I. Introduction:

In GST regime tax incidence will arise when supply is happened but a supply will be subject to Central GST (CGST)/State GST (SGST) or Integrated GST (IGST) that will be decided on the basis classification of Inter-state or Intra-state supply. Though, rate of tax for a taxpayer in case of Inter-state or Intra-state supply will be more or less same but wrong classification of supply between inter-state or intra-state and vice-versa may lead to hardship to taxpayer. As per section 19 of IGST Act and section 70 of CGST Act, taxpayer will have to claim refund of wrong taxes paid on the basis of wrong classification made by him and correct tax on the basis of revised/correct classification will have to be paid.

II. Classification of Supply of Goods as Inter-state or Intra-state:

As per the section 3 of IGST Act where location of supplier and place of supply are in different state then such supply will be addressed as Inter-state supply.

Deemed Inter-state Supply:

A. Import of goods in to India

B. Export of goods from India

C. Supply of goods to or by a SEZ developer or an SEZ unit

Intra-state Supply:

As per the section 4 of IGST Act where location of supplier and place of supply are in same state then such supply will be addressed as Intra-state supply.

III. Place of Supply of Goods:

Determination of place of supply for the purpose of correct classification of inter-state or intra-state supply of goods is very essential. Section 7 of IGST Act provides provisions to determine the place of supply of goods. The said section narrates six different kinds of situations for determination of place of supply of goods, which are as follows:

Scenario 1 where supply involves movement of goods:

“Section 7(2) where supply involves movement of goods, whether by the supplier or the recipient or by any other person, the place of supply of goods shall be the location of the goods at the time at which the movement of goods terminates for delivery to the recipient.”

Illustrations:

♦ When goods are sold by supplier of Rajasthan to Recipient/Buyer of Punjab and such goods are sent to Punjab by supplier thru transport agency (any other person as mentioned in section 7(2) of IGST) hired by him then this transaction will be regarded as inter-state supply and IGST will be levied by supplier.

♦ When goods are sold and delivered in Rajasthan by the supplier of Rajasthan to Recipient/Buyer of Punjab as the buyer has taken hand delivery of goods but the supplier has mentioned Buyer’s Punjab address on invoice then this transaction will be regarded as inter-state supply and it will be assumed that movement of goods has been done by recipient and such movement is terminated in Punjab. Supplier will levy IGST in this case.

♦ When goods are sold by supplier of Rajasthan to Recipient/Buyer of Rajasthan then this transition will be regarded as intra-state supply and CGST/SGST will be levied by supplier.

The above illustrations tabularized as under:

| Location of Supplier | Location of Recipient (i.e. Buyer) | Movement of goods | Location of goods at the time of termination | Place of Supply of Goods | Tax to be levied |

| Rajasthan | Punjab | Transporting goods from RJ to PB on the instruction of Supplier/Recipient | Punjab | Punjab | IGST |

| Rajasthan | Punjab | Buyer has taken hand delivery of goods in Rajasthan and he himself has moved goods to Punjab | Deemed to be in Punjab | Rajasthan | IGST |

| Rajasthan | Rajasthan | Transporting goods from RJ to RJ on the instruction of Supplier/Recipient | Rajasthan | Rajasthan | CGST/SGST |

Scenario 2 where supply involves movement of goods:

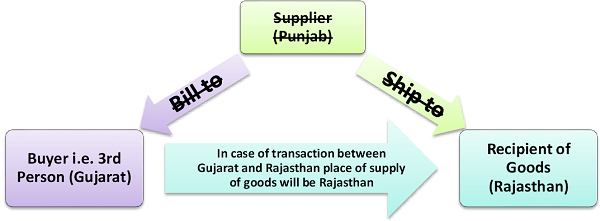

“Section 7(3) where goods are delivered by the supplier to a recipient or any other person, on the direction of a third person, whether Acting as an agent or otherwise, before or during movement of goods, either by way of transfer of document of title to the goods or otherwise, it shall be deemed that the said third person has received the goods and the place of supply of such goods shall be the principal place of business of such person.”

♦ A Punjab supplier sold goods to a Gujarat buyer but on the instruction of buyer the supplier shipped goods (to other person i.e. recipient of goods) at Rajasthan then in this case place of supply of goods will deemed to be the principal place of buyer i.e. Gujarat ignoring the fact that goods physically delivered at Rajasthan.

Scenario 3 where supply does not involves movement of goods:

Section 7(4) where the supply does not involve movement of goods, whether by the supplier or the recipient, the place of supply shall be the location of such goods at the time of the delivery to the recipient.

♦ The first leg of transaction in above example between Punjab Supplier and Gujarat Buyer the place of supply is determined as per the section 7(3) of IGST Act but the second leg of transaction i.e. transaction between Gujarat and Rajasthan, place of supply of goods will be determined as per the provisions of section 7(4) of IGST Act and it will be the location of goods at the time of delivery to the recipient i.e. Rajasthan.

Scenario 4 where supply does not involves movement of goods:

“Section 7(5) where goods are assembled or installed at site, the place of supply shall be the place of such installation or assembly.”

♦ A lift/elevator has installed or assembled in a particular building then the location of supply of goods in this case will be the location of building where the said lift has been installed or assembled.

Scenario 5:

Section 7(6) where goods are supplied on board a conveyance, such as a vessel, an aircraft, a train or a motor vehicle, the place of supply shall be the location at which such goods are taken on board.

♦ Hotel Taj of Mumbai has provided on board meal to a Mumbai Delhi flight, in this case place of supply of goods will be the place where goods are taken on board i.e. Mumbai.

Scenario 6:

As per section 7(7) of IGST where place of supply cannot be determined in terms of above sub section then it shall be determined as per the rules prescribed by the Central Government on the recommendation of the GST Council.

Iv. Concluding Remarks:

The above discussion is solely based on the draft GST law. However, the above provisions may undergo changes by the time of passing of the final GST Act.

(Author is a Manager Taxation with KGK Group of Companies )

SIR WE ARE FALLING UNDER E INVOICE AND WE ARE MANUFCATURER EXPORTER, DEEMED EXPORTER IN DEEMED EXPORT

SUPPLY SUPPLIER : GUJARAT BUYER : RAJASTHAN PLACE OF SUPPLY: MUNDRA PORT – GUJARAT HOW WE CAN ISSUE E INVOICE WITH IGST WITH BILL TO SHIP TO OPTION WITHOUT RCM PLEASE REVERT NEEDFUL