Month: July 2020

1,516 articlesIncome Tax

Income Tax

Taxation of Joint Venture Business

Income Tax

Income Tax

TDS Certificates – Detailed Discussion

Goods and Services Tax

Goods and Services Tax

Advance Ruling | Section 95 to 99 | CGST ACT 2017 | Part I

Goods and Services Tax

Goods and Services Tax

Landmark Judgement by Gujarat HC on refunds on account of inverted duty structure under GST

Goods and Services Tax

Goods and Services Tax

GST E-Invoicing – Enhancement of Aggregate Turnover

Income Tax

Income Tax

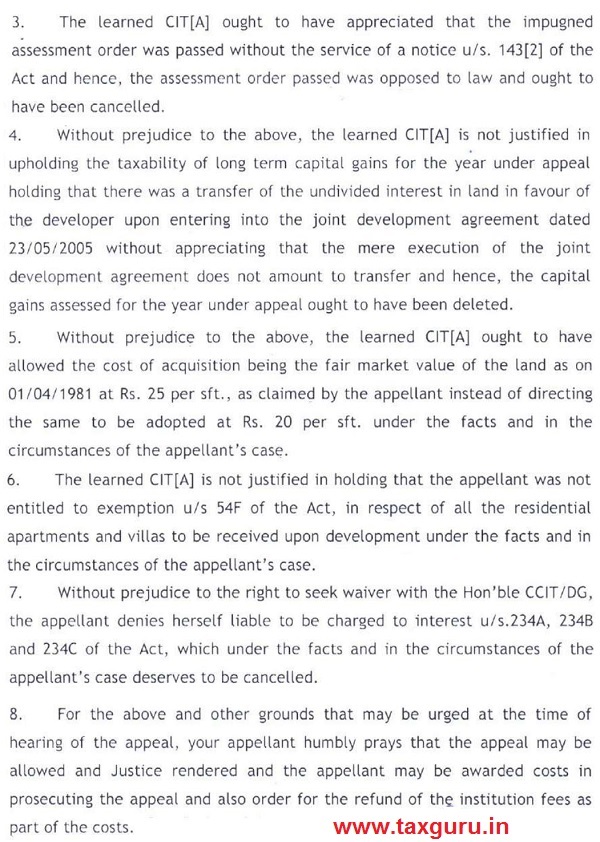

Section 54F deduction restricted to only one residential property

CA, CS, CMA

CA, CS, CMA

ITC reversal for GST payable under RCM

Income Tax

Income Tax

A flat buyer acquire vested right in flat upon payment of consideration & execution of allotment letter

Income Tax

Income Tax

Whimsical Explanation to Section 194O

Income Tax

Income Tax