, a property under the Cost approach is valued by estimating the current cost to construct a reproduction of or replacement for the existing structure, adding any land value, deducting depreciation and including developer’s profit.

58. The Cost approach is relatively lesser reliable from a valuation perspective, but is commonly used as an analytical tool in allocating the contributory value of various elements of the property. The Cost Approach can be applied in the Extractive Industries when there is either no sufficiently reliable income projections to use an Income Approach or appropriate transactional data that can be applied to use a Market Approach. Some of the methods of valuing a property under the Cost approach are as below:

1) Depreciated Replacement Cost (DRC) method: The DRC method is generally applicable to buildings, surface structures, specialised plant and equipment, etc. The value of the property under DRC method is determined as below:

| DRC = (Reproduction or Replacement Cost) – (Physical Depreciation + Functional Obsolescence + External Obsolescence) 0) |

2) Multiple of Exploration Expenditure (MEE): This method is applicable to properties without delineated / specific resources. A Prospective Enhancement Multiplier (PEM), based upon a Valuer’s assessment of the property’s potential to date, is applied to the relevant and effective past exploration expenditure on the property. The value of the property under the MEE method is determined as below:

| Value = Effective Expenditure x PEM |

3) Appraised Value method: This method is similar to MEE method, wherein an adjustment for future warranted expenditures (exploration budget to test the remaining exploration potential of the property) is made. The Appraised Value Method is based on the assumption that the value of a property is derived from its potential for the existence and finding of a mineral deposit with economic value and that the amount of exploration expenditure is related to its value. The appraised value is calculated as an aggregate of the relevant past exploration expenditures and warranted future costs. Relevant past expenditures would mean only those expenditures incurred in the past that are considered appropriate to be considered as an expenditure and have contributed to identification of exploration potential. Warranted future costs comprise a relevant exploration budget to test the identified potential and remaining potential if any. This method is best applied to properties which are actively being explored. The cost information and technical data is generally readily available for marginal development properties and exploration properties. However, the valuer may be required to apply appropriate judgement so as to bifurcate the productive and nonproductive past expenditures. It is thus prudent to compare the value of a property using this method with other methods of valuation. The value of the property under the MEE method is determined as below:

| Value = Effective Expenditure + Warranted Expenditure |

As per Ind AS 106 – Exploration for and Evaluation of Mineral Resources, the following are examples of expenditures that might be included in the initial measurement of exploration and evaluation assets (the list is not exhaustive) – acquisition of rights to explore, topographical, geological, geochemical and geophysical studies, exploratory drilling, trenching, sampling and activities in relation to evaluating the technical feasibility and commercial viability of extracting a mineral resource, etc. Expenditures related to the development of mineral resources shall not be recognised as exploration and evaluation assets. Some challenges faced in considering the Cost Approach involve identifying the cost of an equivalent asset and establishing the appropriate depreciation allowances to reflect physical, functional or economic obsolescence.

Effective Date

59. ICAI Valuation Standard 304 Valuation of Assets in the Extractive Industries, shall be applied for the valuation reports issued on or after 1st ……… 20224.

Note:

1. Appendix A to Ind AS 106 Exploration for and Evaluation of Mineral Resources

2. Can use Probable Reserves or Proven Reserves multiple

3. ICAI Valuation Standard paragraphs 92-94 of ICAI Valuation Standard 103

4. Date to be specified by notification