ACS Divesh Goyal

INDEX OF ARTICLE:

INDEX OF ARTICLE:

1. FAQ’S RELATED PARTY TRANSACTIONS:

2. THRESHOLD LIMITS UNDER COMPANIES ACT, 2013.

3. NOTES FOR SECTION- 188.

4. DEFINITION OF RELATED PARTY BY DIAGRAMS.

FAQ’S RELATED PARTY TRANSACTIONS:

| S. No. | Question & Answers |

| A. | Whether the provisions pertaining to „related parties‟ are applicable based on a financial year? |

| Solu. | NO,The provisions pertaining to „related party‟ and „related party transactions‟ are applicable for all contracts or arrangements with related parties entered on or after 1 April 2014, irrespective of the accounting year followed by the Company. |

| B. | What is the effective date of applicability of the provisions/ sections/ rules relating to related party transactions? |

| Solu. | Provisions of the 2013 Act and Rules framed thereunder in relation to related party and related party transactions are effectively applicable from 1 April 2014.The clause 49 of the listing agreement is now effective in a piecemeal basis. However, the applicability of provisions relating to related party transactions remains effective from 1 October 2014 |

| C. | A corporate group has several foreign subsidiaries. Will provisions in relation to related parties apply to foreign companies as well? |

| Solu. | The term ‘company’, as defined under the Companies Act 2013, is a company incorporated under this Act or any previous company law. Company incorporated under the relevant legislation of a foreign country is not a ‘company’ under Companies Act 2013. However, transactions by Indian company with a foreign company, which is a subsidiary, associate, fellow subsidiary, joint venture of the same venturer or company under control of same promoter, would be covered, based on understanding of combined reading of revised clause 49 and Companies Act 2013. |

| D. | In case of Companies Act, is the board required to approve all related party transactions? |

| Solu | The Companies Act 2013 prescribes that a company needs approval of the audit committee on all related party transactions and subsequent modifications thereto. This is irrespective of whether they are in the ordinary course of business and consummated at arm’s length price or they are below prescribed thresholds |

| E. | Whether the contracts or arrangements of transactions with related parties entered on or before 1 April 2014 are also governed by the provisions of the 2013 Act? |

| No, the contracts or arrangements of transactions with related parties entered on or before 1 April 2014 shall continue to be governed by the provisions of the erstwhile Act, and other applicable provisions. | |

| F. | Whether any modification in the contracts or arrangements of transactions with related parties entered on or before 1 April 2014 are also governed by the provisions of the 2013 Act? |

| Modifications made to such contracts/ arrangements on or after 1 April 2014 shall be governed by the provisions of the 2013 Act | |

| G. | In Listed Companies:Whether the contracts or arrangements of transactions with related parties entered on or before 1 October 2014 and will continue beyond 31st March 2014, are also governed by the provisions of the 2013 Act? |

| Such contracts or arrangements for material transactions shall be placed for approval before the shareholders in the first general meeting held after 1 October 2014. | |

| H. | Whether the provisions relating to special resolution under Section 188 are also applicable to transactions with wholly owned subsidiaries? |

| No! Wholly owned subsidiary companies are exempted from the requirement of passing a special resolution, provided requirement of the special resolutions have been complied by the holding company. | |

| I. | Can there be a situation in which contracts or arrangements require special resolution with related party only under amended listing agreement, and not under the 2013 Act? |

| Yes. Contracts or arrangements with related parties in the ordinary course of business and at arm‟s length prices are exempted from approval from shareholders and board, except the prescribed approvals under Section 177. Whereas Clause 49 requires material related party transactions to be approved by way of a special resolution in the members meeting, in-spite of such transactions being in the ordinary course of business and carried out at an arm‟s length price | |

| J. | How to compute annual turnover and net-worth for the purposes of Rule 15(3) and Clause 49? |

| net-worth and the annual turnover shall be based on the audited financial statements of the preceding financial year | |

| K. | Whether the thresholds Sub-rule 3 of Rule 15 the Board Meeting Rules, 2014 is applicable to individual transaction of sale or purchase or is applicable at an aggregate level? |

| The Second amendment to the Board Meeting Rules 2014 includes an explanation clarifying that the limits listed under the sub-rule 3(i) to (iv), shall apply for transaction or transactions to be entered into either individually or taken together with all the previous transactions during a financial year. | |

| L. | Can a related party transaction entered into without obtaining approval from the board/ members be ratified subsequently? |

| Yes, contract or arrangement entered into without obtaining the consent of the board or approval by a special resolution in the general meeting, as the case may be, shall be ratified by the board or members, by way of a special resolution, within three months from the date of such contract or arrangement being entered. | |

| M. | Can a director who is interested in a contract or arrangement with a related party be present during the discussion at the board meeting for approval of such transactions? |

| Pursuant to the provisions of Sub rule 2 of Rule 15 of the Companies Board Meeting Rules, 2014, none of the interested directors shall be present during the course of discussions at the board meeting. | |

| N. | What are the provisions of the 2013 Act and clause 49, in connection with voting rights of related party at the general meeting? |

| Under the 2013 Act, a related party, being a member of the company and also interested in a contract or arrangement for which a special resolution is passed in the general meeting, shall not be entitled to vote on such special resolution.Whereas, under the clause 49 every related party, whether interested or not in a transaction being subject to special resolution, shall mandatorily be abstain from voting | |

| O. | How to interpret the term “Ordinary Course of its Business” (OCB) as used in the context of „related party transaction‟ under the 2013 Act? |

| which are directly or indirectly connected to or necessary to conduct its business. For example, company ABC which is primarily engaged in the business of manufacturing and selling auto parts, and advancing loans to a related party which is in the business of providing information technology services, could be viewed as a transaction not in the OCB. Whereas, if the company ABC entered into a contract with related party to avail travel services for its employees/ staff, such services, being necessary for ABC‟s ordinary activities, could be regarded as transaction in the OCB. | |

| P. | Whether provisions of the Companies Act, 2013 and relevant rules framed thereunder are applicable to every company? |

| Yes, as of now the provisions in connection with „related party‟ and „related party transactions‟ are applicable to every company including private, public or public listed companies | |

| Q. | Powers of Board to Approve any related party transaction. |

|

Where a Company operating only through Board of Director:The Board of Directors must approve all the related party transactions, where such related party transactions are: not in the ordinary course of its business; · in the ordinary course of its business, but carried at other than arm’s · length price |

|

| R. | Powers of Audit Committee to Approve any related party transaction. |

| A Company having an audit committee, under Section 177 of the 2013 Act Audit committee shall approve all related party transactions; and· Subsequent modifications to the previously approved related party transactions. | |

| S. | Powers of Share holders for Approve any related party transaction |

|

No contract or arrangement for a transaction with a related party shall be entered into without prior approval of:(a) the Board of Directors/ Audit committee, as the case may be, and (b) by members by way of a special resolution If such a contract or arrangement is for: i. transactions which are not in the ordinary course of the business; ii. transactions which are in the ordinary course of the business, but are carried at other than arm’s length price. |

|

| T. | Power of approval of Related Party Transactions in the Listed Company. |

|

Every listed company must obtain an approval of its member by way of a special resolution in respect of material related party transactions. Such approval is mandatory even if the related party transactions are:· i. in the ordinary course of the business; and ii. carried at an arm’s length price |

|

| U. | List of Transactions which are covered under Section 188 of Companies Act, 2013. |

|

i. Sale of goods, material, services and supply of material ii. Purchase of goods, material and services iii. Sale or purchase of any kind of property (movable or immovable, tangible or intangible, financial or non-financial) iv. Disposing of any kind of property v. Leasing of property of any kind (movable or immovable, tangible or intangible, financial or nonfinancial) vi. Appointment of any agent for purchase of goods, purchase of material and purchase of services vii. Appointment of any agent for purchase of property 8. Appointment of any agent for sale of goods material and services viii. Appointment of any agent for sale of property ix. Appointment of related party to any place of profit or to any office in the company x. Appointment of related party to any place of profit or to any office in the subsidiary company xi. Appointment of related party to any place of profit or to any office in the associate company xii. Underwriting the subscription of any securities and derivatives |

|

| V. | Applicability of Section 188. |

| Section 188 will be applicable on ALL COMPANIES.· Private Limited

i. Public Limited ii. Listed Company |

|

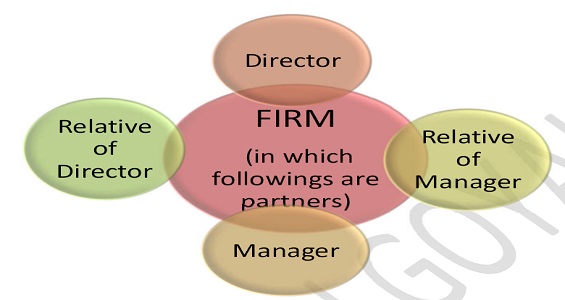

| W. | Definition of Related Party. |

| Given below in chart form. | |

| X. | When Contract will be voidable under Companies Act, 2013? |

| According to the section 188, sub section (1), any contact or arrangement must be passed through Board Meeting or Shareholders Meeting, as case may be,Suppose, the Contact has been made but the approval has not taken either in the Board Meeting or Shareholders Meeting within 3 months from the date of Contract, In that case the Contract shall be voidable at the option of the Board | |

| Y. | Procedural requirements to carry on the transaction: |

|

i. Prior approval from Board is required. Further, in certain cases, prior approval of shareholders by way of special resolution is also required. ii. The details of the proposed transaction shall be circulated in the notice of the meeting. iii. The details and justification of the special transactions shall be referred in the Board’s Report. iv. Any director, interested in the transaction shall not be part of the meeting and he will also not vote in passing the Special Resolution, where applicable. v. All such transactions should be approved by the Audit Committee, where applicable |

THRESHOLD LIMITS UNDER COMPANIES ACT, 2013 FOR SPECIAL RESOLUTION:

| NATURE OF RELATED PARTY TRANSACTION | THRESHOLD LIMIT EARLIER | FROM-14TH AUGUST, 2014 |

| For Every Transaction | When paid Share Capital of Company is 10 Crore or More. | REMOVED FROM RULE |

| Sale, purchase or supply of any goods or materials directly or through appointment of agents (or) | Exceeding 25% of Annual Turnover | Exceeding 10% if Turnover of Company or Rupees 100 Crore Whichever is Lower |

| Selling or otherwise disposing of, or buying, property of any kind directly or through appointment of agents (or) | Exceeding 10% of Net worth | Exceeding 10% of Net worth or Rupees 100 Crore Whichever is Lower |

| Leasing of property of any kind (or) |

Exceeding 10% of Annual Turnover OR Exceeding 10% of Net worth |

Exceeding 10% of the Net worth of company or 10% of Turnover of Company of Rupees 100 Crore, Whichever is lover |

| Availing or rendering of any services directly or through appointment of agents (or) | Exceeding 10% of Net worth | Exceeding 10 % of Turnover of company or Rupees 50 Crore, Whichever is lower. |

| Appointment to any office or place of profit in the company, its subsidiary company or associate company (or) | Monthly Remuneration Exceeding Rs. 2.5 lakhs | NO CHANGE |

| Remuneration for underwriting the subscription of any securities or derivative | Exceeding 1% of Net worth | NO CHANGE |

Note:

i. Turnover and Net worth as per Audited Financial Statement of Preceding Financial Year.

ii. If any member is interested in any transaction, than such member shall not cast vote in meeting regarding such resolution.

iii. It is here by clarified that the limits specified in sub-clause (i) to (iv)shall apply for Transaction and Transactions to be entered into either individually or taken together with previous transactions during a financial year.

iv. Every Transaction enter into section 188 shall be enter into Director Report along with Justification.

MEANINGS OF TERMS USED UNDER COMPANIES ACT, 2013:

Meaning of Office or place of profit for this purpose:

i. Where such office or place is held by a director:

a. If the director holding it receives from the company anything by way of remuneration Over And Above The Remuneration to which he is entitled as director,

b. by way of salary, fee, commission, perquisites, any rent-free accommodation, or otherwise;

ii. where such office or place is held by an individual other than a director or by any firm, private company or other body corporate

a. If the individual, firm, private company or body corporate holding it receives from the company anything by way of

1. Remuneration

2. Salary

3. Fee

4. Commission

5. Perquisites

6. Any rent-free accommodation, or

7. Otherwise;

DISCLOSURE NORMS:

1. DISCLOSURES TO BE MADE IN NOTICE OF BOARD MEETING

The agenda of the Board meeting at which the resolution is proposed to be moved shall disclose:

i. name of the related party and nature of relationship;

ii. nature, duration of the contract and particulars of the contract or arrangement;

iii. material terms of the contract or arrangement including the value, if any;

iv. any advance paid or received for the contract or arrangement, if any; and

v. the manner of determining the pricing and other commercial terms, both included as part of contract and not considered as part of the contract;

vi. whether all factors relevant to the contract have been considered, if not, the details of factors not considered with the rationale for not considering those factors; and

vii. any other information relevant or important for the Board to take a decision on the proposed transaction.

2. DISCLOSURE BY INTERESTED DIRECTORS

Every director of a company who is in any way, whether directly or indirectly, concerned or interested in a contract or arrangement or proposed contract or arrangement entered into or to be entered into

i. with a body corporate in which such director or such director in association with any other director, holds more than 2% shareholding of that body corporate, or

ii. with a body corporate in which such director is a promoter, manager, Chief Executive Officer of that body corporate; or

iii. with a firm or other entity in which, such director is a partner, owner or member, as the case may be

shall disclose the nature of his concern or interest at the meeting of the Board in which the contract or arrangement is discussed.

Where any director who is not so concerned or interested at the time of entering into such contract or arrangement, he shall, if he becomes concerned or interested after the contract or arrangement is entered into, disclose his concern or interest forthwith when he becomes concerned or interested or at the first meeting of the Board held after he becomes so concerned or interested.

3. DISCLOSURES TO BE MADE IN THE EXPLANATORY STATEMENT TO BE ANNEXED TO NOTICE OF GENERAL MEETING:

i. name of the related party ;

ii. name of the director or key managerial personnel who is related, if any;

iii. nature of relationship;

iv. nature, material terms, monetary value and particulars of the contract or arrangement;

v. any other information relevant or important for the members to take a decision on the proposed resolution.

4. DISCLOSURES TO BE MADE IN BOARD’S REPORT:

The particulars of contracts or arrangement with related parties referred in section 188(1) of the Companies Act 2013 should be disclosed in the Directors Report for the financial years commencing on or after April 1, 2014 in Form AOC-2 enclosed as Annexure-I.

All material related party transactions that are entered into with effect from October 1, 2014, to be disclosed quarterly along with the compliance report on corporate governance pursuant to the requirements of clause 49 of the Listing Agreement. The company shall disclose the policy on dealing with Related Party Transactions on its website and a web link thereto shall be provided in the Annual Report.

5. DISCLOSURES TO BE MADE IN REGISTER OF CONTRACTS OR ARRANGEMENTS IN WHICH DIRECTORS ARE INTERESTED:

Every company shall maintain one or more registers in Form MBP 4, and shall enter therein the particulars of contracts or arrangements with a related party with respect to transactions to which section 188 applies.

TRANSACTIONS WHICH ARE DEEMED TO BE RELATED PARTY TRANSACTION:  DEFINITION OF RELATED PARTY:

DEFINITION OF RELATED PARTY:

Annexure I

Annexure I

Form No. AOC-2

(Pursuant to clause (h) of sub-section (3) of section 134 of the Act and Rule 8(2) of the Companies (Accounts) Rules, 2014)

Form for disclosure of particulars of contracts/arrangements entered into by the company with related parties referred to in sub-section (1) of section 188 of the Companies Act, 2013 including certain arm’s length transactions under third proviso thereto

1. Details of contracts or arrangements or transactions not at arm’s length basis

(a) Name(s) of the related party and nature of relationship

(b) Nature of contracts/arrangements/transactions

(c) Duration of the contracts / arrangements/transactions

(d) Salient terms of the contracts or arrangements or transactions including the value, if any

(e) Justification for entering into such contracts or arrangements or transactions

(f) Date(s) of approval by the Board (g) Amount paid as advances, if any:

(h) Date on which the special resolution was passed in general meeting as required under first proviso to section 188

2. Details of material contracts or arrangement or transactions at arm’s length basis

(a) Name(s) of the related party and nature of relationship

(b) Nature of contracts/arrangements/transactions

(c) Duration of the contracts / arrangements/transactions

(d) Salient terms of the contracts or arrangements or transactions including the value, if any:

(e) Date(s) of approval by the Board, if any: (f) Amount paid as advances, if any:

(Author can be reached at csdiveshgoyal@gmail.com )

Author Bio

Whether trade recievable and trade payable be considered in AOC-2

very well note, really appreciable.

one doubt : whether interest on loan of Directors and payment of Managerial remuneration is comes under the aforesaid threshold?..

doubt-whether interest on unsecured loan is covered under this contract?

Very useful and nicely explained.

Very well explained provisions. Thank You Very much

Very well expalained provisions. Thank You Very much

hey thanks informative