CBDT vide Notification No. 31/2020-Income Tax dated 29/05/2020 notified Sahaj (ITR-1), Form ITR-2, Form ITR-3, Form Sugam (ITR-4), Form ITR-5, Form ITR-6, Form ITR-7 and Form ITR-V for A.Y. 2020-21

In this article we will discuss about the Sahaj (ITR- 1), its applicability and new changes in Sahaj (ITR- 1) which are appliable to A.Y. 2020-21.

ITR – 1 – Sahaj is applicable to the following:

- Individuals being a resident (other than not ordinarily resident

- having total income upto Rs.50 lakh.

- having Income from Salaries or Pension.

- Having income from one house property as a joint owner / single (excluding brought forward losses and losses to be carried forward)

- Having income from other sources (Interest, Any other etc.)

- Agricultural income upto Rs.5 thousand

ITR – 1 – Sahaj is not applicable to the individuals who are not falling under the above mentioned conditions and individuals who are

- Director in a company or

- Invested in unlisted equity shares

ITR 1 -Sahaj for A.Y. 2020-21 in PDF format with detailed Notification 31 dated 29th May 2020, Income Tax can be downloaded by clicking on the link provided below:

https://www.incometaxindia.gov.in/communications/notification/notific ation31 2020.pdf

New changes in ITR1-Sahaj, applicable to A.Y. 2020-2 1 are

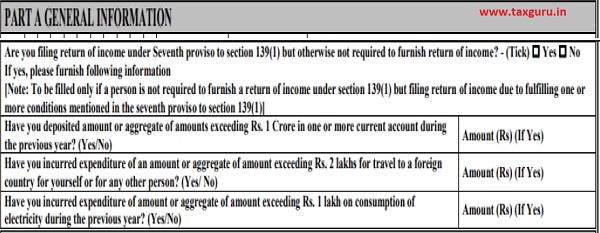

A. Information about the newly introduced Seventh Proviso to sub-section 1 of Section 139

Following seventh proviso shall be inserted after the sixth proviso to sub-section (1) of section 139 by the Act No. 23 of 2019, w.e.f. 1-4- 2020 :

Provided also that a person referred to in clause (b), Sub-section (1) of section 139 who is not required to furnish a return under this sub-section, and who during the previous year—

(i) has deposited an amount or aggregate of the amounts exceeding one crore rupees in one or more current accounts maintained with a banking company or a co-operative bank; or

(ii) has incurred expenditure of an amount or aggregate of the amounts exceeding two lakh rupees for himself or any other person for travel to a foreign country; or

(iii) has incurred expenditure of an amount or aggregate of the amounts exceeding one lakh rupees towards consumption of electricity; or

(iv) fulfils such other conditions as may be prescribed, shall furnish a return of his income on or before the due date in such form and verified in such manner and setting forth such other particulars, as may be prescribed.

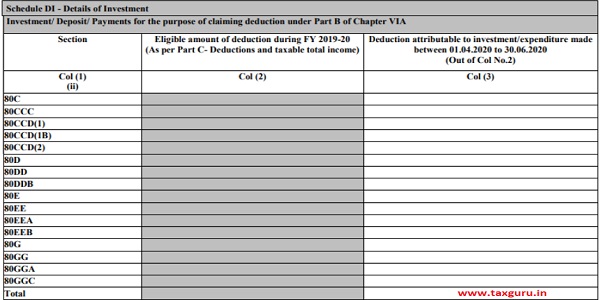

B. New Schedule DI- Details of Investment

This schedule DI is newly introduced during the A.Y. 2020-21.

Due to Corornavirus lockdown, the government has extended the timelimit for completion of Investment in tax-saving deposits for FY20 19- 20 from 3 1.03.2020 to 30.06.2020.

As per the below mentioned table, in col (2), Assessee has to mention the Total amount invested in Tax Savings Deposits till 30.06.2020 for F.Y. 2019-20, out of this, amount deposited between 01.04.2020 to 30.06.2020 & which is to be claimed for F.Y. 20 19-20 to be mentioned in Col (3).

The assessee can claim the investment made between 01.04.2020 To 30.06.2020 in either F.Y. 20 19-20 or F.Y. 2020-2 1.

How to file ITR 1 –Sahaj

The ITR 1 -Sahaj can be filed

Option 1: By generating and uploading an XML file.

For this you need to download excel or the JAVA utility provided at the below mentioned link.

https://www.incometaxindiaefiling.gov.in/downloads/incomeT axReturnUtilities

Fill all the details as asked in the utility, generate XML and upload it by login to the Income Tax India efiling site https://www.incometaxindiaefiling.gov.in/home

Option 2: By directly preparing and submitting ITR 1 online through login.

If you do not want to go for option 1 i.e. filling the excel or JAVA Utility, you can directly log in to your Income Tax Account on the Income Tax India efiling site https://www.incometaxindiaefiling.gov.in/home and fill in the required details online and submit your ITR 1.

Due date for filing ITR 1- Sahaj for A.Y. 2020-21

The last date of filing ITR-1 for FY 2019-20 (A.Y. 2020-21) has been extended to November 30, 2020.

Fee for default in furnishing Return of Income

W.e.f. assessment year 20 18-19, if assessee who is required to furnish return of income under section 139 failed to furnish return of income within due date as prescribed under section 139(1) then as per section 234F, he will be required to pay fee of:-

a) Rs. 5000 if return is furnished on or before 31stDecember of assessment year.

b) Rs. 10,000 in any other case.

However, if total income of the person does not exceed Rs. 5 lakh then fee payable shall be Rs. 1000.