TRANSFER OF CREDIT IN CASE OF BUSINESS RE-ORGANIZATION

1) Background

In the present scenario, where most of the business organizations are unable to survive alone; on account of the liquidity crunches, weak management, etc; Business Re- Organization; is the need of the hour where most probably the strong concerns have an opportunistic takeover of the weak firms to revive the latter. Business Re‑

Organization may take place in various forms; such as merger, demerger, acquisition, change in ownership of business; etc. Under such restructuring, there is also an impact on the GST

Input Tax Credit and various questions emerges as

How, How Much, & How to transfer the unutilized credit. To leave no iota of doubt, CBIC has issued

Circular No.133 03/2020 – GST – Dated 23.03.2020 addressing the various representations received from various organizations.

| 2) LEGAL POSITION: | Section 18(3) of the CGST Act, 2017 read with Rule

41(1) of the CGST Rules, 2017 deals with the apportionment and transfer of CREDIT. Section 18(3) of the CGST Act,2017:

Rule 41 of the CGST Rules,2017: 1) A registered person shall, in the event of sale, merger, de-merger,

Provided that in the case of demerger, the input tax credit shall be apportioned in The ratio of the value of assets (i.e. value of entire assets of the business, whether or not ITC has been availed thereon) of the new units as specified in the demerger scheme.. In short, ITC to be apportioned =

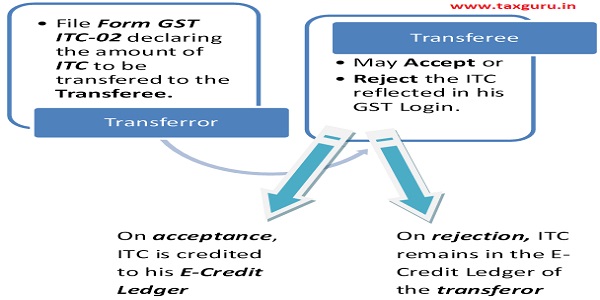

2) The transferor shall also submit a certificate issued by a practicing

Certifying that the sale, merger, demerger, amalgamation, lease or transfer of a business has been done with a specific provision for the transfer of liabilities. 3) The transferee shall, on the common portal, accept the details so furnished by the transferor, and upon such

4) The inputs and capital goods so transferred shall be duly accounted for by the transferee in his books of account.

|

Above adjustment entries, need to be made in the books of account of the Transferee Company to give effect to transfer of the business.

| 3) DOUBTS: | The various doubts arising amongst the business organizations are as follows:

1) While calculating the ratio for apportionment, whether value of assets of the new units is to be taken at

2) Is the transferor required to file Form GST-ITC-02 in all states in which he is registered? 3) Proviso to Rule 41(1) explicitly mentions ‘demerger’. So whether this proviso applies to:

4) Whether the ratio for apportionment applies to each head of ITC, viz:

5) How to determine the amount of ITC to be transferred by the transferor while filing Form GST ITC -02 under each head of tax, viz

6) To calculate the amount of ITC to be transferred, which date unutilized ITC balance in the ELECTRONIC CREDIT LEDGER of the transferor to be taken? 7) Which date shall be relevant to calculate the ratio of the value of assets as prescribed in proviso to Rule 41 (1)? |

||||||||||||||||||||||||||||||||||||||||||||||||

| 4)CLARIFICATIONS: | Such doubts arising from the various tax payers has been clarified by vide CIRCULAR No 133 03/2020 – GST dated 23rd March, 2020.

Q1) In case of multiple registrations, ratio for the apportionment of ITC is to be calculated at state level Or at all INDIA level? → For the purpose of apportionment of ITC, ratio to be calculated at state level.

CRUX: At the State level and NOT at all India level. Q2) In case of multiple registration, Form GST ITC-02 is required to be filed by the transferor in all the states? → No, only in the states where both the transferor and the transferee is registered. Q 3) Proviso to Rule 41(1) explicitly mentions “demerger”. Whether other forms of business reorganization where part of the business is hived off or transferred as a going concern or where there is partial transfer of assets along with liabilities? → Yes, the formula prescribed in the proviso to Rule 41(1) is applicable to all forms of business re-organization, where there is partial transfer of assets along with liabilities. Q4) Whether the ratio is to be applied to each head of ITC viz,CGST, SGST, IGST,Cess separately or together? →The ratio is to be applied to the sum of unutilized (CGST+SGST+IGST) of the transferor.

CRUX: Apply ratio to the TOTAL of the Unutilized ITC. Q5) How to determine the total amount of ITC to be transferred under each head (viz. CGST, SGST, IGST) while filing Form GST ITC-02 by the transferor? → Step:1 Calculate the ratio: Ratio = value of assets of new units total value of assets before demerger Step:2 Calculate the total ITC to be transferred: ITC to be transferred to the transferee = Ratio (as calculated in Step:1) * Total unutilized ITC (sum of CGST+SGST+IGST) Step:3 Determine the amount of ITC to transferred under each head: Amount of ITC to be transferred under each head (viz CGST, SGST, IGST) left to be decided by the transferor ,but shall not EXCEED:

llustration: State: Rajasthan Ratio of assets transfer: 70%

CRUX: Do analysis and transfer ITC to the transferee under each head in the best possible manner. Q6) For the purpose of proviso to Rule 41(1), which date unutilized balance of ITC of the transferor to be taken? → Unutilized ITC balance on the date of filing of the Form GST ITC-02 is to be considered for the purpose of proviso to Rule 41 (1). Q7) On which date, the ratio of the value of assets to be considered? → The ratio of the value of assets to be taken on the “appointed date of demerger” (i.e. the date on which the scheme of demerger comes into force and such date is specified in the scheme of Demerger). |

DISCLAIMER: This article is based on the personal understanding and legal interpretation of the author and does not render any professional advice.

In case of any queries or doubts, please feel free to ask at visheshsurana@yahoo.com

Author Bio

What compliances we need to follow for transfer of business with no input tax credit?