MINISTRY OF CORPORATE AFFAIRS

NOTIFICATION

New Delhi, the 16th May, 2017

G.S.R. 470(E).—In exercise of the powers conferred by sub-sections (1) and (2) of section 79 of the Limited Liability Partnership Act, 2008 (6 of 2009), the Central Government hereby makes the following rules further to amend the Limited Liability Partnership Rules, 2009, namely:—

1. (1) These rules may be called the Limited Liability Partnership (Amendment) Rules, 2017.

(2) They shall come into force with effect from 20th May, 2017.

In the Limited Liability Partnership Rules, 2009 (herein after referred to as the Principal Rules), in rule 37, after sub-rule (1), the following sub-rule shall be inserted, namely:—

“(1A) The limited liability partnership referred to in clause (b) of sub-rule (1) of rule 37 shall,—

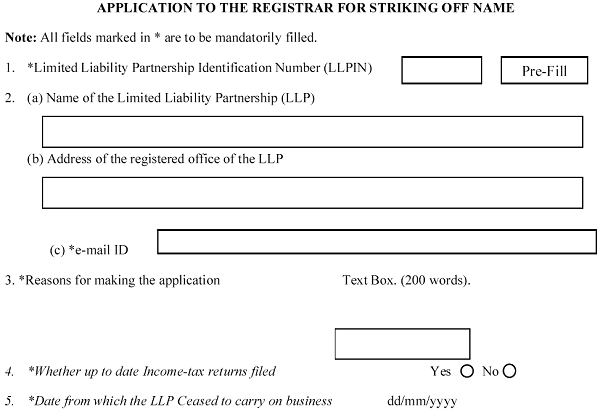

(I) file overdue returns in Form 8 and Form 11 up to the end of the financial year in which the limited liability partnership ceased to carry on its business or commercial operations before filing Form 24;

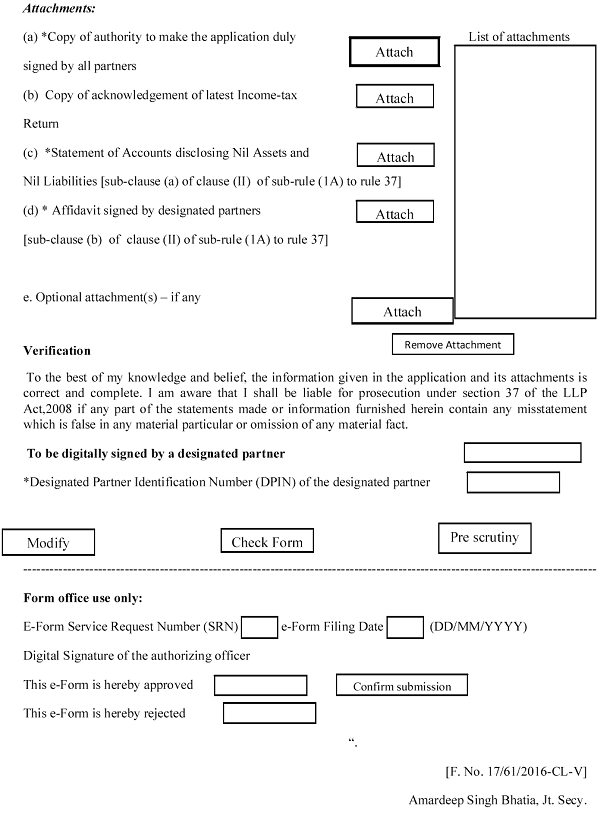

(II) enclose along with Form 24,—

(a) a statement of account disclosing nil assets and nil liabilities, certified by a Chartered Accountant in practice made up to a date not earlier than thirty days of the date of filing of Form 24;

(b) an affidavit signed by the designated partners, either jointly or severally, to the effect,—

(i) that the Limited Liability Partnership has not commenced business or where it commenced business, it ceased to carry on such business from (dd/mm/yyyy);

(ii) that the limited liability partnership has no liabilities and indemnifying any liability that may arise even after striking off its name from the Register;

(iii) that the Limited Liability Partnership has not opened any Bank Account and where it had opened, the said bank account has since been closed together with certificate(s) or statement from the respective bank demonstrating closure of Bank Account;

(iv) that the Limited Liability Partnership has not filed any Income-tax return where it has not carried on any business since its incorporation, if applicable.

(c) a copy of the acknowledgement of the latest Income-tax return filed under the Income-tax Act,1961 (43 of 1961) and the rules made thereunder for the time being in force, where the limited liability partnership has carried out any business and has filed such return.

(d) copy of the initial limited liability partnership agreement, if entered into and not filed, along with changes thereof in cases where the Limited Liability Partnership has not commenced business or commercial operations since its incorporation.

Explanation.—The date of cessation of commercial operation is the date from which the Limited Liability Partnership ceased to carry on its revenue generating business and the transactions such as receipt of money from debtors or payment of money to creditors, subsequent to such cessation will not form part of revenue generating business.”

3. In the Principal Rules, for Form 24, the following Form shall be substituted, namely:—