With the introduction of new indirect tax, multiple taxable events/elements were done away, and a unified element i.e. “supply” was defined as one of base ignition point of chargeability of tax.

Supply may be of goods or services or both and so is the classification of supply (whether as goods or services) is essential to enable the application of relevant provisions of act enacted distinctly w.r.t. goods and services.

Some supplies can be classified on the face of it, some are “clarified” by schedule-II. But, when there exists a combination of goods or combination of services or combination of goods and services both, GST law coins them either as composite supply or as mixed supply or none and further relevant provisions to cater taxability are thus enacted.

COMPOSITE SUPPLY

Composite supply means a supply made by a taxable person to a recipient

- consisting of two or more taxable supplies of goods or services or both, or any combination thereof,

- which are naturally bundled

- and supplied in conjunction with each other

- in the ordinary course of business, one of which is a principal supply.

For e.g. Machinery (supply of goods) provided along with warranty and maintenance contract (supply of service). Here, there are two or more supplies, naturally bundled and supply of machine is the principal supply.

Principal supply – as per Section 2(90) of CGST Act means supply of goods or services which constitutes the predominant element of a composite supply and to which any other supply forming part of that composite supply is ancillary.

Naturally bundled – Another important factor is that supplies must be naturally bundled. For studying the same we may refer to Education Guide issued by CBEC (now CBIC) in the year 2012 as under –

‘Bundled service’ means a bundle of provision of various services wherein an element of provision of one service is combined with an element or elements of provision of any other service or services. The rule is – ‘If various elements of a bundled service are naturally bundled in the ordinary course of business, it shall be treated as provision of a single service which gives such bundle its essential character’

Further, Para 9.2.4 of Education Guide mentions:

“Whether services are bundled in the ordinary course of business would depend upon the normal or frequent practices followed in the area of business to which services relate. Such normal and frequent practices adopted in a business can be ascertained from several indicators some of which are listed below-

- Perception of the consumer or the service receiver

- Majority of service providers in the in a particular area of business provide similar bundle of services

- The nature of various services

- Advertised as a single package

- Single Price

- different elements aren’t available separately

- different elements are integral to one overall supply

No straight jacket formula can be laid down to determine whether a service is naturally bundled in the ordinary course of business.

Each case has to be individually examined in the backdrop of several factors some of which are outlined above.

M/S SARJ EDUCATIONAL CENTRE (GST AAAR WEST BANGAL)

In the instant case, the Applicant is engaged in supplying food, laundry service, housekeeping service, etc. which are not naturally bundled with the lodging service. All these components are independent of each other and can be supplied separately. It is also evident from the submission of the Appellant that they also provide lodging service without providing food and Day Boarders do not avail laundry services. Therefore, none of the Services are bundled together in a natural way and there appears to be no principal Service.

Calling for a dominant nature test. In Bharat Sanchar Nigam Ltd. v. Union of India [2006] wherein the Hon’ble Supreme Court observed: “The test for composite contracts remains to be – did the parties have in mind or intend separate rights arising out of the sale of goods. The test for deciding whether a contract falls into one category or the other is as to what is “the substance of the contract”.

MIXED SUPPLY

Mixed supply means two or more individual supplies of goods or services, or any combination thereof, made in conjunction with each other by a taxable person for a single price where such supply does not constitute a composite supply.

For example, supply of stationery pack containing crayons, paints, brushes, drawing book etc. supplied at a single price by the seller together as a package is a mixed supply

Primary requisite is to rule out that the supply is a composite supply.

EXAMPLES

BOARDING SCHOOLS

Services provided by boarding school of which primary supply is educational service are coupled with many other services namely providing dwelling units for residence and food. This may be a case of bundled services if the charges for education and lodging and boarding are inseparable

DUAL QUALIFICATION

If a course in college leads to dual qualification only one of which is recognized by law – they are in the nature of two separate services as the curriculum and fees for each of such qualifications are prescribed separately. Service in respect of each qualification would, therefore, be assessed separately. Therefore, they can’t be assessed as bundled services.

COMPREHENSIVE MAINTENANCE SERVICES

In an Advance Ruling, M/s GE Diesel Locomotive Private Limited, Shahjanpur (U.P.), comprehensive maintenance services in relation to railway locomotives is a Composite Supply of maintenance services.

In Hindustan Aeronautics Ltd. v. State of Karnataka [1984]

While executing service, articles have to be used but usage of same doesn’t convert the supply to supply of goods. In every case, the court would have to find out what was the primary object of the transaction and the intention of the parties while entering into it.

RENTING SERVICE

Giving on rent a residential dwelling for dual purpose like first floor used for residence and ground floor for business if a single rent deed is executed it will be treated as a service comprising entirely of such service which attracts highest liability of service tax. In this case renting for use as residence is an exempt service while renting for commercial use is chargeable to tax. Since the latter category attracts highest liability of tax, entire bundle would be treated as renting of commercial property.

E-Square Leisure Pvt Ltd (GST AAR Maharashtra)

-Renting of immovable property would be the main supply and provision of other utilities such as electricity, and water supply, fuel etc. would be in the nature of ancillary supply.

-The utility charges reimbursed by the Applicant from lessee (Applicant has failed to establish themselves as a “pure agent”) forms part of composite supply. Thus, GST is payable at a rate as applicable to the principal supply.

ANCILLARY FREIGHT SERVICES

Services provided along with transportation services such as insurance, packaging, loading, unloading, handling, are supplied in conjunction to principal supply under single contract or single price. Thus they would be covered under composite supply.

ANCILLARY SERVICES ON BOARD

Services like entertainment, massage, catering etc. on board while transport given to passengers is a bundle offered by majority of passage transporters most commonly in airline transport.

HOTEL – ANCILLARY

hotel provides a 4-D/3-N package with the facility of breakfast. This is a natural bundling of services in the ordinary course of business.

HEALTH CARE SERVICES

Referring to the case Tata Main Hospital Vs the State of Jharkhand & Ors. 2007, Supply of medicines, surgical items, X-ray plates, etc. during rendition of healthcare services in hospitals should be classifiable as provision of healthcare services and not as sale of goods. Dominant intention of Agreement is to render medical services and supply of medicines, surgical items, etc. is incidental to such supply.

Advance ruling: Terna Public Charitable Trust (MH)

Supply of medicines, surgical items, implants, consumables and other allied items provided by the hospital through the hospital owned pharmacy as well as food, room for rent.

- to the in-patients is part of composite supply of health care treatment.

- to the out-patients or the attendees, is not part of composite supply of health care treatment

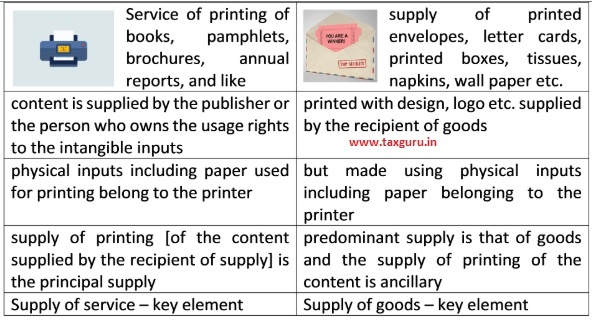

PRINTING CONTRACTS

UPS ALONG WITH BATTERY

AAR (WB) Switching Avo Electro Power Ltd. [2018] UPS supplied with external storage battery is a mixed supply as the strength of the battery, make of a battery or number of batteries is not unique to UPS but it varies as per power requirement of the customer and the storage battery has multiple uses and can be put to different uses. Actual functionality rather than the contract was considered for deciding the issue.

CONSTRUCTION – RESIDENTIAL COMPLEX

Providing service of construction of a dwelling unit in a residential complex, bundled with services relating to the preferential location of the unit, which includes services of floor rise and directional advantage amounts to composite supply under GST. This is subject to conditions stated in Schedule-III.

MILLING WORK & ANCILLARY SUPPLIES

AAR (C.G.) – M/s Taranjeet Singh Tuteja & Brothers. Along with custom milling they will also get the payment towards the transportation of paddy & Rice, usage of gunny bags for packing of Rice and incentives as an additional charge for custom milling. This constitutes composite supply.

Works contracts and restaurant services are classic examples of composite supplies, however the GST Act identifies both as supply of services (refer to schedule II) & chargeable to specific rate of tax mentioned against such services.

TAXABILITY

Columbia Asia Hospitals Private Limited (GST AAR Karnataka)

The two or more supplies of goods or services or both which are naturally bundled in which the principal supply is exempt and others are taxable can be treated as a composite supply of the principal supply if such principal supply is not a non-taxable supply as per sub-section (78) of section 2 of the Central Goods and Service Tax Act, 2017 and such composite supply with the principal supply being exempt supply would be treated as an exempt composite supply.

M/s. Kerala Forest Development Corporation Ltd. (GST AAR Kerala)

Tax liability under GST for the tour packages, which are providing to guests by way of separate services like accommodation, serving food and beverages, service of authorized guides, trekking accessories etc. against separate invoices.

In case where a supply involves supply of both goods and services and the value of such goods and services supplied are shown separately, the goods and services would be liable to tax at the rates as applicable to such goods and services separately.

TIME OF SUPPLY

- Composite supply: The key element in a composite supply is “the principal supply”. So, if in the composite supply the main/principal element is supply of goods then accordingly relevant provisions related to time of supply of goods shall be considered into account. Similarly provisions of TOS of supply of service would apply if principal supply is supply of services.

- Mixed supplies The key element in a composite supply is “supply of a service liable to tax at higher rates than any other constituent supplies”. So if in a mixed supply, supply of service is taxed at higher rate amongst others then accordingly relevant provisions related to time of supply of services shall be considered into account. mutatis mutandis if supply of goods is taxed at highest rate among others in a mix of multiple supplies.

Classification of two or more supplies as composite or mixed or none of them is essential regarding their taxability. Above provisions and examples do let us have a fair picture of its understanding. Still, there’s no limit to possibilities of contrary arguments and to cater taxability each case has to be dealt individually.