Case Law Details

During the course of assessment proceedings, it was noted by the assessing officer that assessee company had made payments of Rs. 2.26 crores during the year under consideration to Radio Jockeys (RJs) and deducted TDS on this payment @ 10 per cent under section 194J considering its as payment of professional/ consultancy charges. The assessing officer examined the terms of the agreement made with RJs and inferred that there was an employer-employee relation between the assessee and RJ, therefore payments of RJ should have been subjected to deduction of TDS under section 192 by treating is as salary and not under section 194J by treating is as professional/ consultancy charges. Accordingly, he issued show-cause notice to the assessee. The assessee submitted detailed reply analyzing various clauses of the agreement in detail to argue that contents of the agreement with the RJ clearly suggest that these are exclusive professional contract. It was also submitted that RJs have raised invoices on the assessee company for the service rendered by them.

But, assessing officer was not convinced with the argument of the assessee, and after analyzing agreement with RJs, it was held by the assessing officer that TDS should have been deducted by treating the impugned payment as salary under section 192.

It is noted by us at the very outset that it has been pointed out by the assessee that the impugned payments have been shown as part of professional income by the RJs in their respective returns and have been accepted as such by their respective assessing officers. Nothing has been brought on record by the assessing officer or by the learned Departmental Representative before us to contradict this aspect to show whether in any case the said income has been treated as income under the head of salaries. It is also not the case of the assessing officer that ultimately any RJs is left to be assessed by the Department or if any one of them avoided making payment of tax. The case of the assessee, which remains undisputed, is that all the RJs were duly assessed to tax and they have paid taxes and filed their returns as per law. Under these circumstances, it was not justified on the part of the assessing officer to magnify this issue and change the relationship of the assessee and RJs from professional consultant to employee by any inappropriate reading of terms of the agreement. Further, it is noted by us that learned Commissioner (Appeals) has rightly pointed out RJs were not entitled for the various benefits which assessee company’s employees were entitled e.g. provident fund, gratuity, retirement benefits etc. The agreements with them were for a specific period and assessee company was not bound to renew the same. It has also been noted by us that RJs were free to take assignments from any company (except with any other radio broadcasting company). They were not bound to act solely as RJs. Such kind of permissions cannot be given to employee. It is also worth noting that with effect from 1-7-2012, the RJs were liable to pay service-tax on the value of service rendered by them. The assessee supported this fact with the help of sample copies of invoices showing that service- tax was charged by the RJs. Thus, different treatment cannot be given under the income-tax law and service-tax law to decide the nature of the payments.

Further, on examination of various clauses of the agreement, it is noted that neither it is mentioned anywhere that RJ would be employee of the assessee, nor it can be concluded on the basis of holistic reading of the entire agreement that there was any employer-employee relationship between assessee and RJs.

Lastly, it is noted by us that the assessee has made payment by treating it as payment for professional services. Under these circumstances, the assessee was obliged to deduct the TDS under section 194J only.

Full Text of the ITAT Order is as follows:-

These appeals have been filed by the Revenue pertaining to the same assessee for different years involving identical issues. Therefore, these were heard together and being disposed of by this common order.

2. During the course of hearing, arguments were made by Shri Mayur Kisnadwala, Authorized Representatives (AR) on behalf of the assessee and by Shri Vishwas Mundhe, Departmental Representative (DR) on behalf of the Revenue.

3. First we shall take appeal for assessment year 2011-12 filed against the order of learned Commissioner (Appeals) on 18-12-2013 passed against the order under section 201(1)/(1A) of the Act, dated 21-03-2013 on the following grounds :–

“1. The learned Commissioner (Appeals) has erred in law and on facts in holding that the assessee company is not liable to deduct TDS on agency discount under section 194H of the IT Act.

“1. The learned Commissioner (Appeals) has erred in law and on facts in holding that assessee company has rightly deducted tax at source under section 194J of the IT Act, 1961 on payments made to Radio Jockey.

The learned Commissioner (Appeals) has erred in law and on facts in holding that the payment made to Radio Jockey by the assessee is not salary under section 192 of the IT Act.

On the facts and in the circumstances of the case and in law, the learned Commissioner (Appeals) has erred in deleting the interest under section 201(1A) of the IT Act, 1961 determined by the assessing officer as the tax determined has already been deleted by her and interest deletion is consequential to the quantum deletion for which further appeal has been recommended vide ground Nos. (1), (2) and (3).

5. The appellant craves to leave or alter any ground or add a new ground which may be necessary at the time of hearing of the case or thereafter.”

4. Ground No. 1 : Revenue is aggrieved with the decision of learned Commissioner (Appeals) in reversing the action of the assessing officer wherein assessing officer had held that agency discount allowed by the assessee was in the nature of commission and thus liable for deduction of TDS under section 194H of the Act.

4.1 The brief facts are that the assessee company was engaged during the year in the business of operating FM Radio broadcasting stations in 32 Indian cities under the brand name “Radio Mirchi”.

4.2 The assessee company’s principal revenue stream is advertising, which is generated through the sale of air time on assessee company’s FM Radio broadcasting stations. It was noted by the assessing officer that the assessee company had given credit of Rs. 33,10,80,109 to various clients in the forms of agency discount, client discount and volume incentive, on which no TDS was deducted by the assessee. The assessing officer was of the opinion that these amounts were in fact in the nature of commission upon which TDS was required to be deducted as per provisions of section 194H. Therefore, he issued show-cause to the assessee in this regard. In response, it was explained by the assessee that there is no principal-agent relationship between the assessee and the advertisement agency companies, therefore, no agency commissions was paid and thus no TDS was required to be deducted on the payment made by the assessee to the said companies. The relevant part of the reply dated 15-3-2013 is reproduced here under :–

“Entertainment Network (India) Ltd. (ENIL) raises invoice on the agencies for the sale of air time spots in its radio, after allowing discount at the rates mutually agreed upon generally 15 per cent on the gross amount plus the applicable service-tax. The service-tax is levied only on the -1 amount net of discount, The net amount billed after allowing discount is shown as sales in the P&L a/c. The agency pays ENIL the amount billed after deduction of TDS @ 2 per cent under section 194C of IT Act. The billing done to the agency by ENIL is in the form of principal-to-principal relationship.

The agency raises invoice on the ultimate clients’ (advertisers) for the amount billed by ENIL (net of discount) plus the applicable service-tax on the same as reimbursement of broadcasting charges. The agency charges a Media Agency’ Commission at a rate on the ultimate clients on the gross amount of billing done by ENIL plus the applicable service-tax separately. The client (advertiser) pays the agency the commission charged and the reimbursement of broadcasting charges after deduction of applicable TDS. Hence from the above facts, it is very clear the ENIL does not pay the agency any commission, Hence, the provisions of TDS are not applicable on the same. The alleged discount is neither accounted as expenditure in the books of ENIL nor accounted as income in the books of agency.

Reference may be made to decision of Allahabad High Court in the case of Jdgran Prakashan Ltd. Vs. Dy. CIT wherein it was held that (i) To constitute “Commission or brokerage” under section 194H, it is necessary that person receiving payment should be acting as agent and rendering services. The relationship between the assessee and the advertising agency in accordance with the rules is that of a principal to principal because (a) the assessee has no control over the advertising agency, (b) the agency is responsible for payment even if the advertiser has not paid the advertising agency, (c) the advertising agencies are rendering service to the advertisers/ customers and other terms. The “discount” was not “commission”.

Reference may be made to the decision of the Kolkata Income Tax Tribunal where it was held that payment made by an assessee- company to accredited advertising agencies could not be termed as payment of commission, and accordingly no TDS is required to be deducted under the provisions of section 194H of the IT Act, 1961. The accredited agents got advertisement order directly from the advertisers, who thereafter placed order to the assessee on which they received trade discount. The assessee paid trade discount to the advertising agent without deducting TDS. The assessing officer contended that the payment was in nature of commission and liable to TDS under section 194H of the Act. The Tribunal held that the advertising agency was placing orders for advertisement to various newspapers and was being taxed on the profits so made by it, and hence the transactions between the assessee- company and the accredited advertising agencies were on a principal to principal basis and not on as principal to agent basis. Hence, it was held that the payments by the assessee- company- to accredited advertising agencies could not be termed as payments of commission.”

4.3 But assessing officer was not satisfied with the submissions of the assessee and it was held by him that TDS was required to be deducted by the assessee on the amount of disallowance (sic-discount) to be allowed to the advertising agencies. Therefore, assessing officer worked out the liability of the assessee under sections 201(1) and 201(1A) by observing as under :–

“8. In the instant case the assessee company is engaged in running Radio FM services in different cities of the country. The company’s principal revenue stream is advertising. Adverting revenues are generated through the sale of air time of the company’s FM Radio ‘broadcasting stations. For the sale of air time the assessee company bills the agency/client after allowing the deduction of 15 per cent, which is mutually agreed upon. This 15 per cent amount is retained by the agency on account of the services provided to the principal (assessee) and the rest 85 per cent is paid to the assessee. The 15 per cent commission retained by the agencies as mentioned in the list provided is for the services provided in the form of bringing advertising revenue for the assessee. Thus, the agency is acting as on agent for the assessee company aid the 15 per cent retained is nothing but commission/brokerage. From the said also the relation between a principal and agent is proved.

9. In this context, it is important to note that Explanation to s. 194H reads a under :-

‘commission or brokerage’ includes any payments received or receivable, directly or indirectly, by a person acting on behalf of another person for services rendered (not being professional services) or for any services in the course of buying or selling of goods or in relation to any transaction relating to any asset, valuable article or thing, not being securities.

10. In view of the above Explanation as well as considering the facts of the case and after due consideration of the assessee submission it is held that assessee company liable to deduct TDS on the retained money Of the agencies which is nothing but commission allowed by the assessee company @ 10 per cent under section 194H. Since the assessee company has not done so, hence the assessee is in default under section and 201(1A). Thus, the total demand in this regard is computed as under.”

4.4 Being aggrieved, the assessee filed an appeal before learned Commissioner (Appeals) wherein detailed submissions were made, which can be summarized as under :–

(i) Amount of discount credit deducted by the assessee from gross amount in the invoices is not a real expense of the assessee.

(ii) Since there was no relationship between the assessee and advertising agencies, provisions of section 194H are not applicable.

(iii) Provision of s. 194H applies to payment of commission.

(iv) Reference was made to the Circular of CBDT No. 715, date 8-8-1995 ((1995) 127 CTR (St) 13) and Circular No. 133, dt. 12-9-1995 (sic) wherein it was clarified that advertisers would be required to deduct tax under section 194C of the Act, on the gross amount of bill including the bill of the Media Agency. Thus, commission income, if at all it has been paid, it has been paid by the advertiser to the assessee and not by the assessee to the agency.

(vi) Once it has been clarified by the board that deduction was required to be done under section 194C by the advertiser while making payment to the agency, then by necessary implication, assessee was clearly not required to deduct tax under section 194H. Because two different persons cannot be required by the law simultaneously to deduct tax on the same transactions, as it will lead to double deduction of tax at source on the same amount.

4.5 It was also alternatively submitted by the assessee that in any case non-deduction of tax was under bona fide belief. Under these circumstances, assessee should not be deemed as assessee in default in view of judgment of Hon’ble Supreme Court in the case of Hindustan Coca Cola Beverages (P) Ltd. Vs. CIT (2007) 211 CTR (SC) 545 : (2007) 293 ITR 226 (SC) and judgment of Hon’ble Bombay High Court in the case of CIT Vs. Kotak Securities Ltd. (2011) 245 CTR (Bom) 3 : (2011) 62 DTR (Bom) 339 : (2012) 340 ITR 333 (Bom). Learned Commissioner (Appeals) considered observations made by the assessing officer as well as detailed submissions of assessee and also considered the judgments available on this issue, and held that the amount of discount offered by the assessee could not partake the character of commission as envisaged under section 194H and therefore assessee was not required to deduct tax at source under section 194H on the said amount. Detailed findings of learned Commissioner (Appeals) are reproduced below :–

“5.3 I have considered the facts of the case the submission of the appellant and the order of the assessing officer. The dispute before me is whether the amount shown as 15 per cent trade discount is discount or commission and whether tax is required to be deducted under section 194H of the IT Act. The distinction between commission and discount is subtle and loosely speaking sometimes the words are interchanged. Therefore, before deciding the issue, it is very important to understand the meaning of two words commission can be defined as under :-

(i) ‘Commission’ is percentage or allowance of factor or agent for transacting business for another.

(ii) ‘Commission’ is compensation paid to another for service rendered in the handling of another’s business or property and based proportionately upon the amour or value thereof.

(iii) ‘Compensation is paid for works measured by results achieved,’

(iv) ‘Commission’ generally denotes the compensation which a person can receive on sales.’

A producer or manufacturer of goods generally does not sell his goods directly to the ultimate consumer. There are agents who purchase the goods from the manufacturer and sell them to the consumer. In a sense, such agents bring the manufacturers and the consumers together, for transaction. The remuneration which an agent gets for his services in the transaction is called commission. Most of the business transactions are made through intermediate persons.

Trade discount is an allowance or rebate from the listed price granted by the seller to buyer. In other words, trade discount is an allowance made from the full invoice price to a customer who buys goods in the ordinary course of trade. For example, a wholeseller may invoice goods to a retailer at the retail selling price less a discount of 25 per cent, which represents the retailer’s gross profit.

From above it is observed that the discount is for the customer or the buyer and commission is to the agent/middlemen. Whether the appellant has appointed the advertising agency as its agent is a question of fact and has to be determined based on the prevailing evidence.

The nature of work of the appellant and’ advertiser is completely different. Appellant is in the business of operating radio channel and sells its air time to generate revenue whereas the advertising agency is ir the business of creating, advertisement and books air time, on radio/TV and space in print media on behalf of the advertisers.

In this backdrop let us analyze the transaction of the appellant. The appellant to sell its air time has entered into two types of transactions. One it sells directly to the advertiser and the other it sells to advertiser through the advertising agency. To both it is giving a discount of 15 per cent as per its tariff card which is normally accepted prevailing practice in the industry.

When the air time is sold directly to the advertiser and discount of is given which, in my considered opinion, cannot be held, as commission. This is due to the reason that no middleman agent or intermediary is involved. The sale is directly made from seller to the buyer. Therefore, the agency is, count credit aggregating Rs. 58,69,73 provided to clients (i.e. advertisers) directly, cannot be treated as commission provided for in the form of bringing advertisement revenue to the appellant. The assessing officer is accordingly directed to not trend the, assessee in default on this amount and delete the addition under section 201(1) on this amount of Rs. 58,69,793.

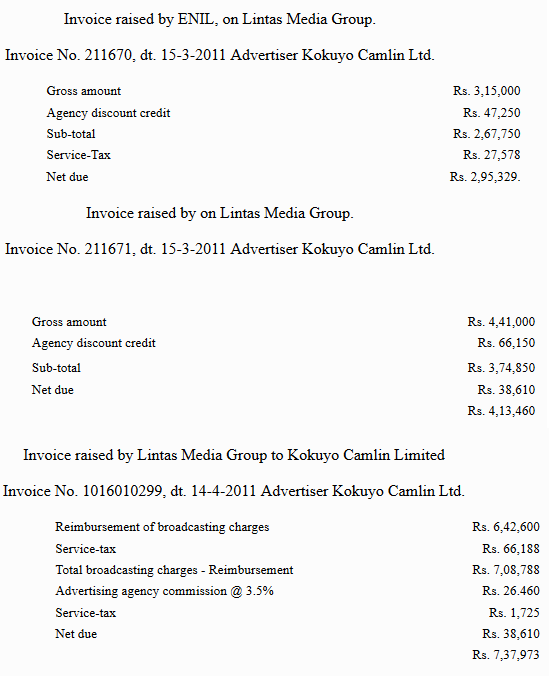

5.4 The other type of transaction corresponds to air time sold to advertisers through advertising agency. In this transaction to the appellant has given 15 per cent discount on the tariff amount as per industry practice. The appellant has nowhere in its account shown as receivable this 15 per cent agency discount. The agreement between the advertiser and the appellant was perused. None of the clauses of agreement connotes that the appellant has appointed the advertising agency as their agent to bring the advertisement for sale of their air time. There is nothing on record to prove that the advertising agency acted as an agent of the appellant. In this regard the sample of the invoices raised by the appellant as filed was perused and reproduced as under :

5.4.1 Thus from above it is clear that the advertising agency is raising the bill to the advertiser on net amount charged by the appellant i.e. Rs. 6,42,600 (Rs. 2,67,750 + Rs. 3,74,850) and charging separate commission from the advertiser, No commission is charged from the appellant by the advertising agency nor the appellant has given the advertising agency any commission on purchase/ sale of air time. Therefore, no amount is transacted between the appellant and advertising agency which partakes the character of commission. Hence the application of section 194H is not satisfied.

5.4.2 Section 194H talks about the payment to a recipient which is the income by way of commission or brokerage. The commission under the Explanation I to s. 194H is defined in an inclusive manner. ‘Commission under the definition includes payment received or receivable, directly or indirectly, by a person acting on behalf of another person for services rendered (not being professional services) or for any service in the course of buying or selling of goods or in relation to any transaction relating to any asset, valuable article or thing (not being securities). It takes into account a situation where a person renders service to another person for which the person rendering service either receives or is entitled to receive, directly or indirectly, payment from that another person to whom the service is rendered.

5.4.3 Adverting to the fact in the instant case and from facts on record, it is clearly discernible that the advertising agencies are not the agents of the appellant, whether directly or indirectly. They have not received any payment from the appellant directly or indirectly. The agency discount credit given by the appellant is same to the direct advertisers as well as to the advertising agency.

5.4.4 The Hon’ble Gujarat High Court in the case of Ahmodabad Stamp Vendors Association vs. Union of India (2002) 176 CTR (Guj) 193 has made a reference to the distinction between the ‘commission’ and ‘discount’ as explained in law dictionaries and in judicial pronouncement. The definition of commission as given the Black’s law dictionary is that:

‘To recompense, compensation or reward of an agent, salesman, executor, trustee, receiver, factor broker or bailee, when the same is calculated as a percentage on the amount of his transactions or on the profit to the principal. This was further elaborate in the decision of the Weiner Vs. Swales 211 Md 123; is a fee paid to an agent or employee for transacting a piece of business or performing a service.’

5.4 The discount, in general sense is, all allowance or deduction made from a gross sum on any account whatever; in a more limited and technical sense, the taking of interest in advance. It was further elaborated by Hon’ble Court as a deduction from an original price or debt, allowed for paying promptly or in cash.

5.4.6 The Hon’ble Gujarat High Court has also considered the distinction between the commission and discount as explained by the Hon’ble Bombay High Court in the case of Harihar Cotton Pressing Factory v. CIT (1960) 39 ITR 594 (Bom) wherein it has been explained the expression “Commission” has no technical meaning but both in legal and commercial acceptation of the term it has definite signification and is understood as an allowance for service or labor in discharging certain duties such for instance of an agent, factor, broker or any other person who manages the affairs or undertakes to do some work or renders some service to another. Rebate, on the other hand, is a remission or a payment back and of the nature of adduction from the gross amount.

5.4.7 The Hon’ble High Court has also considered the decision of the Hon’ble apex court in the case of Coromandel Fertilizers Ltd. v. Union of India 17 ELT 607 wherein the Hon’ble apex court has applied the aforesaid principles and observed that:

The trader discounts given to the dealers by the manufacturer were held to be liable to be deducted from the price charged to the dealers for the purpose of arriving at the excisable value of the goods, but the commissions given to the agents were held to be, not deductible from the price for the purpose of arriving at the excisable value of the goods.

5.4.8 It is clear from the various decisions as considered by the Hon’ble Gujarat’ High Court that a discount is given from the gross price and it occurs at the instance of sale and purchase between the owner and ‘the buyer, whereas the commission is in the nature of refund or compensation for .performing some task or business by one person on behalf of the other.

5.4.9 In the case in hand, the undisputed fact is that the amount of discount has been reduced from the value of price charged by the assessee from the advertising agency on sale of air time.

5.4.10 The Hon’ble Delhi High Court in the case of CIT v. Idea Cellular Ltd. (2010) 230 CTR (Del) 43 : (2010) 35 DTR (Del) 219 : (2010) 325 ITR 0148 (Del) has also discussed the definition of commission as well as discount and also the difference, between two terms/ expression. There is no dispute that there is no necessity for a formal contract of agency, it may be implied which could arise from the act and conduct of all the parties or situation in which the parties are put as observed by the Hon’ble Supreme Court in the case of Lakshrniriaraypn Ram Gopal & Sons Ltd. Vs. Government of Hyderabad (1954) 25 ITR 449 (SC).

5.4.11 In the case in hand, it is manifested from the records as well as from the facts and circumstances of the case that the benefit/incentive given by the assessee is in the nature of discount because the discount is always given at the time of transaction of sale and purchase between the owner and the advertising agency and the said amount is required to be reduced from the gross price and therefore, the sale price is always ex-discount.

5.4.12 On the other hand, the commission is given only after the completion of the task or services or the sale, if it is on sale of products by the distributor or dealer to the retailer or consumers. When the distributor records the purchase price without reducing the amount of so-called discount, then the said benefit flowed by the assessee to the distributor, would not partake the character of discount.

5.4.13 The assessee recognizes the revenue from sale of air time as per invoice/bill at which the air time were sold to the advertising agency and the amount of discount is not separately treated as expenditure on account of sale of air time and accordingly, not debited to the P&L account. This clearly brings out the case of the assessee to fall within the ambit of discount. The assessee has not appointed the advertising agency as its agent directly or indirectly. No evidence on record is produced by assessing officer to show that the advertising agency was appointed by the appellant for sale of its air time. The discounts have been offered by the appellant as per prevalent trade practice. The inventory of the air time is always with the appellant. The advertising agency buys the air time slots as per their desire and requirements of the advertiser. The appellant has no say in this regard. If a particular time slot remains vacant the loss is of the appellant. Therefore the discount offered by that appellant on sale of air time does not partake the character of commission.

5.4.14 The Hon’ble Allahabad High Court in the case of Jagran Prakashan (supra) has held that it is clear that no foundational facts exists on the basis of which any inference can be drawn that advertising agencies are agent of the petitioner and further advertising agencies render any service to the newspaper. The SLP filed by the Department against the decision is dismissed by the Supreme Court. Hence this judgment has attained finality.

5.4.15 In the instant case also, there is no evidence on record to show that the advertising agencies were agents of the appellant directly or indirectly and they have received any remuneration from the appellant to sell of their air time. The discount given by the appellant as per prevailing industry practice which the appellant was giving to any person who was buying air time from them i.e. direct advertisers or the advertising agency.

5.4.16 In view of the aforesaid discussion, the legal and factual matrix of the case, I am of the considered opinion that appellant is not liable to deduct TDS on agency discount under section 194H of the IT Act, the addition made by assessing officer is accordingly deleted.”

4.6 During the course of hearing before us, learned Departmental Representative supported the order of the assessing officer and submitted that there was failure on the part of the assessee in deducting tax at source on the amount of agency commission paid to these agencies as has been discussed by the assessing officer in his assessment order.

4.7 Per contra, learned counsel of the assessee vehemently supported the order of the learned Commissioner (Appeals). It was submitted that now this issue is covered in favor of the assessee on the basis of various judgments. Reliance was placed on the judgments of Hon’ble Allahabad High Court in the case of Jagaran Prakashan Ltd. Vs. Dy. CIT (2012) 251 CTR (All) 65 : (2012) 73 DTR (All) 233 : (2012) 345 ITR 288 (All) and Asstt. CIT Vs. TV. Today Network Ltd. (ITA No. 3943/Del/2006, date 15-7-2011). Reliance was also placed on the CBDT Circular No. 5 of 2016, dt. 29-2-2016 ((2016) 132 DTR (St) 335 : (2016) 284 CTR (St) 4) regarding applicability of TDS provisions on payments made by television channels to media agencies. It was also submitted that in subsequent years TDS returns were processed by the assessing officer wherein no such issue has been raised and no such liability has been raised.

4.8 We have gone through the orders passed by the lower authorities and facts of this case and also the judgment relied upon before us. It is noted by us that now the issue of obligation of deduction of tax at source by the television channels or media companies upon the payments made to advertising agencies has been settled by the Board in its Circular No. 5 of 2016, dt. 29-2-2016. We find it appropriate to reproduce the relevant part of this circular as under :–

Sub : Tax Deduction at Source (TDS) on payments by television channels and publishing houses to advertisement companies for procuring or canvassing for advertisements.

The issue of” applicability of TDS provisions on payments made by television channels or media houses publishing newspapers or magazines to advertising agencies for procuring and canvassing for advertisements has been examined by the Board in view of representations received in this regard.

2. It is noted that there are two types of payments involved in the advertising business :-

(i) Payment by client to the advertising agency, and

(ii) Payment by advertising agency to the television channel/newspaper company.

The applicability of TDS on these payments has already been dealt with in Circular No. 715, dated 8-8-1995 ((1995) 127 CTR (St) 13), where it has been clarified in Question Nos. 1 and 2 that while TDS under section 194C (as work contract) will be applicable on the first type of payment, there will be no TDS under section 194C on the second type of payment e.g. payment by advertising agency to the media company.

However, another issue has been raised in various cases as to whether the fees/charges taken or retained by advertising companies from media companies for canvasing/booking advertisements (typically 15 per cent of the billing) is ‘commission’ or ‘discount’. It has been argued by the assessees that since the relationship between the media company and the advertising company is on a principal-to-principal basis, such payments are in the nature of trade discount and not commission and, therefore, outside the purview of TDS under section 194H. The Department, on the other hand, has taken the stand in some cases that since the advertising agencies act on behalf of the media companies for procuring advertisements, the margin retained by the former amounts to constructive payment of commission and, accordingly, TDS under section 194H is attracted.

The issue has been examined by the Allahabad High Court in the case of Jagran Prakashan Ltd. and Delhi High Court in the matter of Living Media Ltd. and it was held in both the cases that the relationship between the media company and the advertising agency is that of a ‘principal to principal’ and, therefore, not liable for TDS under section 194H. The SLPs filed by the Department in the matter of Living Media Ltd. and Jagran Prakashan Ltd. have been dismissed by the Supreme Court vide order dated 11-12-2009 and order dated 5-5-2014, respectively. Though these decisions are in respect of print media, the ratio is also applicable to electronic media/ television advertising as the broad nature of the activities involved is similar.

5. In view of the above, it is hereby clarified that no TDS is attracted on payments made by television channels/ newspaper companies to the advertising agency for booking or procuring of or canvassing for advertisements. It is also further clarified that ‘commission’ referred to in Question No. 27 of the Board’s Circular No. 715, dt. 8th Aug., 1995 does not refer to payments by media companies to advertising companies for booking of advertisements but to payments for engagement of models, artists, photographers, sports persons, etc. and, therefore, is not relevant to the issue of TDS referred to in this circular.”

4.9 Thus, from the above circular, it is clear that this issue is now settled in favour of the assessee on the basis of judgments of Hon’ble Allahabad High Court in the case of Jagran Prakashan Ltd. (supra) and Delhi High Court in the matter of T.V. Today Network Ltd. (sic-Living Media Ltd.). Both these judgments have been accepted by Hon’ble Supreme Court by dismissing SLPs filed by the Department against these judgments. Further, relying upon these judgments, now Board has also taken a clear stand that no TDS is required to be deducted on the impugned payments made by the assessee to the advertising agency. Thus, we find that the order passed by the learned Commissioner (Appeals) is in consonance with the aforesaid judgments and Board’s circular. Therefore, no interference is called for in the order passed by learned Commissioner (Appeals). Thus, ground No. 1 raised by the Revenue is dismissed.

5. Ground Nos. 2 and 3 : In these grounds, the Revenue is aggrieved with the action of learned Commissioner (Appeals) in holding that the assessee company has rightly deducted the tax at source under section 194J of the Act, on payments made to Radio Jockey(ies) as against view of the assessing officer that these payments were in the nature of salary, therefore TDS should have been deducted under section 192 of the Act.

5.1 During the course of assessment proceedings, it was noted by the assessing officer that assessee company had made payments of Rs. 2.26 crores during the year under consideration to Radio Jockeys (RJs) and deducted TDS on this payment @ 10 per cent under section 194J considering its as payment of professional/consultancy charges. The assessing officer examined the terms of the agreement made with RJs and inferred that there was an employer-employee relation between the assessee and RJ, therefore payments of RJ should have been subjected to deduction of TDS under section 192 by treating is as salary and not under section 194J by treating is as professional/ consultancy charges. Accordingly, he issued show-cause notice to the assessee. The assessee submitted detailed reply analyzing various clauses of the agreement in detail to argue that contents of the agreement with the RJ clearly suggest that these are exclusive professional contract. It was also submitted that RJs have raised invoices on the assessee company for the service rendered by them. Finally, the assessee summarized its arguments on this issue as under :

5. We wish to clarify the following in respect of the engagement of RJs :–

(a) The RJs are not required to provide services in compliance to all internal codes of ENIL unlike in the case of its employee;

(b) The RJs are not required to report as per duty hours like the employees;

(c) The RJs are not governed by the leave rules of the company;

(d) The RJs are not entitled to terminal and retirement benefits like

gratuity, leave encashment etc.;

(e) The RJs are not eligible for contribution of provident fund;

(f) The RJs are required to provide exclusive services to ENIL with the exception of providing services such as compering, anchoring etc. (to non-restricted persons) with the prior permission of the company;

(g) The in/ out time are not applicable for RJs as they are not required to sign the muster.

5.2 But, assessing officer was not convinced with the argument of the assessee, and after analyzing agreement with RJs, it was held by the assessing officer that TDS should have been deducted by treating the impugned payment as salary under section 192, by observing as under :–

“From the above mentioned terms and conditions it seems that the RJs are engaged by the assessee company on fixed compensation/fees and also the RJs are employed not for one year but also for three years. It is also seen that they are eligible for annual performance bonus and they are at the discretion of the company to relocate at any station. Further, the RJs are not allowed to do similar type of job with any other entity.

In view of the above observations it is clear that there exists an employer-employee relationship between the RJs and the company. Therefore, the company is supposed to deduct TDS under section 192 as per applicable rate which is @ 30 per cent on the payment to RJs which is salary but not professional/consultancy fees. Since the assessee company has deducted TDS @ 10 per cent as per section 194J on total payment of Rs. 2.26 to RJs, hence the assessee is in default under sections 201(1) and 201(1A) of IT Act.”

5.3 In the appeal before the learned Commissioner (Appeals), the assessee made detailed submissions. It was submitted that the relationship between the assessee and RJs is one of the independent professional service and cannot be construed as employment. The assessee suggested following factors to impress upon the point that terms and conditions of the agreement with the RJs suggest that there was no relations of employer and employee between the assessee and RJs :–

RJs were not regulated by employee rule

They were not eligible for retirement benefits

They were not exclusively rendering services to ENIL

Annual performance incentive plan – the RJs were incentivized on the basis of popularity

Limited liability–RJs were solely responsible for their acts

Full indemnification by the RJs for injuries to ENIL

No probation period

Restriction on use of logo, trade mark, personality name, etc.

Limitation of ENIL’s liability for any damages

Relationship of independent contractors on a principal-to-principal basis.

No break-up of compensation into basic, allowances, etc.

5.4 It was also submitted by ‘he assessee that RJs are free to take assignments elsewhere (except with any other Radio Broadcasting Company). Learned Commissioner (Appeals) considered observations of the assessing officer as well as submissions made by the assessee and also examined copies of agreements put forth before him. It was concluded by him that there was no employer-employee relationship between assessee and RJs. Learned Commissioner (Appeals) decided this issue in favour of the assessee by observing as under :–

“I have considered the facts of case, the submission of the appellant and the order of the assessing officer. On perusal of the agreement it is observed that nowhere it is mentioned that RJs are employees of the appellant. It is also admitted fact that RJs are not entitled for benefits which a company employee is entitled for e.g. provident fund, gratuity, retirement benefits etc. The agreement is for a specific period and its ‘renewal is not binding on the company. The assessing officer has also not brought any conclusive evidence on record to prove that RJs are employees. In his order the assessing officer has simply stated that it seems that RJs are employees without corroborating it with any evidence. The RJs are professionals and have taken other assignments too. The proof for the same is on record. In IT return also their income is shown as professional receipt and not as salary. Therefore, the assessee has rightly deducted tax at source under section 194J. The claim of the assessee is upheld and the addition of Rs. 61,03,334 stands deleted.”

5.5 During the course of hearing before us, learned Departmental Representative relied upon the order of the assessing officer. Per contra, learned counsel of the assessee vehemently relied upon the order of the learned Commissioner (Appeals) and further relied submissions made by the assessee before learned. Commissioner (Appeals). He also drew our attention upon the sample agreement enclosed in the paper book to impress upon the point that there was no employer-employee relationship. It was submitted that the RJs have offered the impugned income as part of the professional receipts and has been accepted as such. Nothing has been brought on record by the assessing officer to show that if in any case the said income has been treated as income under the head ‘Salary’. It was also submitted that service-tax is being paid since July, 2012. Learned counsel also submitted sample copy of appointment letter as is issued to the employees by the assessee company and argued that the rules applicable to the employees of the assessee are not applicable upon the RJs. These agreements have been entered with the purpose of bring continuity and stability in providing service by the RJs so that live programmes are not adversely affected.

5.6 Finally, in support of his argument that in such case no employer-employee relationship exists, he placed reliance upon the following judgments :–

1. Asstt. CIT Vs. Fortis Healthcare Ltd. (ITA Nos. 296, 297, 649 and 650/Chd/2015)

2. Dy. CIT Vs. Yashoda Super Specialty Hospital (2010) 133 TTJ (Hyd)(UO)

3. CIT Vs. Yashoda Super Specialty Hospital (2014) 270 CTR (AP) 457 : (2014) 108 DTR (AP) 323 : (2014) 365 ITR 356 (AP)

4. ITO Vs. Calcutta Medical Research Institute (2001) 70 TTJ (Kol) 583 : (2000) 75 ITD 484 (Kol)

5. CIT Vs. Mrs. Durga Khote (1952) 21 ITR 22 (Bom)

6. G. Godhra Electricity Co. Ltd. Vs. CIT (1997) 139 CTR (SC) 564 : (1997) 225 ITR 746 (SC)

7. Asstt. CIT Vs. Ushodaya Enterprises (P) Ltd. (2012) 53 SOT 193 (Hyd).

5.7 We have gone through the orders passed by the lower authorities, copies of agreement and other evidences shown to us and also judgment placed before us. It is noted by us at the very outset that it has been pointed out by the assessee that the impugned payments have been shown as part of professional income by the RJs in their respective returns and have been accepted as such by their respective assessing officers. Nothing has been brought on record by the assessing officer or by the learned Departmental Representative before us to contradict this aspect to show whether in any case the said income has been treated as income under the head of salaries. It is also not the case of the assessing officer that ultimately any RJs is left to be assessed by the Department or if any one of them avoided making payment of tax. The case of the assessee, which remains undisputed, is that all the RJs were duly assessed to tax and they have paid taxes and filed their returns as per law. Under these circumstances, it was not justified on the part of the assessing officer to magnify this issue and change the relationship of the assessee and RJs from professional consultant to employee by any inappropriate reading of terms of the agreement. Further, it is noted by us that learned Commissioner (Appeals) has rightly pointed out RJs were not entitled for the various benefits which assessee company’s employees were entitled e.g. provident fund, gratuity, retirement benefits etc. The agreements with them were for a specific period and assessee company was not bound to renew the same. It has also been noted by us that RJs were free to take assignments from any company (except with any other radio broadcasting company). They were not bound to act solely as RJs. Such kind of permissions cannot be given to employee. It is also worth noting that with effect from 1-7-2012, the RJs were liable to pay service-tax on the value of service rendered by them. The assessee supported this fact with the help of sample copies of invoices showing that service-tax was charged by the RJs. Thus, different treatment cannot be given under the income-tax law and service-tax law to decide the nature of the payments.

5.8 Further, on examination of various clauses of the agreement, it is noted that neither it is mentioned anywhere that RJ would be employee of the assessee, nor it can be concluded on the basis of holistic reading of the entire agreement that there was any employer-employee relationship between assessee and RJs.

5.9 Lastly, it is noted by us that the assessee has made payment by treating it as payment for professional services. Under these circumstances, the assessee was obliged to deduct the TDS under section 194J only. Similar view has been taken in various cases as have been relied upon by the learned counsel, as reproduced in earlier part of our order. In the case of CIT Vs. Yashoda Super Specialty Hospital (supra) following questions were raised :–

“1. Whether, on the facts and in the circumstances of the case, the Appellate Tribunal is justified in setting aside the order passed against the assessee under section 201 and section 201 (1A) of the IT Act ?

2. Whether, on the facts and in the circumstances of the case, the finding of the Appellate Tribunal that there existed no relationship of employer and employee between the assessee and the consultant doctors, employed in the hospital can be said to be based on material on record ?”

5.10 The main issue involved before Hon’ble High Court was whether doctors were employees of the assessee hospital or not, and if yes, payments made to the doctors were to be treated as payment of the salary so as to attract provisions of section 192 of the Act. Hon’ble High Court examined the agreement between hospital and doctors, which was on identical facts and circumstances as between assessee and RJ, and observed as under :–

“The learned Tribunal as well as the Commissioner (Appeals), on facts and on examining the document ‘agreement of engagement of the consultant doctors by the assessee, found that there is no relationship of employer and employee. After examining the agreement and various terms and conditions, it was found that the doctors are not administratively controlled or managed by the assessee and they are free to come at any point of time as far as their attendance is concerned and treat the patients. In the agreement, there is no provision for payment of any provident fund and gratuity. The only clause in the agreement is that the doctors cannot take up any other assignment. Reading the agreement as a whole, both the authorities below observed that the existence of one prohibitory clause, as stated above, does not change the basic character of the relationship between the assessee and the doctors concerned. On facts, the Tribunal found that there is no employer and employee relationship and their payment cannot be treated to be salaries and, as such, deduction cannot be made under section 192 of the IT Act.”

5.11 Similarly, in the case of Asst. CIT Vs. Fortis Healthcare Ltd. (supra), Hon’ble Chandigarh Bench has taken a similar view. Relevant part of decision is reproduced here under :–

20. To decide the issue whether TDS has to be deducted as per section 192 or 194J of the Act, the basic requirement is to interpret the relationship between the assessee and the doctors. Further, a distinction is also to be drawn between the ‘contract for service’ and ‘contract of service’. This issue has been very aptly dealt with by the learned Commissioner (Appeals) in his order at para 5.1. The contract ‘for service’ implies a contract, whereby one party undertakes to render the service, for example professional or technical services, to or for another in the performance of which he is not subject to detailed directions and control but exercises professional or technical skill and uses his own knowledge and discretion. A ‘contract of service’ implies relationship of master and servant and involves an obligation to obey orders in the work to be performed and also as to its mode and manner of performance. As we have also stated that from the perusal of the agreements with the doctors, we do not see any relationship that of master and servant between the assessee and the doctors on retainer ship basis. It is also seen from these agreements that the doctors who are on the payroll of the assessee are debarred from taking up any other work for remuneration part time or otherwise or work in advisory capacity or on interest directly or indirectly in any other trade or business during the employment with the assessee without permission of the assessee, while the doctors on retainer ship basis are only debarred from not getting in similar or any capacity for any other company engaged in a business similar to that of the assessee. The difference between this clause in two types of agreements itself goes to prove that doctors who are engaged on retainer ship basis are not the servants of the assessee since they are allowed to do whatever they want except joining the similar business while other doctors who are on the payroll of the assessee are debarred from doing any other activity apart from that of the assessee.

21. From the perusal of all the material placed before us as well as the judicial pronouncements cited, we see that no relationship of master and servant exists between the assessee and the retainer doctors.

5.12 Turning back to the facts of the case before us, it is noted that actually there was no relationship of master and servant between the assessee and RJ. Nothing has been brought before us by the assessing officer or by learned Departmental Representative to establish any such relationship between the two. Under these circumstances, we find that the order of learned Commissioner (Appeals) is perfectly in accordance with law and facts of this case. We do not find any justification for making any interference in the order of the learned Commissioner (Appeals). Therefore, same is upheld. Ground Nos. 2 and 3 are dismissed.

6. Ground No. 4 : This ground was stated to be consequential, therefore same is hereby dismissed.

Now we shall take up appeal for assessment year 2012-13 in ITA No. 5227/Mum/2014.

7. It is noted that grounds raised by the Revenue are identical to the grounds raised in assessment year 2011- 12. Thus, the order for assessment year 2011- 12 shall apply mutatis mutandis on the ground raised in assessment year 2012- 13.

8. In the result, both the appeals filed by the Revenue are dismissed.