Preparation For New Export Remission Scheme: Remission of Duties & Taxes On Export Products (RODTEP)

Part 1 of the Article

The Merchant Export from India (MEIS) Scheme and some other pre-export and post-export incentive Schemes are expected to be withdrawn from 1st April 2020. A New Scheme Remission of Duties & Taxes on Export Products (RoDTEP) is being drafted by The Ministry of Commerce to replace the existing Schemes. The Ministry is deliberating with Trade & Industry and has already issued circulars for Trade to propose to them on the suggested benefits for their Industry. It is the right time for Trade & Industry to respond and share their views in the best interest of their Industry.

In The Union Budget 2020, it has been proposed to insert Section 51B in the Customs Act, 1962 so as to create an Electronic Duty Credit Ledger in the customs system which will enable duty credit in lieu of duty remission to be given in respect of exports or other such benefit in electronic form for its usage, transfer etc. This seems a precursor to The Remission of Duties & Taxes on Export Products (RoDTEP)

Page Contents

Various Export Incentive Schemes for Exporters at present –

A: Pre- Export Incentive Schemes for Exporters

(a) Advance Authorization Scheme (commonly known as Advance Licence under which input materials for exports as per SION can be imported without payment of Custom Duty;

(b) Duty Free Import authorization Scheme (DFIA);

(c) Export Promotion Capital Goods Scheme (Commonly known as EPCG Scheme under which capital goods can be imported for manufacturing exportable goods without payment of duty with certain export fulfilment condition )

B: Post Export Incentive Schemes for Exporters

(a) Duty Draw Back ( A fixed % on the FOB Value of the Exports)

(b) Merchandise Exports from India Scheme (MEIS)- a fixed % of the export value of goods

(c) Services Exports India Scheme (SEIS)- a fixed % of the export of certain specified area of services (software exports not included)

C: Status Based Incentive Schemes for Exporters

(a) Export oriented unit Scheme (EOU)

(b) Special Economic Zone Scheme (SEZ)

WTO’s findings against Export Schemes

The WTO’s dispute settlement panel ruled that India’s export subsidy schemes, including the provision for special economic zones, violated core provisions of global trade norms. Some of WTO’s findings against Export Schemes are as follows –

(a) The benefits provided by India are actually subsidies since such benefits have no direct co-relation with the payment of taxes;

(b) MEIS scheme is not meant for reimbursement of taxes but these are awards.

(c) Taxes refunded are not actual but average;

(d) The capital goods which are imported under EPCG are also used for manufacturing domestic products;

(e) By exempting the importation of goods in EOU/STP and EPCG scheme from custom duties, India has foregone revenue otherwise due and hence provides financial contribution;

In this backdrop, a New Scheme Remission of Duties & Taxes on Export Products (RoDTEP) is being drafted by The Ministry of Commerce to replace the existing Schemes. The purpose of this Scheme will be to refund un-refunded taxes or duties/ levies, not exempted or rebated at present by any other mechanism. The contours of the proposed new Scheme for Remission of Duties and Taxes on Exported products (RoDTEP) are being detailed out and will be notified separately after approval of the competent authority. In the interim, to determine and recommend the rates and value caps for various items in different export sectors under the proposed scheme for Remission of Duties and Taxes on Exported Products (RoDTEP), it has been decided that the existing Sectoral Norms Committees structure in the DGFT Headquarters, will also function as Sectoral RoDTEP Committees (SRCs).

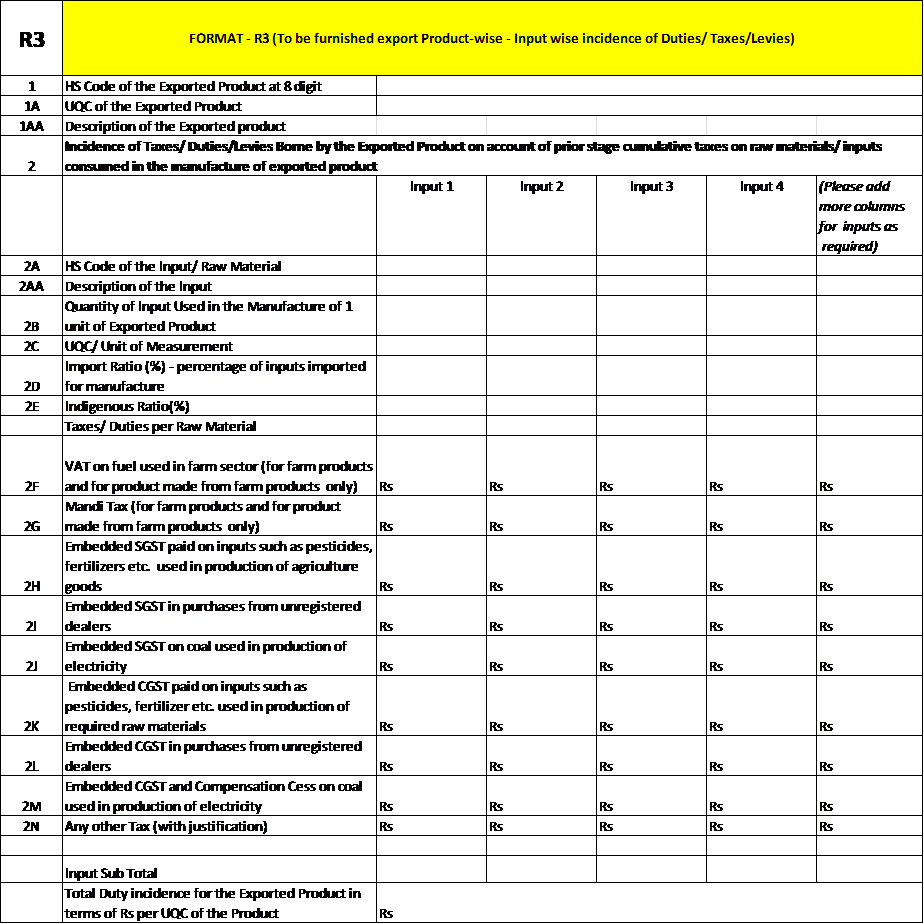

Therefore, the concerned commodity boards/Trade & Industry Associations/Chambers of commerce are requested to seek the data in the prescribed formats from the members of the industry/ firms/ exporters. The concerned associations are the nodal agencies to interact with the SRCs. The trade bodies are requested to provide data to the concerned Export Promotion Councils, with respect to un-rebated taxes/ duties/levies used in the manufacture of export product(s)in prescribed formats. The concerned associations would in turn consolidate the data product-wise, based on ITC-HS code, and forward such consolidated data along-with all supporting submissions by other exporters/manufacturers and industry associations, for each product in the prescribed proforma to this committee for further processing. There are 3 formats/ proformas(R1, R2, R3- linked below) which are required to be filled separately for each export product by a manufacturing/ exporting unit. The Industry Bodies are requested to compile information received from member exporters/firms and submit it to the concerned EPCs. EPCs would also compile the data received by them from the exporters/manufacturers. EPCs would in turn submit the compiled data along with supporting documents collected to the jurisdictional Sectoral RoDTEP Committee(s) in DGFT Hqrs, along with their recommendations, in a separate report. Recommendations made by the EPCs/Associations/Trade Bodies should mention the HS Code wise incidence of taxes/ duties/ levies in %age terms with respect to FOB Value of each product (as per Unit of Measurement (UQC) and should be supported with relevant notifications/ circulars/ justifications on tax incidence which are at present not refunded by any other mechanism.

Requisites of providing the Data –

a) Information may be submitted by manufacturers/ manufacturer exporters for every export product individually in a separate file/document in all three proforma/ formats i.e. R1, R2 and R3.

b) Data relating to DTA Unit and / or SEZ unit/ EOU/ FTWZ/ Warehouse under section 65 of the Customs Act, as the case may be, needs to be filed separately for each such unit.

c) A list of indicative taxes which should be counted for estimating the non reimbursed/ non refunded tax incidence shall be annexed with the prescribed formats. Generally used UQC Codes have also been annexed for reference. It may be ensured that only taxes/ levies/ duties borne on the exported product which are at present not getting refunded/ reimbursed under any other mechanism are counted while calculating the tax incidence on the exported product.

d) Data provided should be from manufacturers/manufacturer exporters and it should be properly scrutinized and certified by the manufacturer/ manufacturer exporter and their Chartered Accountant/Cost Accountant.

e) While forwarding the recommendations on each HS code/export product, the EPCs/ industry bodies need to ensure that information from at least five units/ firms are included so as to be representative of the industry. The units should have a representation of the small, medium as well as large manufacturer exporters.

f) The data should be supported by relevant documents such as sample Shipping Bills of export and other relevant documents forming the basis of calculation, such as Mandi Tax rate circular, Electricity Duty circular of the respective state and should have proper justifications for recommended tax incidence.

g) The data provided should pertain to only those manufacturers/units who agree to have their records and production processes inspected by the Government for the purpose of verification. Verification of data/ processes would be undertaken by DGFT, if required.

What Needs to be Done Next?

1. Trade & Industry need to fill up these Formats and send to the Ministry as soon as possible

2. The non-refundable taxes must be weeded out with a tooth-comb so that maximum benefit can be taken. It may be noted that the remission percentage (%) once fixed may be difficult to change.

3. Representations shall be made to The Ministry of Commerce & Ministry of Finance.

4. Impact Analysis for SEZ, EPCG, EOU and STP schemes may be done and the workings of such Companies may require a revisit depending upon the next steps taken by the Government of India;

5. We expect that the Government will give some transition period before scrapping the existing benefits which being enjoyed by the Traders under FTP ;

6. Status quo for Services – SEIS may continue;

In our next release we will share our practical approach for Filing Form R1, R2 & R3 and representation to The Ministry of Commerce & Ministry of Finance for greater benefit under the Scheme.

It may be noted that the Government of India has increased its budget on RoDTEP to Rs.50,000 crore from the current Rs.40,000 crore.

ANNEXURE : FORM R1, R2 & R3

R2 |

FORMAT – R2 (To be furnished export Product-wise – Data for Transportation, stamp duty and Electricity Duty etc.) | |

| Sl No. | Item | |

| 1 | HSN Code of the Exported Product at 8 Digit (as in Format R1) | |

| 2 | Unit Quantity Code (UQC) of Exported Product | |

| 3 | Description of the Export Product | |

| 4 | Period of Export | 01.01.2019 to 30.06.2019 |

| 5 | Fuel Used in Transportation (Inbound Transport) | |

| 5A | Total Transportation Cost actually incurred with respect to process of procuring raw materials, consummables, spares for manufacture of above mentioned export product (Inbound transportation) | Rs |

| 5B | Component of State VAT and Central Excise Duty on fuel used in the Tranportation Cost ((out of 5A above) ) – for Inbound Transportation, in %age | % |

| 5C | Total transportation cost incurred for exported products per UQC for Inbound Transportation | Rs |

| 5D | Total transportation cost on account of State VAT and Central Excise Duty on fuel used in Inbound Transportation per UQC of the Exported Product in Rs | Rs |

| 6 | Fuel Used in Transport (Outbound Transport) | |

| 6A | Total Transportation Cost actually incurred with respect to process of transporting exported product from factory to the gateway port (Out bound transportation) | Rs |

| 6B | Component of State VAT and Central Excise Duty on fuel used in the Tranportation Cost ((out of 6A above) ) – for out bound Transportation, in %age | %age |

| 6C | Total transportation cost incurred for exported products per UQC for outbound Transportation | Rs |

| 6D | Total transportation cost on account of State VAT and Central Excise Duty on fuel used in Outbound Transportation per UQC of the Exported Product in Rs | Rs |

| 7 | Electricity Duty | |

| 7A | Total Electricity consumed in units (KWh) for manufacture of the exported product | in units (KWh) |

| 7B | Rate of Electricity Duty per Kwh | |

| 7C | Total Electricity Duty paid for manufacture of exported products | Rs |

| 7D | Total Electricity Duty paid for manufacture of 1 UQC of the exported product | Rs per UQC |

| 8 | Stamp Duty | |

| 8A | Stamp Duty paid for relevant Export Documents (in Rs) | Rs |

| 8B | Type of Transaction for which Stamp Duty has been paid (please sepcify) – please do not include stamp duty paid of registration of land and lease of immoveable property | |

| 8C | Total stamp duty paid per UQC of the exported product | Rs |

| 9 | State VAT on fuel used in generation of captive power | |

| 9A | Units of power generated by captive power through DG Sets for manufacturing process | Units in KwH |

| 9B | Total cost of Fuel used to generate the captive power through DG Sets | Rs |

| 9C | Component of State VAT on fuel used for generation of captive power , in %age | %age |

| 9D | Total duty paid on account of captive power generation per UQC of the exported product | Rs |

| 10 | Embedded CGST/ SGST on inputs used in the Transport Sector | |

| 10A | Total Transportation Cost Including Inbound Transportation and Outbound Transportation (5A + 5B) | |

| 10B | Estimated Component of embedded CGST/SGST on the cost actually incurred for the Inbound and Outbound Transportation of the exported product , such as on Tyres, Lube oil, Spares etc, in %age | |

| 10C | Total estimated embedded CGST/SGST in Rs per Unit cost of the Exported Product | |

| Declaration by the Manufacturer/ Manufacturer Exporter | ||

| D1 | I declare that the above information is true and correct to be best of my knowledge | Signature with date |

| D2 | Declaration by the Chartered Accountant/ Cost Accountant | |

| I/We declare that the above information has been audited and verified by us based on the Book of Accounts/ other statutory documents | Signature and Seal with date | |

| Name of the Chartered Accountant/ Cost Accountant with Membsership No. | ||

Author Bio

How can we compile or determine & fill up the data in form R3 related to sl. no 2A to 2N at the stage of manufacturer exporter ( Taxes born by the exported product on account of prior stage cumulative taxes on raw material)

Hello Sir,

Form Where I can Download Annexure R1,R2,R3???