Accounting Standard –1 (Disclosure of Accounting Policies) and Indian Accounting Standard -1 (Presentation of Financial Statements) Along with Impact of COVID-19 Over the same.

Accounting Standard –1 (Disclosure of Accounting Policies)

1. Purpose: Purpose of this standard is to promote better understanding of financial statements by establishing the practice of disclosure of significant accounting policies followed and the manner in which they are disclosed in the financial statements so as to enhance meaningful comparison between financial statements of different organizations.

2. Fundamental Accounting Assumptions

3. Accounting Policies: Refers to accounting principles and methods of applying these principles in preparation and presentation of financial statements of an organization.

4. Accounting Disclosures

4. Accounting Disclosures 5. Impact of COVID-19

5. Impact of COVID-19

Management of the entity should assess the impact of COVID-19 over its organisation and the measures taken on its ability to continue as a going concern for such a purpose an entitiy should consider the events occurring after the balance sheet date that may lead to ceasation of entity for being a going concern.

And if it is analysed that the entity is no more a going concern proper facts should be disclosed as per AS-1.

Indian Accounting Standard –1 (Presentation of Financial Statements)

1. According to Ind AS-1, financial statements are a structured representation of the financial position and financial performance of an entity and are prepared to provide useful information about the:

- Financial Position (Assets, Liabilities & equity)

- Financial Performance (Income, Expenses including gains and Losses)

- Cash Flows (Including Cash Equivalents)

2. Purpose: It prescribes the basis for presentation of financial statements to ensure comparability of:

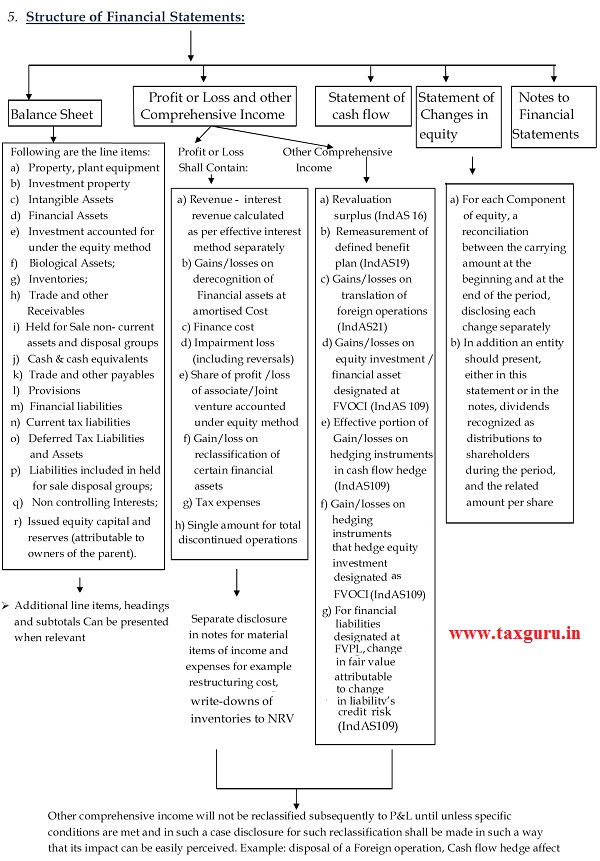

3. Constituents of Financial Statements:

- Balance Sheet

- Statement of Profit & Loss with other Comprehensive Income

- Statement of changes in equity

- Statement of Cash Flow

- Significant Accounting Policies and other explanatory notes

- Balance sheet at the beginning of the year.

- Balance sheet as at the beginning of the earliest comparative period when IND AS 8 (Accounting Policies, Estimates and Errors) applies.

- Entities may present additional information on a voluntary basis, for example Environment Reports, Value added statements, review by management including financial

- Schedule-III provides additional disclosure to Ind AS

- If any modification is required by Ind AS, Schedule-III stand modified

- Additional disclosure in addition to Ind AS and Schedule-III to be made If required by any Act or regulation

4. Key Principles:

True and Fair View:

♦ Ind AS-1 requires the entity to represent the true and fair view of the financial position, financial performance and cash flows of the entity while preparing Financial Statements and for the same entity should apply accounting policies as per Ind AS-8

♦ If management concludes compliance with an IND AS is misleading and conflicts with objective:

departure from that Standard requires Comprehensive disclosure requirements (if relevant regulatory framework requires or does not prohibit)

Compliance with Ind AS:

Standard requires an explicit and unreserved statement of compliance with IND AS be included in the notes.

Going Concern:

Management shall make an assessment of an entity’s ability to continue as a going concern. When financials are not prepared on a going concern basis, the financial statements should disclose that fact together with the reason why the entity is not considered as a going concern.

Accrual Basis of Accounting:

Financial statements (except the statement of cash flows) should be prepared under accrual basis of accounting.

Materiality and Aggregation:

♦ Present separately each material class of similar item

♦ Present separately each material class of disimilar item (unless they are immaterial)

Offsetting:

Assets, Liabilities, Income and Expenses should not be set off until unless require by any Ind AS

Frequency of Reporting:

♦ a complete set of financial statements should be presented at least annually (IFRS allows 52 Weeks)

♦ When the reporting period is longer or shorter than 1 year, an entity shall disclose:

- Reason for using a longer or shorter period

- The fact that the amounts presented in the financials are not entirely comparable

Comparative Information:

♦ Numerical comparative information in respect of the previous period should be disclosed in financial statements

♦ Narrative and descriptive comparative information is also required, to understand the current period’s financial statements.

♦ Additional comparative information may also be provided voluntarily

♦ Reclassify or represent the comparative amounts to conform to the new presentation or classification

♦ 3rd Balance sheet at beginning of preceding period if there is retrospective change in accounting policy or reclassification or restatement

♦ For material reclassification disclose nature, amount and reason

♦ If impracticable to reclassify comparative amounts, disclose reasons for not classifying and nature of adjustment that would have been made if reclassified.

Consistency of Presentation:

♦ IND AS 1 requires the presentation and classification of items in financial statements to be consistent from one period to another unless:

- Change will result in more appropriate presentation due to change in entity operations or another presentation would be more appropriate having regard to criteria for selection and application of accounting policies in Ind AS 8

- Change required by an IND AS / law.

Other Key Points:

♦ Identify each financial statement and the notes presented (e.g., Balance sheet)

♦ Name of reporting entity

♦ Whether financial statements relate to an individual entity or a group of entities

♦ Reporting date and reporting period

♦ Presentation Currency

6. Impact of COVID-19

a) Going Concern: In assessing whether the going concern assumption is appropriate, management considers all available information about the future, which is at least, but is not limited to, twelve months from the end of the reporting period. Management of the entity should assess the impact of COVID-19 and the measures taken on its ability to continue as a going concern. The impact of COVID-19 after the reporting date should also be considered and if, management after the reporting date either intends to liquidate the entity or to cease trading, or has no realistic alternative but to do so, the financial statements should not be prepared on going concern basis. Necessary disclosures as per Ind AS 1 shall also be made, such as material uncertainties that might cast significant doubt upon an entity’s ability to continue as a going concern.

b) Inventory: Due to increasing severity of COVID –19, Inventories might be necessary to write down to NRV due to reduced movement in inventory.

c) Deferred Tax Asset/ Deferred Tax Liabilities: COVID-19 could affect future profits and/or may also reduce the amount of deferred tax liabilities. Management should disclose significant judgements and estimates made in assessing the recoverability of deferred tax assets.

d) Classification of Liabilities from non-current to current: Due to impact of COVID-19, many instances may arises for the concern that make the liability to be due for the payment and thus may lead to classify the liability as current. But if the lender refuses to demand the payment against the loan as a consequence of the breach, after the reporting period but before the approval of Financial Statements, such reclassification need not be made.

e) Estimation of Uncertainties: Many uncertainties arise due to the epidemic which may affect the estimations of amount recognized in balance sheet as of reporting date. Such estimation needed to be disclosed carefully as per Ind AS-1.

f) Comparative Informations: Due to the epidemic, preparers of Financial statements shall make proper disclosures and explanatory notes over the impact of COVID-19 on the financial position of the entity.

Author Bio