Case Study Leading To Some Pertinent Anomalies Due to GSTN Common Portal Designing Deficiencies

In this article ‘SHARNAM Legal Team’ has through a practical experience based on a specific Case Study tried to raise some pertinent inconsistencies or glitches due to GSTN Common Portal (Web-Portal) designing defects. GSTN might have done a commendable job to help Ministry of Finance or CBIC and the States to administer the intricate provisions of GST Law as an interface between the assessee tax payer and the Government, but at some places GSTN have made some significant mistakes in analysing and converting the provision of GST Law into Web Portal driven by the software.

Since, the implementation of the new regime of GST w.e.f. 1st July 2017 the proactive approach of the Government alongwith GST Council is regularly upgrading the provisions of the GST Law by large number of amendments or clarifications, but the GSTN common portal even though an IT platform has not been able to match the spirit of removing the difficulties or intricacies in the administration of GST Law through their platform. GSTN common portal is under criticism and attack since very beginning due to which the system of gathering information of business transactions from the registered dealers by way of Monthly Return GSTR-1 or GSTR-2 or GSTR-3 have miserable failed and Government have to withdraw the implementation of required return GSTR-2 and GSTR-3 which has shaken the strength of GST which was envisaged and passed by the Parliament. Due to the failure of GSTN common portal, the country have lost a very unique opportunity of being a Game Changer for its economy. The desired jump in the economy or increase in GDP as expected by accredited economist including the Government after the implementation of GST from 1st July 2017 had not been felt at all during the last more than 2 years. GSTN also needs to be tax payer friendly which is the foremost aim of its creation. The tax payer must feel ease of doing business rather than futile running from post to pillar and ultimately to the rescue of Hon’ble High Courts in such large numbers as the Nodal Officer or the Jurisdictional Officer are not able to resolve major problems of the assessee creating decent among the tax payers leading to non-compliance in many circumstances.

In the interesting discussions below, we have thrived to decipher some of the intricate issues which have been faced by many of the registered dealers including the one whose Case Study is being taken to understand the factual situation and the problems faced by the assessee including their possible solutions. In the end some points to ponder have been left for the readers to ultimately solve not only these issues but many such similar issues.

1. TABLE 6B and TABLE 6C OF PRESCRIBED FORMAT GSTR-1 AS PER RULE 59(1) WRONGLY MERGED WITH TABLE 4 (4A, 4B, 4C) ON GSTN PORTAL LEADING TO PROBLEM IN DECLARATION OF TRANSACTIONS / COMPLIANCE

ISSUE 1 OF THE CASE – SEZ Transactions of Table 6B inadvertently punched in Table 6A of GSTR-1, deletion of such data from Table – 6A and addition of such data in correct Table 6B of GSTR-1.

SL Observations:

As per the prescribed Form of GSTR-1 under Rule 59(1) as per Notification No. 3 /2017 dated 19 .06.2017:

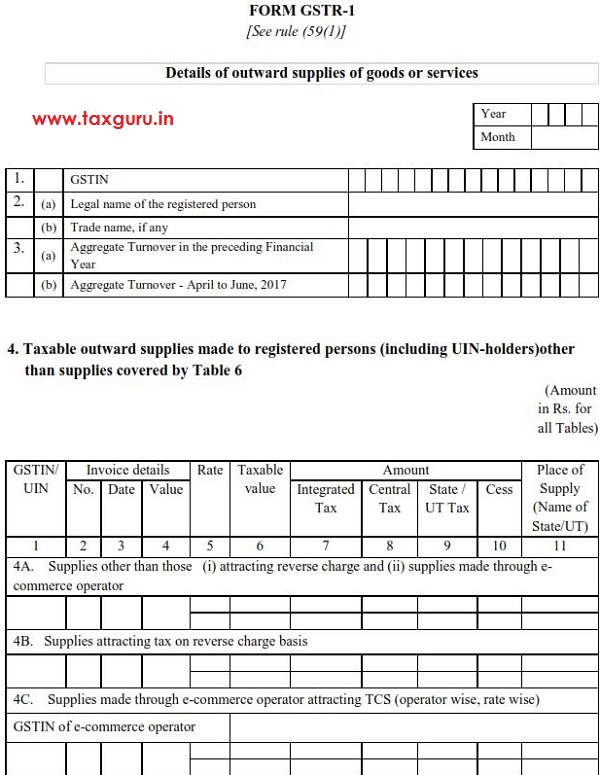

Table 4 of GSTR 1 – Taxable Outward Supplies made to registered persons (including UIN holders) other than supplies covered by Table 6. Under this table three sub tables i.e. Table 4A – Supplies other than those(i) attracting reverse charge (ii) supplies made through e-commerce operator, Table 4B – Supplies attracting tax on reverse charge basis , Table 4C – Supplies made through e-commerce operator attracting TCS (operator wise, rate wise).

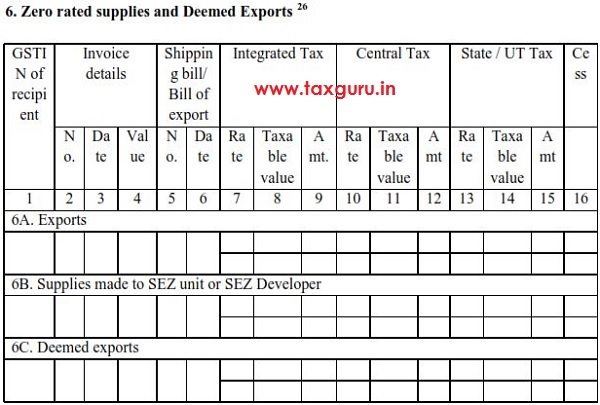

Table 6 of GSTR-1 – is for declaring outward transactions pertaining to Zero rated supplies and Deemed Exports. Under this table three sub tables i.e. Table 6A – Exports Transactions, Table 6B – Supplies made to SEZ Unit or SEZ Developer, Table 6C – Deemed Exports.

Position on GST Portal: Table 6B & Table 6C of GSTR-1 are merged with Table 4 (4A, 4B, 4C).

SL Comments: The taxpayer is to declare the outward supplies made to SEZ under Table 6B of GSTR-1 which has been merged with Table 4 which already consists of (4A, 4B, 4C) on the GST portal whereas Table 6A shows the Export Invoices while 6A and 6B, both are parts of Table 6 as per prescribed format of GSTR-1 under the Rules. Further in the main heading of table 4 it has been mentioned as ‘Taxable Outward Supplies made to registered persons (including UIN holders) other than supplies covered by Table 6’. The inclusion of details to be furnished in Table 6B and 6C as per prescribed format under Rule 59(1) is wrongly required to be filled in the web portal under main block of Table 4 which is contrary to the Rules. Any common man / taxpayer may get confused while punching the details in GSTR-1 on GST Portal as the Format of Form of GSTR-1 on GST Portal differs from the prescribed format as given under the Rule 59 CGST, 2017.

Further, there is no provision in the GST portal to ‘delete’ or ‘shifting to correct table’ of any entry once declared wrongly in a particular table due to confusions like above. Transactions punched in a wrong table may lead to creation of Tax Demands, Mis-match of data between Monthly Returns and Annual Return as well as reversal of ITC, which is leading to filing of multiple Writ Petitions before the Honourable High Courts through the country increasing the litigation which is against the spirit of GST i.e. reducing litigation and creating ease of doing business.

2. TABLE 6A OF GSTR-1 REQUIRES CERTAIN INFORMATION AS MANDATORY FOR MATCHING AND VERIFICATION OF CORRECTNESS OF ZERO RATED TRANSACTIONS

ISSUE 2 OF THE CASE: Export Transactions of Table 6A of GSTR-1: To Add / Correct Shipping Bill, Port Code, Invoice number, Invoice Date as well as mode of payment of tax i.e. with payment or without payment (LUT) etc. (As the time period to correct such data had lapsed on 30.04.2019 while time for filing Annual Return for Financial Year 2017-18 has been extended till 30.11.2019 – these time limitations should coincide for reconciliation and correct filing of the Annual Return).

Sharnam Legal Observations:

As per the prescribed Form of GSTR-1 under Rule 59(1) as per Notification No. 3 /2017-Central Tax dated 19 .06.2017:

Table 6 of GSTR-1 – is for declaring outward supply transactions pertaining to Zero rated supplies and Deemed Exports. Under this main table three sub tables i.e. Table 6A – Exports Transactions, Table 6B – Supplies made to SEZ Unit or SEZ Developer, Table 6C – Deemed Exports have been separately provided.

Position on GST Portal: Table 6A – Export Transactions

–

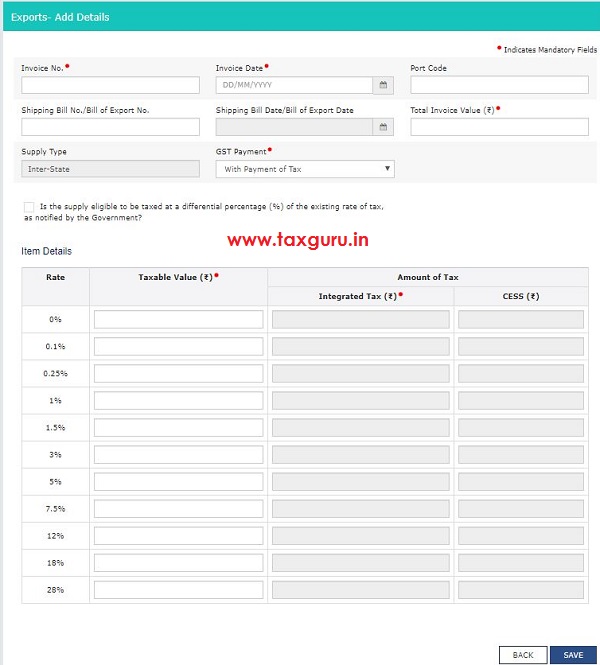

Sharnam Legal Comments : The taxpayer is to declare the outward Export supplies under Table 6A GSTR-1 wherein the taxpayer has to punch the following details Invoice Details – Invoice Number , Invoice Date , Invoice Value ; Shipping Bill / Bill of Export Details – Number and Date (in case of Goods Exported); Port Code (in case of Goods Exported) ; GST Payment Details (With payment of Tax or Without payment of Tax); Item Details – Rate (0%, 0.1%, 0.25%, 1%, 1.5%, 3%, 5%, 7.5%, 12%, 18% or 28%) Taxable Value, Amount of Tax (Integrated Tax, Cess)

The taxpayer has to furnish the complete data in order to get his transactions details transmitted / matched from GST Portal to ICE Gate Portal (details as per Shipping Bill), The Portal however till date doesn’t makes it mandatory to fill Shipping Bill Details, Port Code Details, due to which the data doesn’t transmit from GST Portal to ICE Gate Portal and the refund on account of Export is blocked or not processed. Further, the software/ interface designers at GSTN could have made a simple check box system for this particular Table wherein Type of Outward Supply of Export whether Goods or Services. The nature of Export Supply between Goods and Services is also necessary as the Act and the Rules as well as the Procedure laid down for two nature of supplies are distinctly dealt in the GST Law.

In case of Export of Goods the details of Shipping Bill Number, Shipping Bill Date, Port Code, Invoice Number (as declared on Shipping Bill / Bill of Export), Invoice Date (as declared in Shipping Bill / Bill of Export) is to be mentioned necessarily, then only the data gets transmitted from GST Portal to ICEGATE Portal and could be matched for processing of the Refunds or verification of the Export transactions. Further, in case of Services exported Port Code, Shipping Bill details or Bill of Export details are not required and there is lot of confusion regarding Refund in case of payment of GST while making such transaction as the data is not required to be transmitted or matched with ICEGATE.

It is pertinent to note that the Refund in the case of Export of Services is to be processed and finalised only by GST Authorities with no requirement or involvement of Custom Authorities or ICEGATE Portal.

Due to lack of distinction between declaration of Export Supplies for Goods or Services, the verification of transactions pertaining to one nature keeps pending and adding up in the mis-match list or failed Invoices list which is one of the reasons for pending or delayed Refunds in case of Export of Services with payment of Tax.

Further if the Export transaction is made under LUT and the relevant Export Invoice is categorised under Mismatch or failed Invoices list and the Taxpayer has adjusted/ availed the ITC on Inputs with Domestic Outward Supply instead of claiming refund under Exports made without payment of Tax, then such ITC may be asked to be reversed as the Transaction of Export is not matched with ICEGATE Portal.

Further such type of corrections should be allowed to be made in Annual Return or at any time before filing of Annual Return as these are mere procedural corrections which impacts the cash flow of the taxpayer.

Table 6A of GSTR-1 depicts certain fields as mandatory, but not all. Shipping bill number and port code are non- mandatory fields, which are often not filled by assesse/ taxpayer. The same happened in the current case where petitioner skipped filing these non-mandatory fields and it led to mismatch of data as declared in Table 6A with the data punched by Customs Officers at Ports on the ICEGATE portal. This has led to blocked refunds for the petitioner and has significantly impacted the cash flow of the petitioner and has dissolved the purpose of GST i.e. ease of doing business.

The list of ‘rates of taxes’ under item details is not provided under the prescribed Form GSTR-1 as per Rule 59(1). The ‘item-wise rate of taxes list’ is probably the creation of GSTN itself for providing some ease to the taxpayers filing the Return, but such list of rates of taxes without complete or sufficient information about the rate regardless of the description for riders / conditions for such rates like 0%, 0.1%, 0.25%, 1%, 1.5% as well as in some cases even 5% does not allow any ITC or refund.

There is no distinction between 0% Vs. ‘Zero’ Rated for Export/ SEZ Vs. Deemed Export Vs. Nil Rated as per Schedule Vs. Exempt Supplies as per Notification No. 2/2017 Central Tax (Rate) dated 28.06.2017etc which creates confusion and errors in filing up of the respective figures for the Turnovers pertaining to different kinds of Supplies identified by such terminology which ultimately has the same monetary effect as far as outward supply is concerned. This deficiency of required information in the GSTN web portal for Return filing is leading to inappropriate declarations made by assesses throughout the country resulting in blocked refunds and availment of ITC.

In some cases the Taxable turnover declared in 0% wrongly due to the confusion that 0% means Zero Rated and not Nil- Rated or Exempt Supplies, the ITC availed by the taxpayer will be asked to be reversed with interest and penalty when the matching is done after filing of Annual Returns by the Departmental Audit team.

3. AMENDMENT IN RETURN SHOULD INCLUDE SHIFTING OF TRANSACTION FROM ONE TABLE TO ANOTHER TABLE IN THE SAME RETURN AND DELETION OF THE TRANSACTION FROM THE WRONG TABLE

ISSUE 3 OF THE CASE: B2B Transactions inadvertently punched in B2C Large Table of GSTR-1, deletion of these transactions from B2C Large Table of GSTR-1 as the petitioner had re-declared these transactions in his December 2017 return correctly in B2B Table of GSTR-1, resulting in increase of Total outward Supplies made during the F.Y. 2017-2018.

Sharnam Legal Observations:

As per the prescribed Form of GSTR-1 as per Notification No. 3 /2017-Central Tax dated 19 .06.2017:

Table 4 of GSTR 1 – Taxable Outward Supplies made to registered persons (including UIN holders) other than supplies covered by Table 6. Under this main table three sub tables are prescribed i.e.

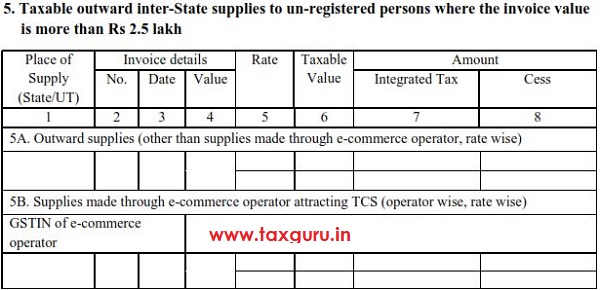

Table 5 of GSTR 1 – Taxable Outward inter-state supplies to unregistered persons where the invoice value is more than Rs 2.5 Lakh. Under this table two sub tables are prescribed i.e.

Position on GST Portal: Table 4 (4A, 4B, 4C) and Table 5 (5A & 5B).

Sharnam Legal Comments: The taxpayer should declare the B2B inter-state outward supplies made under Table 4A of GSTR-1 on the GSTN the portal whereas inadvertently the taxpayer kept on declaring B2B transactions in Table 5A on GSTN portal for a period of four months for August 2017 to November 2017 at the initial stage of introduction of GST. The GSTR-2A was made available with a delay due to technical reasons on the GSTN Portal for the first time to Taxpayers in the month of November 2017. After the registered buyers of the taxpayer’s goods verified the transaction from the available GSTR-2A for the first time made available in November 2017, then they informed the taxpayer that they cannot find and verify the Invoices in their GSTR-2A and insisted the taxpayer for correction of data / declaration of transaction data in the correct Table 4A of GSTR-1 so that the registered Buyer can rightfully claim ITC, the second declaration made under pressure of the transactions in correct column led to double declaration of the same transactions in GSTR-1 for the relevant months which created a mis-match between GSTR-1 and GSTR-3B of the Taxpayer. The gross turnover of the Outward supplier thus, increased due to double declaration as there was no option for shifting of the wrongly declared transaction from one table to another table for rectification in accordance to the correct nature and facts of the transaction.

Further, there is no provision in the GST portal to delete any entry once declared wrongly in a particular table. Transactions punched in a wrong table may lead to creation of Tax Demands, Mis-match in between GSTR-1 and GSTR-3B and accordingly in the Annual Return.

Hence, the mistakes made by the taxpayer could not be rectified/ shifted, so to make ITC available to the registered buyer, taxpayer added the details in Table 4A along with earlier wrongly filled transaction in B2C Large in Table 5 in the month of December 2017. This led mis-match of total outward taxable turnover as declared in GSTR-1 v/s. Tax paid on Total Taxable Turnover in GSTR-3B for the month and further led to increased total turnover of the taxpayer.

4. AMENDMENT IN RETURN SHOULD INCLUDE SHIFTING OF TRANSACTION FROM ONE ROW TO ANOTHER ROW OF THE SAME TABLE OF THE RETURN AND DELETION OF THE TRANSACTION FROM THE WRONG ROW

To correctly punch data in Table 3.1 (b) of GSTR-3B as the petitioner has inadvertently punched / uploaded data in Table 3.1 (a) & Table 3.1 (c).

As per the prescribed Form of GSTR-3B as per Notification No. 3 /2017 dated 19 .06.2017:

GSTR 3B – The taxpayer has to declare the tax payable in GSTR-3B.

Sharnam Legal Comments:

Under Table 3.1 of GSTR-3B requires information on Outward Supplies and Inward Supplies liable to reverse charge. The petitioner wrongly fed the data in 3.1 (a) which is Outward Supplies other than Zero rated, Nil rated and Exempt as well as in 3.1 (c) which is Other Outward Supplies including Nil rated and Exempted. The petitioner was legally required to fill the data in 3.1 (b), an outward taxable supplies of Zero rated for the Exports Transactions declared under Table 6 (6A, 6B, 6C) of GSTR-1. The fundamental difference in Zero rated, Nil rated and Exempt are not clear among the taxpayers/ business man, common man as well as consultants. This has led to huge confusion among people leading to wrong punching of data on the GST portal and in cases has also led to mis-match of data between GSTR-1 and GSTR-3B as well as also led to blockage of refunds, non–processing of refunds and rejection of refunds. The same happened in the current situation. This caused huge blockage of GST refund on the Export Transaction and impacting the cash flow of the taxpayer, further leading to inconvenience in conducting the business and carrying out routine work.

There is no distinction between ‘Zero’ Rated for Export/ SEZ Vs. Deemed Export Vs. Nil Rated as per Schedule Vs. Exempt Supplies as per Notification No. 2/2017 Central Tax (Rate) dated 28.06.2017 etc which creates confusion and errors in filing up of the respective figures for the Turnovers pertaining to different kinds of Supplies identified by such terminology which ultimately has the same monetary effect as far as outward supply is concerned. This deficiency of required information in the GSTN web portal for Return filing is leading to inappropriate declarations made by assessees throughout the country resulting in blocked refunds and availment of ITC.

In some cases where the taxpayer has made an Export transaction and has declared the same in GSTR-1 rightly but while making the declaration and payment through GSTR-3B, the taxpayer declares the Taxable turnover wrongly in 3.1(c) {Other Outward Supplies (Nil Rated, Exempted)} instead of declaring in 3.1(b) {Outward Taxable Supplies (Zero Rated)}, then the taxpayer will not be entitled to any refund or availment of ITC as the Act and the Rules very clearly restrict ITC and refund on Nil Rated and Exempt Supplies. Further, if the taxpayer declares the Zero rated transaction in 3.1(a) [Outward Taxable Supplies (Other than Zero Rated, Nil rated and exempted)] instead of 3.1(b) [Outward Taxable Supplies (zero rated)], then the taxpayer maybe liable to deposit GST on the Export transaction made under LUT as he declares his export turnover along with domestic turnover under the Outward Taxable Supplies (Other than Zero Rated, Nil rated and exempted). Further the tax payer may not receive his refund or maybe denied refund due to the mistake he committed while punching the total taxable value in the wrong row of Table 3.1. As well as if the taxpayer has paid the GST through his ITC available then he may be asked to reverse with interest and penalty when the matching is done after filing of Annual Returns by the Departmental Audit team.

Even though the government have issued directions through circular to process the blocked interim Refunds in the above referred circumstances but that is not the correct solution as whenever the returns are analysed by the jurisdictional officer or Audit Team, the issue of mis- match between GSTR-1, GSTR-3B vis-a-vis Annual Return shall naturally crop up to the detrimental of the assessee.

Practical Scenario as developed on the above issues wherein the Taxpayer was forced to approach the Hon’ble High Court as the Government of India or the GST Council or the GSTN or CBIC has not provided any relief or resolution:

In brief the petitioner had made inadvertent errors in punching of data in its GST monthly returns (GSTR-1 & GSTR-3B), the petitioner tried making rectifications / corrections in the wrongly filed transaction details but the portal did not allow rectifications / corrections as well as deleting any previous entries resulting in double declaration of total taxable turnover, mis-match in GSTR-1 and GSTR-3B, blockage refund in case of Export Transaction.

On such problematic issues, the Petitioner stated its grievance to the GSTN Portal, ICEGATE as well as to the Jurisdictional Officer to allow him to make necessary corrections before the filing of GSTR-9 so that the Annual return could be filed correctly. As there was no guidance, no help and support to make corrections provided by the GSTN, ICEGATE and the Jurisdictional Officer, the petitioner had no choice but to approach the Hon’ble Punjab & Haryana High Court.

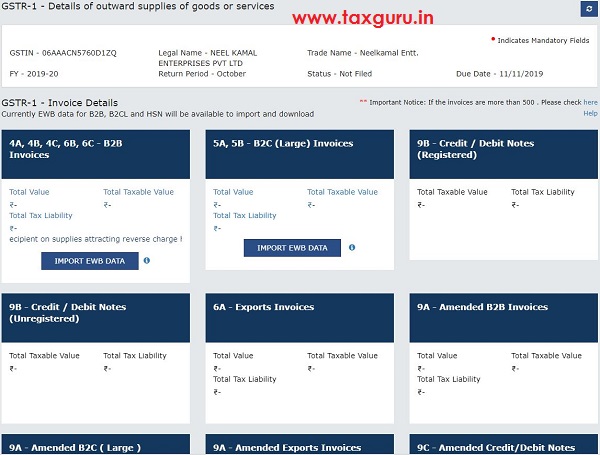

Case Details: M/s Neelkamal Enterprises Pvt. Ltd. V. Union of India and others

Case No. CWP-21651-2019

Court: Punjab & Haryana High Court

Counsel for the Petitioner: Prateek Gupta, Advocate (Partner & Counsel – Sharnam Legal), Sandeep Goyal, Advocate & Rishab Singla, Advocate

Interim Relief given by the Court

Punjab & Haryana High Court allowed the Petitioner to correct its GST Returns (GSTR-1 & GSTR-3B) on account of inadvertent errors in punching of data in its monthly returns for F.Y. 2017-2018, the court had directed the GST Authorities on an earlier hearing to verify by the Jurisdictional Authority the transactions of the petitioner which needs to be corrected / revised, on the basis of affirmative report furnished to the High Court after verification of transactions by the GST Authorities, the court has allowed the petitioner to correct its data on GSTN portal and the court has directed GSTN to open the portal in petitioners case however in the meantime the court permitted the petitioner to manually submit revised returns by making necessary corrections in the GSTR-1, GSTR-3B and also Annual Return for assessment year 2017-18 by the closing date subject to decision of the Writ Petition. The court also observed that “the problem persisting is that such genuine corrections are not being permitted to be corrected in the GST Portal leading to serious consequences of double tax liability along with interest and penalty hence, either the portal has to be re-programmed to permit removal of such restrictions or the assessees like the petitioner have to be permitted to file their annual returns manually which the GST Scheme does not permit. The issue requires some serious reconsideration by the GST Council, the Nodal Agency for administering the provisions of the GST Scheme.”

Sharnam Legal – Comment / Observation

This is a unique case where the Honourable High Court has gone into the details of transaction to understand the errors done by the petitioner as well as the department and portals involved. The court has given the scope to make changes to the errors committed by the assesse, considering that there is no intention to evade tax. The errors are proven to be reasonable that can be committed by any common man as GST is a new law. The court, on such examination of ‘intention’ through evidences, records and data maintained has given leverage to the assesse and asked GSTN to re-open the portal for correction of data entered.

Let’s Ponder!

GST has been executed with aim to boost economy and ease the business. But looking at the above complex return filing system and execution of the law, the number of litigations have been on sudden rise. This is causing unnecessary litigations before the High Courts.

Also, it is very important to note that format of GSTR-1 as discussed above is not same as that given under the CGST Rules, 2017.

The question which arises is whether the GSTR-1 Return filed/ uploaded by registered dealers on the GSTN web-portal since July 2017 is in the prescribed Form of Return GSTR-1 as per as per section 39(1) of CGST Act and Rule 59(1)? If not, then had the registered dealers properly complied the CGST Act and Rules 2017?

The Government / CBIC should provide a clarification under which notification or circular or ROD they have allowed the GSTN to change the format on GSTN Web-Portal for the prescribed GSTR-1 Return?

The government must fix a time limit for GST “IT Grievance Redressal Mechanism” Committee to act upon the directions in the order of the Hon’ble High Courts so as to allow the necessary relief to the tax payer immediately as in many cases it has been observed that the “IT Grievance Redressal Mechanism” Committee do not take any action of redressal of the issue and sit upon, inspite of the clear instructions and order of the Hon’ble High Courts which are made after getting the verification of the transactions.

Prateek Gupta

Advocate – Tribunals & High Courts

Partner & Counsel

SHARNAM Legal

Mobile: +91-9654140247

Landline: +91120-4118856