Case Law Details

We have observed, the AO while completing the assessment has called for complete details of calculation of deduction u/s 10A and 10AA of the Act. We have referred to the enquiries made by the AO in this regard in the earlier paragraphs of this order. In the light of the enquiries made by the AO in the course of assessment proceedings, we are of the view that the findings of CIT in para-4 of his order that the AO did not make necessary enquiries regarding the existence of a single account for various units or separate accounts of various units and about the nature of work of separate units, cannot be sustained. We also are of the view that the AO was fully conscious of the issue where provision of section 10A and 10AA of the Act were to be construed as deduction provision or exemption provisions and had in the course of assessment proceedings called for calculation of deduction u/s 10A and 10AA of the Act. In fact perusal of the order of assessment u/s 143(3) of the Act shows that the AO has disallowed the expenses claimed by the assessee by way of provision for leave encashment while arriving at the eligible provision of section 10A and 10AA units. It cannot therefore be said that there was any failure on the part of the AO for proper or adequate enquiries to claim deduction u/s 10A and 10AA before completing the assessment.

As far as the question whether section 10A and 10AA of the Act are deduction provisions or exemption provisions, is concerned, the first aspect which needs to be mentioned is that the issue was debatable and there are decisions of courts which have taken a view that the aforesaid provisions were exemption provision and will therefore not enter the computation of total income at all. These decisions have been rendered even after the CBDT Circular dated 16.07.20 13 wherein it has been mentioned that provision of section 10A and 10AA of the Act were deduction provision though they are part of Chapter-III of the Act. In the light of the debate that existed when the order of the assessment was framed and when the impugned order u/s 263 of the Act was passed, it cannot be said that the view taken by the AO was an erroneous view. In fact the view taken by the AO was a possible view supported by decisions of courts. It cannot therefore be said that there was either incorrect assumption of fact or incorrect application of law so as to invoke the provision u/s 263 of the Act. Apart from the above we find that the Hon;ble Supreme Court in the case of CIT vs Yokogawa India Ltd. (supra) has taken the view that the provision of section 10A and 10AA of the Act are deduction provisions but the stage of deduction would be while computing gross total income of eligible undertaking under Chapter-IV of the Act and not at the stage of computation of total income under Chapter-VI of the Act. The effect of the aforesaid decision would be that the provision of set off and carry forward as contemplated under Chapter-VI of the Act would not be attracted and therefore intra head set off sought to be done by the CIT by seeking to rely on the provision of section 70(1) of the Act and seeking to restrict the deduction u/s 10A and 10AA of the Act to the extent of gross total income as contemplated u/s 80A(2) of the Act, cannot be sustained.

Every loss of revenue due to AO order cannot be treated as prejudicial to revenue interest

For the reasons given above we are of the view that the order of AO was neither erroneous nor prejudicial to the interest of the revenue and the conditions precedent for exercise of jurisdiction u/s 263 of the Act are absent in the present case. The principles laid down by the Hon’ble Supreme Court in the context of exercising of jurisdiction u/s 263 of the Act in the case of Malabar Industrial Co. Ltd. 243 ITR 83 as well as CIT vs Max India Ltd. 294 ITR 292 is that every loss of revenue as a consequence of the order of AO cannot be treated as prejudicial to the interest of the revenue. When the AO adopted one course permissible under law and it is resulted in any loss of revenue or where two views are possible and the AO has taken one view with which the Commissioner does not agree, it cannot be treated as an erroneous order prejudicial to the interest of the revenue, unless the view taken by the AO is unsustainable in law. The above proposition of law if applied to the facts of the present case would show that the condition precedent for exercise of jurisdiction u/s 263 of the Act, are absent.

Full Text of the ITAT Order is as follows:-

This is an appeal by the Assessee against the order dated 18.03.2015 of CIT-Kol-3, Kolkata passed u/s 263 of the Income Tax Act, 1961 (Act.).

2. The Assessee is a company. The assessee is management, technical, professional consultant and it is also engaged in the business of providing back office support service, i.e., Information Technology Enabled Services (ITES). For A.Y.2010-11 the Assessee filed return of income on 14.10.2010 showing a loss of Rs.14,30,54,165/-. The Assessee had four units

(i) STPI unit eligible for deduction u/s 10A of the Act known as SSL

(ii) SEZ unit eligible for deduction u/s 10AA of the Act called as SEZ unit

(iii) GGN unit which is a non SEZ unit whose income is chargeable to tax under the Act, and

(iv) Non SSL unit whose income is also chargeable to tax.

The computation of total income as given by the assessee is given as Annexure to this order. The computation of Income under the head Income from Business & Profession, as furnished by the Assessee along with the return of income was as under :

| Income under the head Business & Profession | |

| For eligible units before allowing deduction u/s 10A is | Rs.58,65,95,555 |

| Less: Deduction allowed u/s 10A | (Rs.58,31,79,442) |

| Taxable Business Income of STPI Unit …[A] | Rs. 34,16,113 |

| Income under the head Business & Profession | |

| For eligible units before allowing deduction u/s 10AA is | Rs.5,58,26,092 |

| Less: Deduction allowed u/s 10AA | (Rs.5,45,20,053) |

| Taxable Business Income of SEZ Unit …[B] | Rs. 13,06,039 |

| -Loss under the head Business & Profession for other unit is..(C) | (Rs.8,37,63,777) |

| Income under the head Business & Profession[A]+[B]+[C] | (Rs.7,90,41,626) |

| Short Term Capital Gains | Rs. 45,692 |

| Income from other sources | Rs. 32,10,941 |

| Taxable Income/(Loss) Carry Forward | (Rs. 7,57,84,993) |

3. The AO completed the assessment u/s 143(3) of the Act wherein the AO allowed deduction u/s 10A and 10AA of the Act without set off of loss of taxable unit. It can be seen from the aforesaid computation that out of the 4 units of the Assessee, two units whose income is chargeable to tax i.e., units other than the Sec.10A and 10AA units, incurred loss of Rs.8,37,63,777.

4. Sec. 4 of the Act creates charge of income-tax and it provides that where any Central Act enacts that income tax shall be charged for any assessment year at any rate or rates, income-tax at that rate or those rates shall be charged for that year in accordance with, and subject to the provisions (including provisions for the levy of additional income-tax) of this Act in respect of the total income of the previous year of every person. The charge of tax is thus on total income. Sec. 2 (45) defines total income to mean total amount of income referred to in Sec.5, computed in the manner laid down in this Act. Chapter-II of the Act, from section 4 to 9 deal with Basis of Charge. Chapter-III of the Act, deals with income which do not form part of total income and are contained in Sect. 10 to 13-B of the Act. Chapter IV deals with the computation of total income. Firstly income is categorized under various heads of income. This is laid down in Section 14 of the Act, which lays down that save as otherwise provided by this Act, all income shall, for the purposes of charge of income-tax and computation of total income, be classified under the following heads of income – Salaries, income from house property, profits and gains of business or profession, capital gains, income from other sources. Chapter V then brings income of other persons, which are to be included in the total income of an Assessee and this is contained in section 60 to 65 of the Act. Chapter-VI (containing sec. 66 to 80) then lays down provisions regarding aggregation of income and set off or carry forward of loss. Section 66 reads as under:-

“Total income – in computing the total income of an assessee, there shall be included all income on which no income-tax is payable under Chapter VII.”

The provisions of section 66 are not applicable to incomes which are absolutely exempt from tax as per Section 10, Section 11 etc., falling under Chapter III. This position is made clear by s. 66 itself as it speaks only of “incomes on which tax is not payable” and similar words are used in Chapter VII only thus leaving out by implication incomes which do not form part of total income at all as per Chapter III from the scope of s. 66. Under Sec.70(2) of the Act, where the net result for any assessment year in respect of any source falling under any head of income, other than “capital gains”, is a loss, the Assessee shall be entitled to have the amount of such loss set off against his income from any other source under the same head.

5. From the charging provisions of the Act, it is clear that both profit as well as loss which is negative profit must enter into computation, wherever it becomes material. The charge is on total income of the Assessee. Sec. 2 (45) defines total income to mean total amount of income referred to in Sec.5, computed in the manner laid down in this Act. An income in order to come within the purview of that definition must satisfy two conditions. Firstly, it must comprise the “total amount of income, profits and gains. Secondly, it must be “computed in the manner laid down in the Act”. If either of these conditions fails, the income will not be a part of the total income that can be brought to charge. If income includes loss and if income of the eligible unit does not form part of the total income under the Act by virtue of provisions of Sec.10A or 10AA of the Act contained in Chapter III of the Act, then neither the gain nor loss would be considered for computation of total income. (emphasis supplied). Therefore if the income of the eligible unit is considered as falling within Chapter III then the computation of total income as done by the Assessee is correct. On the other hand if the income of the eligible unit is considered as falling within Chapter VIA of the Act dealing with deductions from Gross Total Income, then the provisions of Chapter VI of the Act, especially Sec.70(1) of the Act has to be given effect to. In that case, the loss of the non eligible units would get set off completely by the profits of the eligible unit and the deduction allowed to the eligible units u/s.10A and 10AA of the Act would be less. More importantly the carry forward of loss as claimed by the Assessee for set off in the subsequent assessment years would be nil. This the background in which the present proceedings u/s.263 of the Act was initiated by the CIT.

6. The AO before completing the assessment u/s 143(3) of the Act, made the following enquiries with regard to the assessee’s claim of deduction u/s 10A and 10AA of the Act. On 23.07.20 12 the AO called upon the Assessee to give calculation of deduction u/s 10A and 10AA of the Act and explain how the figure claimed as income eligible for deduction u/s.10A and 10AA of the Act was arrived at. The case was adjourned to 22.08.2012. On 22.08.2012, the AO has recorded proceedings before him in which he has recorded the fact that the assessee has explained sector wise break up of profit and loss account calculation of section 10A and 10AA deduction. Again on a hearing held on 12.02.20 13, the AO has recorded the fact that the assessee has filed submissions of 20.09.20 12 explaining calculation of deduction u/s 10A and 10AA and reasons for adjustment of income and expenses claimable u/s 10AA of the Act.

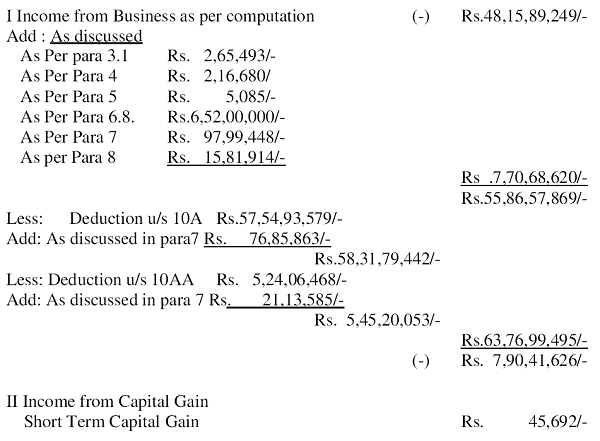

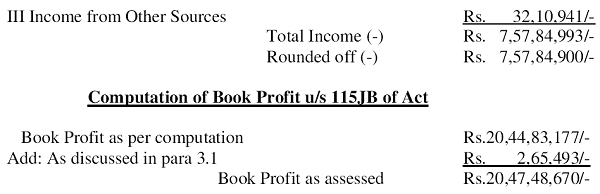

7. The AO passed an order of assessment u/s 143(3) of the Act dated 31.03.2013 wherein he accepted the computation of deduction u/s 10A and 10AA of the Act as worked out by the assessee. The AO also did not set off the loss of taxable unit against the income of 10A and 10AA unit. Further the AO allowed deduction u/s 10A and 10AA and added a sum of Rs.63,76,99,495/- though the income under the head income from business arrived at by the AO was only at Rs.55,86,57,869/-. The following was the computation of total income made by the AO :-

“ 9. Subject to the above discussion and materials on record, the total income of the assesee is determined and assessed as under :

Long Term Capital Loss of Rs.65,60,002/- and unabsorbed depreciation of Rs.7,57,84,990/- are to be carried forward for future set off. “8. The CIT in exercise of his powers u/s 263 of the Act was of the view that the aforesaid order of the AO was erroneous and prejudicial to the interest of the revenue for two reasons. (i) the deduction u/s10A and 10AA of the Act was allowed without setting off of loss of units whose income was chargeable to tax and (ii) deduction u/s 10A and 10AA of the Act ought to have been restricted to the total income computed under the head “ income from business” of Rs.55,86,57,869/-. The CIT issued a show cause notice on the above issues to the Assessee and calling upon the Assessee to show cause as to why the aforesaid order should not be revised in exercise of powers u/s.263 of the Act.9. The assessee in reply to the show cause notice dated 08.01.2015 vide its reply dated 19.01.2015 pointed out that the view taken by the AO was a possible view supported by several decisions rendered by Hon’ble High Courts and therefore the CT in exercise of his powers u/s 263 of the Act cannot term the view taken by the AO as erroneous. The Assessee pointed out that in Circular No. 7 /DV /20 13 dated 16.7.20 13 wherein it was explained that despite the placement of Sec.10A in Chapter III, those provisions were deduction provisions and therefore the set off of profits of the eligible unit with the loss of the non eligible unit has to be done at the stage of aggregation of income and before allowing deduction under Chapter VIA of the Act. It was also pointed out by the Assessee that in several judicial pronouncements, it has been laid down that Section 10A is a self-contained provision for computing the profits and gains of an undertaking engaged in the export and a literal reading thereof requires a deduction from total income. The Act provides for deductions “in” computing the total income but no mechanism is provided for any deduction “from” the total income already computed. In other words, once total income is computed, the next step would be computation of tax and there would be no further deductions. The phrase ‘total income’ as used in Section l0A is to be understood in commercial sense. In the context of section l0A, total income is of the undertaking and not the total income of the Taxpayer. Further, the relief under Section l0A is with respect to an undertaking and not the business of the Taxpayer as a whole. The relief under Section 10A is in the nature of exemption, although termed as deduction. The relief is in respect of commercial profits, which are neither subject to charge under the ITA nor includible in the total income. Relief under section 10A would have to be given effect before Chapter-IV of ITA which deals with the computation of total income. In other words, deduction shall be given before process of computation of profits or gains of business or profession begins. As the income of 10A unit was to be excluded at source itself before arriving at gross total income, the question of setting off losses of non- eligible units or unabsorbed business loss and depreciation of preceding years of the same unit does not arise. Computation of total income is to be carried out only after exclusion of profits under section 10A.The Income Tax Return form also supports the proposition that though taxpayer may be having more than one undertaking, it is the export profits of the eligible undertaking which are to be considered for computing the relief and such profits are not to be included in total income of the taxpayer. Prior to amendment in 2003, section 10A(6) provided for complete prohibition from carried forward of business losses and depreciation beyond the tax holiday period. Amendment carried out by Finance Act 2003 w.e.f April 2001 lifted the bar and permitted the taxpayer to carry forward and set off unabsorbed business losses and depreciation beyond the tax holiday period. Having regard to exemption nature of section-10A, ordinarily, loss incurred by an eligible unit would not have been allowed to be carried forward and set off against income of other unit. Grant of carry forward and set off of losses and depreciation does not mitigate against the proposition that benefit or relief under section 10A is in the nature of exemption with reference to the commercial profits. The Assessee placed reliance on the decision of the Hon’ble Supreme Court in Canara Work Shop Ltd. [161 ITR 120] and decision in the case of CIT v Yokogawa India Ltd. [(2012) 341 ITR 385(karn) in this regard. The Assessee thus submitted that a taxpayer should be allowed deduction under s. 10A/10B/10AA with respect to profits of a specific eligible unit without adjustment there against of current or unabsorbed losses and depreciation of any activity or any unit regardless of whether the other unit is or is not an eligible unit in its own right. This proposition is on the basis that each qualifying unit should be considered as a self-contained independent unit in the year in which deduction is to be computed. This position also has support from judicial rulings as submitted herein above.10. The Assessee submitted that the view taken by the AO finds support from the decisions mentioned above. Therefore the view being taken by the AO was a possible view and cannot be said to be erroneous. The view taken by the CIT in the show cause notice based upon CBDT circular to the extent it suggests aggregation is in conflict with correct legal position and judicial rulings. The Assessee therefore submitted that circular is not binding as it is contrary to the decisions sighted above.

11. The CIT however observed in para-4 and 5 of his order that the AO failed to make necessary inquiry with regard to the existence of separate units and as to how the assessee has maintained its accounts viz., whether one account was maintained for all the units or separate accounts were maintained for separate units. The CIT in para-4 of his order concluded that failure to make such enquiry rendered the order of AO erroneous and prejudicial to the interest of the revenue. The CIT has also observed that in exercise of his powers u/s 263 of the Act he can even go into a debatable issue and he has wide powers. Thereafter in para-6 of his order the CIT has also expressed his view that provisions of section 10A and 10AA of the Act were deduction provisions and therefore loss of the units which were not entitled to tax exemption ought to be set off against the profits of 10A and 10AA unit and only on the reminder deduction u/s 10A and 10AA of the Act ought to have been allowed by the AO. The CIT in this regard made a reference to the CBDT Circular No.07/DV/2013 dated 16.07.2013 . Thereafter he has referred to the fact that since the AO had not examined all the facts and details while allowing excess carry forward loss to the assessee as mentioned in para-4 there was wrong assumption of facts and incorrect application of law. The CIT accordingly set aside the order of AO passed u/s 143(3) of the Act and directed the AO to make a fresh verification and assessment. The following were the relevant observations of the CIT :-

“ 6. It is observed that the assessee was allowed deduction of Rs.58,31 ,79,442/- u/s. 10A of the Act and Rs.5,45,20,053/- u/s. 10AA of Act without setting off of loss of taxable unit. It was further observed that the amount of deduction u/s. 10A and Sec. 10AA of the Act was required to be restricted to the business income of Rs.55,86,57,869/- as determined in the assessment order but excess carry forward of loss amounting to Rs. 7,90A1 ,626/- was also allowed to the assessee. It is to be noted that there is no doubt that the cognizance of CBDT’s circular No. 07 /DV /2013 dated 16/07/2013 in this respect has to be taken. However, in this case, the AO has not examined all facts and details while allowing excess carry forward of loss to the assessee as mentioned in Para-4. To that extent there is wrong assumption of fact and incorrect application of law.

The assessment order u/s. 143(3) is, therefore, erroneous and prejudicial to the interest of revenue. I am of the opinion that the case has to go’ pack to the A.O. for prior verification and assessment.

7. In the result, the assessment is set aside for fresh ‘verification end assessment after giving due opportunity to the assessee. A fresh order should be passed after such verification.”

12. Aggrieved by the order of CIT the assessee has preferred the present appeal before the Tribunal.

13. The Ld. Counsel for the assessee pointed that the issue as to whether provision of sections 10A and 10AA of the Act are deduction provisions or exempt provisions was a debatable issue and the AO when he passed the order of 31.03.2013 had taken a view that provisions of section 10A and 10AA of the Act were exemption provisions and therefore the loss of the taxable units should not be set off against the income of the units eligible for deduction u/s 10A and 10AA of the Act. The view taken by the AO was a possible view supported by several decisions of the High Courts referred to by the assessee in reply to the show cause notice u/s 263 of the Act. Therefore order of AO in not setting off of the loss of the taxable units against the income of 10A and 10AA units cannot be termed as erroneous. It was further submitted by him that when the show cause notice u/s 263 of the Act dated 08.01.2015 was issued by CIT and as on 03.2015 when the CIT passed the impugned order, the issue was debatable. The issue was ultimately considered by the Hon’ble Supreme Court in the case of CIT vs Yokogawa India Ltd. (2017) 77 Taxman.,com 41 (SC) by its order dated 16.12.2016 and in the aforesaid decision the Hon’ble Supreme Court took the following view :-

That from a reading of the relevant provisions of section 10A it is more than clear that the deductions contemplated therein is qua the eligible undertaking of an assessee standing on its own and without reference to the other eligible or non-eligible units or undertakings of the assessee. The benefit of deduction is given by the Act to the individual undertaking and resultantly flows to the asses see.

This is also more than clear from the contemporaneous Circular No. 794, dated 9- 8-2000.

If the specific provisions of the Act provide [first proviso to sections 10A(1); 10A(1A) and 10A(4)] that the unit that is contemplated for grant of benefit of deduction is the eligible undertaking and that is also how the contemporaneous Circular of the department (No.794 dated 9-8-2000) understood the situation, it is only logical and natural that the stage of deduction of the profits and gains of the business of an eligible undertaking has to be made independently and, therefore, “immediately after the stage of determination of its profits and gains.

At that stage the aggregate of the incomes under other heads and the provisions for set off and carry forward contained in sections 70, 72 and 74 would be premature for application. The deductions under section 10A therefore would be prior to the commencement of the exercise to be undertaken under Chapter VI for arriving at the total income of the assessee from the gross total income. The somewhat discordant use of the expression ‘total income of the assessee’ in section 10A has already been dealt with earlier and in the overall scenario unfolded by the provisions of section 10A the aforesaid discord can be reconciled by understanding the expression “total income of the assessee” in section 10A as ‘total income of the undertaking’.

For the aforesaid reasons it is held that though section 10A, as amended, is a provision for deduction, the stage of deduction would be while computing the gross total income of the eligible undertaking under Chapter IV and’ not at the stage of computation of the total income under Chapter VI. ”

According to him therefore even if ultimate decision of the Hon’ble Supreme Court is considered then the view taken by the AO was the correct view and therefore the impugned order u/s 263 of the Act deserves to be quashed.

14. The ld. DR placed reliance on the order of CIT and in particular in para-4 of the order of CIT where he placed reliance on the fact that the AO while completing the assessment failed to make proper and adequate enquiries with regard to the claim of deduction u/s 10A and 10AA of the Act as made by the assessee.

15. We have given a very careful consideration to the rival submissions. As we have observed, the AO while completing the assessment has called for complete details of calculation of deduction u/s 10A and 10AA of the Act. We have referred to the enquiries made by the AO in this regard in the earlier paragraphs of this order. In the light of the enquiries made by the AO in the course of assessment proceedings, we are of the view that the findings of CIT in para-4 of his order that the AO did not make necessary enquiries regarding the existence of a single account for various units or separate accounts of various units and about the nature of work of separate units, cannot be sustained. We also are of the view that the AO was fully conscious of the issue where provision of section 10A and 10AA of the Act were to be construed as deduction provision or exemption provisions and had in the course of assessment proceedings called for calculation of deduction u/s 10A and 10AA of the Act. In fact perusal of the order of assessment u/s 143(3) of the Act shows that the AO has disallowed the expenses claimed by the assessee by way of provision for leave encashment while arriving at the eligible provision of section 10A and 10AA units. It cannot therefore be said that there was any failure on the part of the AO for proper or adequate enquiries to claim deduction u/s 10A and 10AA before completing the assessment.

16. As far as the question whether section 10A and 10AA of the Act are deduction provisions or exemption provisions, is concerned, the first aspect which needs to be mentioned is that the issue was debatable and there are decisions of courts which have taken a view that the aforesaid provisions were exemption provision and will therefore not enter the computation of total income at all. These decisions have been rendered even after the CBDT Circular dated 16.07.20 13 wherein it has been mentioned that provision of section 10A and 10AA of the Act were deduction provision though they are part of Chapter-III of the Act. In the light of the debate that existed when the order of the assessment was framed and when the impugned order u/s 263 of the Act was passed, it cannot be said that the view taken by the AO was an erroneous view. In fact the view taken by the AO was a possible view supported by decisions of courts. It cannot therefore be said that there was either incorrect assumption of fact or incorrect application of law so as to invoke the provision u/s 263 of the Act. Apart from the above we find that the Hon;ble Supreme Court in the case of CIT vs Yokogawa India Ltd. (supra) has taken the view that the provision of section 10A and 10AA of the Act are deduction provisions but the stage of deduction would be while computing gross total income of eligible undertaking under Chapter-IV of the Act and not at the stage of computation of total income under Chapter-VI of the Act. The effect of the aforesaid decision would be that the provision of set off and carry forward as contemplated under Chapter-VI of the Act would not be attracted and therefore intra head set off sought to be done by the CIT by seeking to rely on the provision of section 70(1) of the Act and seeking to restrict the deduction u/s 10A and 10AA of the Act to the extent of gross total income as contemplated u/s 80A(2) of the Act, cannot be sustained.

17. For the reasons given above we are of the view that the order of AO was neither erroneous nor prejudicial to the interest of the revenue and the conditions precedent for exercise of jurisdiction u/s 263 of the Act are absent in the present case. The principles laid down by the Hon’ble Supreme Court in the context of exercising of jurisdiction u/s 263 of the Act in the case of Malabar Industrial Co. Ltd. 243 ITR 83 as well as CIT vs Max India Ltd. 294 ITR 292 is that every loss of revenue as a consequence of the order of AO cannot be treated as prejudicial to the interest of the revenue. When the AO adopted one course permissible under law and it is resulted in any loss of revenue or where two views are possible and the AO has taken one view with which the Commissioner does not agree, it cannot be treated as an erroneous order prejudicial to the interest of the revenue, unless the view taken by the AO is unsustainable in law. The above proposition of law if applied to the facts of the present case would show that the condition precedent for exercise of jurisdiction u/s 263 of the Act, are absent.

18. For the reasons given above we quash the order u/s 263 of the Act and allow the appeal of the assessee.

19. In the result the appeal of the assessee is allowed.

Order pronounced in the Court on 19.05.2017.