India’s young and educated population, growing and aspirational middle class, regular flow of direct investments outside India and huge push on infrastructure development are all the ingredients to propel growth. India has emerged as one of the large economies in the world, and it is expected to continue on this growth trajectory in the foreseeable future.

With the aim to diversify the business abroad, avail the opportunity thrown by the overseas market, to make full utilization of full capacity, branding, and many more reasons inspire the entities to go overseas, invest and set up business over there and it not only benefits the investing entities, also the county in the form of better promote economic co-operation with the host countries, branding of a country as investor and much more.

The transactions on account of Overseas Direct Investments are governed by clause (a) of section 6 (3) of the Foreign Exchange Management Act, 1999 read with Foreign Exchange Management (Transfer or Issue of Any Foreign Security) Regulations notified vide Notification No. FEMA.120/RB-2004 dated July 7, 2004.

Section 6(3) of the Foreign Exchange Management Act, 1999 confers to the Reserve Bank of India (RBI) powers to prohibit, restrict or regulate the transactions by imposing necessary restrictions.

In this article, we have tried to focus on the basic concepts that will enlighten about achieving the technical know- how and the provisions before making such Investment.

1. Governing regulations for making overseas investment :

The guidelines have been notified by the Reserve Bank of India vide Notification No. FEMA 120/RB-2004 dated July 7, 2004, as amended from time to time, which can be accessed at the Reserve Bank’s website http://www.rbi.org.in/scripts/Fema.aspx.

A Master Direction titled ‘Master Direction on Direct Investment by Residents in Joint Venture (JV) / Wholly Owned Subsidiary (WOS) Abroad’ has been issued. The Master Directions consolidate instructions on rules and regulations framed by the Reserve Bank under various Acts including banking issues and foreign exchange transactions and is available at ‘Notification’ Section on RBI’s website https://www.rbi.org.in.

Any further clarifications in respect of cases not specifically or generally covered by the instructions may be obtained from the concerned Authorized Dealer (AD) bank. If, however AD bank fails to provide satisfactory reply, a request may be made, giving full details of the case, to the Central Office of the Reserve Bank by routing it through AD bank.

2. Meaning of Overseas Direct Investment :

Overseas direct investment means direct investment outside India means investments, either under the Automatic Route or the Approval Route, by way of

1. Contribution to the capital or

2. Subscription to the Memorandum of a foreign entity

3. Purchase of existing shares of a foreign entity either by market purchase or private placement or through a stock exchange, signifying a long-term interest in the foreign entity (Joint Venture JV or Wholly-Owned Subsidiary WOS).

3. Definitions:

- Joint Venture (jv)/ Wholly Owned Subsidiary :“Joint Venture (JV)”/ “Wholly Owned Subsidiary (WOS)” means a foreign entity formed, registered or incorporated in accordance with the laws and regulations of the host country in which the Indian party/Resident Indian makes a direct investment;

A foreign entity is termed as JV of the Indian Party/Resident Indian when there are other foreign promoters holding the stake along with the Indian Party. In case of WOS entire capital is held by the one or more Indian Party/Resident Indian.

- An Indian Party: An Indian Party is a company incorporated in India or a body created under an Act of Parliament or a partnership firm registered under the Indian Partnership Act 1932 or a Limited Liability Partnership (LLP) incorporated under the LLP Act, 2008 and any other entity in India as may be notified by the Reserve Bank. When more than one such company, body or entity makes investment in the foreign JV / WOS, such combination will also form an “Indian Party”.

- Automatic Route: Under the Automatic Route, an Indian Party does not require any prior approval from the Reserve Bank for making overseas direct investments in a JV/WOS abroad.

The Indian Party should approach an Authorized Dealer Category – I bank with an application in Form ODI and the prescribed enclosures / documents for effecting the remittances towards such investments. However, in case of investment in the financial services sector, prior approval is required from the regulatory authority concerned, both in India and abroad.

- Approval Route:Proposals not covered by the conditions under the automatic route require prior approval of the Reserve Bank for which a specific application in Form ODI with the documents prescribed therein is required to be made through the Authorized Dealer Category – I banks.

4. Eligibility for the investment in overseas direct investment :

- An Indian Party is eligible to make an overseas direct investment under the Automatic Route.

- With effect from 5th August, 2013, a Resident Individual satisfying the conditions mentioned in the Master Direction may make overseas investment in the equity shares and compulsorily convertible preference shares of a JV or WOS outside India with the ceiling limits mentioned in the Liberalized Remittance Scheme, as prescribed by the RBI from time to time.

5. General Permission available to persons (individual) resident in India for purchase / acquisition of securities abroad :

a) Out of funds held in the RFC account;

b) As bonus shares on existing holding of foreign currency shares;

c) When not permanently resident in India, from the foreign currency resources outside India.

General permission is also available to sell the shares so purchased or acquired.

A resident Indian can remit; up to the limit prescribed by the Reserve Bank from time to time, per financial year under the Liberalized Remittance Scheme (LRS), for permitted current and capital account transactions including purchase of securities and also setting up/acquisition of JV/WOS overseas with effect from August 5, 2013 (vide Notification No. 263).

6. The Transactions that require the prior approval of RBI:

- Real Estate Business.

- Banking Business (However, Indian banks can set up JVs/WOSs abroad provided they obtain clearance under the Banking Regulation Act, 1949)

- Clarification-An overseas entity, having direct or indirect equity participation by an Indian party, shall not offer financial products linked to Indian Rupee (e.g. non-deliverable trades involving foreign currency, rupee exchange rates, stock indices linked to Indian market, etc.) without the specific approval of the Reserve Bank

> The other ODI transactions that require RBI approval :

-

- Overseas Investments in the energy and natural resources sector exceeding the prescribed limit of the net worth of the Indian companies as on the date of the last audited balance sheet;

- Investments in Overseas Unincorporated entities in the oil sector by resident corporates exceeding the prescribed limit of their net worth as on the date of the last audited balance sheet, provided the proposal has been approved by the competent authority and is duly supported by a certified copy of the Board Resolution approving such investment.

- Overseas Investments by proprietorship concerns and unregistered partnership firms satisfying certain eligibility criteria;

- Investments by Registered Trusts/Societies (satisfying certain eligibility criteria) engaged in the manufacturing / educational / hospital sector in the same sector in a JV / WOS outside India;

- Corporate guarantee by the Indian Party to second and subsequent level of Step Down Subsidiary (SDS);

- All other forms of guarantee which is offered by the Indian Party to its first and subsequent level of SDS;

- Restructuring of the balance sheet of JV/WOS involving write-off of capital and receivables in the books of listed/ unlisted Indian Company satisfying certain eligibility criteria mentioned under Regulation 16A of notification ibid;

- Capitalization of export proceeds remaining unrealized beyond the prescribed period of realization will require the prior approval of the Reserve Bank.

7. Conditions for making investment in ODI :

By Indian Party:

a) The total financial commitment of the Indian Party in Joint Ventures/Wholly Owned Subsidiaries shall not exceed 400%, or as decided by the Reserve Bank from time to time, of the net worth of the Indian Party as on the date of the last audited balance sheet;

b) The direct investment should be made in an overseas JV or WOS engaged in a bonafide business activity;

c) The Indian Party should not be on the Reserve Bank’s Exporters caution list /list of defaulters to the banking system circulated by the Reserve Bank or Credit Information Bureau (India) Ltd. (CIBIL) or any other credit information company or under investigation by any investigation /enforcement agency or regulatory body;

d) The Indian Party must have submitted its Annual Performance Report in respect of all its overseas investments in the format given in Part III of the Form ODI;

e) The Indian Party must route all transactions relating to the investment in a Joint Venture/Wholly Owned Subsidiary through only one branch of an authorized dealer to be designated by it

f) The Indian Party must submit Part I of the Form ODI, duly completed, to the designated branch of an authorized dealer within 30 days of transaction.

By Resident Individual :

Individuals resident in India may invest by way of purchasing/acquiring shares of a foreign entity as a part/full consideration for rendering professional services or in lieu of director’s remuneration.

However, the aforesaid manner of acquiring such shares in terms of value shall be within the overall ceiling limit i.e. US$250,000 in a financial year as prescribed for the resident individuals under the Liberalized Remittance Scheme (LRS) in force at the time of acquisition.

In case the value of shares exceeds the limit mentioned under the LRS, such shares are to be acquired after the consent of the RBI.

8. The various filing requirements in ODI are

i. Form ODI Part I– Application for making overseas direct investments and reporting of Remittances/ Transactions to be submitted by the applicant to the RBI

ii. Form ODI Part II – Annual Performance Report (APR) – To be submitted, certified by Statutory Auditors of the Indian party, through the designated AD Category– I bank every year by June 30th as long as the JV / WOS is in existence.

iii. Form ODI Part III – Report on disinvestment by way of closure/ voluntary liquidation, winding up of the JV/WOS abroad/ sale / transfer of the shares of the overseas JV/ WOS to another eligible resident or non-resident/ Buy back of shares by the overseas JV/ WOS of the IP/RI .

9. Annual Return on Foreign Liabilities and Assets :

It has been notified under FEMA 1999 and it is required to be submitted by all the India resident companies which have made overseas investment in any of the previous year(s), including current year by July 15 every year. Non-filing of the return before due date will be treated as a violation of FEMA and penalty clause may be invoked for violation of FEMA.

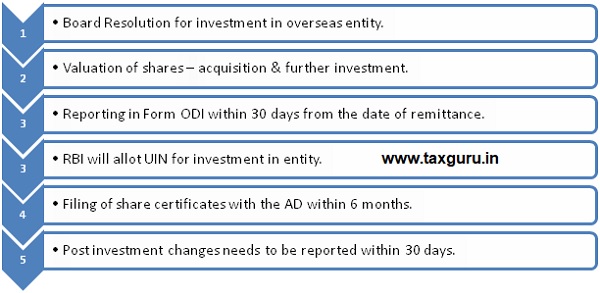

10. To Wrap-up the Overseas Direct Investment –Procedure are as follows :

As it can be seen from above, there are a plethora of rules & regulations, and checks and balances which RBI has kept in place; however that said, in my opinion it is admirable that RBI has ensured a hassle free ODI policy for willing and genuine investors.

Author kindly contact:-harshita.dhariwal@jainshrimal.in Mo. +91-9929984880

Author Bio

Annual performance report shall be submitted every year by IP by 31st December in Part II of Form ODI.

Annual performance report shall be submitted every year by IP by 31st December in Part III of Form ODI.

Dear Ma’am,

I rarely put comments,But I have to say that this is the best article on Basics of ODI, till now I had read this topic on various other platforms ,but getting here altogether is really helpful.